Mish's Global Economic Trend Analysis |

- G-20 Summit in Flames Already as EC President Blames US For Financial Crisis in Europe

- "Germany is a Credit Risk" Says Bill Gross; Germany Exiting Eurozone is One of Very Few Scenarios in Which German Bonds Do Well

- Another "We are Saved" Euphoria Lasts Only Moments; European Bond Market Revolts Already as Spain 10-Year Yield Hits Record High 7.28%

- Greek Election Sideshow; Socialists Win Absolute Majority in France; How Long Will the Bond Market Celebrate Another Glorious Can-Kicking Exercise?

| G-20 Summit in Flames Already as EC President Blames US For Financial Crisis in Europe Posted: 18 Jun 2012 06:08 PM PDT The G-20 summit is off to a great start if you like fireworks, endless bickering, and finger-pointing. Otherwise these summits are totally useless. When asked by a Canadian journalist "Why should North Americans risk their assets to help Europe?" EC President José Barroso replied "Frankly, we are not here to receive lessons in terms of democracy or in terms of how to handle the economy. The Guardian has further details in Barroso blames eurozone crisis on US banks. The opening day of the G20 summit was threatening to deteriorate into a fractious row between eurozone countries and other non-European members of the G20, notably the US, as EU commission president José Manuel Barroso insisted the origins of the eurozone crisis lay in the unorthodox policies of American capitalism.A Few Questions Nannycrats Might Consider

I am quite certain I can ask dozens of such questions. Let's be honest here. Yes the US caused lots of problems. So did the ECB, and so did the nannycrats. China played a part as well. Thus, those comments by Barroso are strictly from Fantasyland if not Idiotland. Europe created the euro, not the US. Europe foolishly pledged more and more money to Greece, not the US. And eurozone rules are at the heart of Europe's mess, not anything the US did. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 18 Jun 2012 11:01 AM PDT Bill Gross echoes my statements that Germany is poised for a big hit either by a piecemeal breakup of the eurozone, by Germany indefinitely ponying up more money to keep the eurozone intact, or by Germany saying it has had enough and goes back to the deutsche mark. On Bloomberg TV's "Market Makers" Bill Gross of PIMCO spoke to Erik Schatzker and Stephanie Ruhle today and said, "I would be leery of German bunds simply because there are only a few scenarios in which they can do well…Germany for me is a credit risk. It's not an attractive market." Partial Transcript Gross on what he sees happening in Europe:Leery of German Bonds I concur with Bill Gross. I suppose yields could go negative in a capital flight scenario, but otherwise where are German bonds headed? Are Germany Two-Year Bonds attractive at .025%?  I do not think .025% is an attractive rate for 2-year bonds. Nor is 1.41% an attractive rate for 10-year bonds. A bet on long-term German bonds is a bet that Germany is not affected by eurozone fallout and/or returns to the deutsche mark. One reader commented this is not about return-on-investment but rather return-of-investment. Perhaps so. However, return-of-investment may not hold up if German bonds yields soar due to credit risk. While I think Germany should exit the eurozone, a piecemeal breakup that has a nasty spillover into Germany is as likely. For a discussion why, please see "Multi-Stage" Nannycrat Proposals; Devaluation - The Last Option? Focus on the Obtanium not the Unobtanium Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

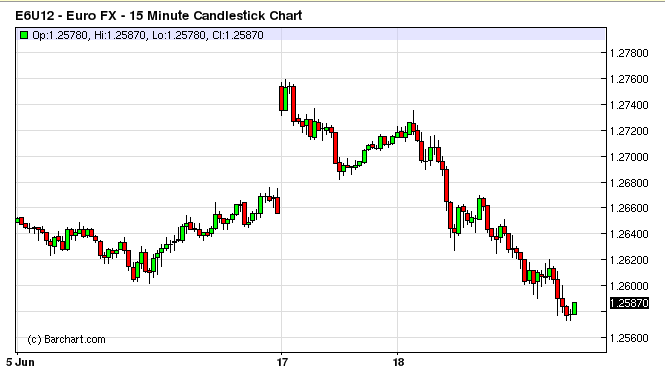

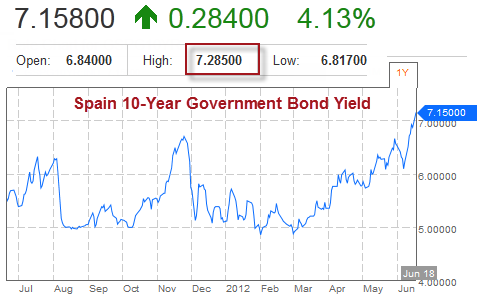

| Posted: 18 Jun 2012 09:44 AM PDT Following news of the victory of the "pro-bailout the French and German banks party" known in Greece as "New Democracy", the euro sailed to 1.2760 and a lovefest in the Asian equity markets began. However, the rally in the euro did not last long. There was no rally in the European bond markets to begin with. The US stock market opened in the red. Euro 15-Minute Chart  click on chart for sharper image Chart from Barchart The rally in the euro lasted about 39 candles, 585 minutes, or roughly 9.75 hours. It was essentially straight downhill once the European markets opened. European Bond Market Revolts Already The far more important European bond market never got going in the first place as the following charts from Bloomberg show. Spain 10-Year Yield Hits Record High 7.28%  Chart from Bloomberg. Italy 10-Year Yield Hits 6.17%  Chart from Bloomberg. Greece wants to stay on the euro. Lovely. How long will Spain and Italy? What about France? For further discussion, please see Greek Election Sideshow; Socialists Win Absolute Majority in France; How Long Will the Bond Market Celebrate Another Glorious Can-Kicking Exercise? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 18 Jun 2012 01:18 AM PDT New Democracy won the Greek election. However, party leader Antonis Samaras still needs to form a coalition. If this seems like Déjà Vu, it's because it is. We were in the same place following the May election. Does the Outcome Matter? This go around, I expect Pasok will reluctantly cave in and form a coalition with New Democracy. The price might be high, such as demanding the much despised Antonis Samaras to step aside. Regardless, does the outcome matter? The answer is "not really", except in the very short term, because of what I said in Europe Will Splinter Regardless of Greek Election Outcome; "France Has At Most Three Months Before Markets Make Their Mark" says German Official All eyes are focused on the Greek election on Sunday.Socialists win absolute parliament majority in French election The results are in: Hollande's Socialists win absolute parliament majority in French election French President François Hollande's Socialists won an absolute parliamentary majority on Sunday, strengthening his hand as he presses Germany to support debt-laden euro zone states hit by austerity cuts and ailing banks.Greek Sideshow Hollande now has free rein to do whatever he wants. I believe he will do just that, and if so the bond markets will not take too kindly to it, nor will Merkel, and nor will the average citizen in Germany, Finland, the Netherlands, or Austria. An amazing amount of attention has been focused on the election in Greece when a far more important election was just held in France. The French election received scant media coverage. Moreover, Spain has not been fully reckoned with, nor has Italy. France Has At Most Three Months If Hollande carries out his stated programs, it won't take three months before the bond market revolts, Germany revolts, or both revolt. Step back for a moment and look at the enormous fundamental rift between France and Germany. Regardless of the outcome of the Greek election, that rift is not going away. Hollande already threatened to renegotiate the so-called Merkozy treaty (which by the way France has not yet ratified). Also note that last Thursday, the Bundesbank (Germany's central bank) came flat out and stated Policymakers Should Refrain From "Wild Goose Chase" of Higher Firewalls and Merkel Warned "Limited German Resources" Assume France does ratify the treaty. Major revisions down the road are virtually impossible. Dead Before Arrival Thus, I was highly amused when a group of eurozone Nannycrats agreed to meet later this month to devise a master plan for a eurozone fiscal and banking union. (see Details of the Secret "Nannyplan" Emerge; Proposed Nannygroup Uniforms) My response was "Dead Before Arrival": Bundesbank Shoots Down EU Banking-Union Proposal; Eight Lessons the EU Needs to Learn Another Glorious Can-Kicking Event For now the market is celebrating another glorious can-kicking event. The celebration will last until the bond market has had enough. I expect days at most, and perhaps hours. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment