Mish's Global Economic Trend Analysis |

- France, Italy, Spain Services PMI Show Continued Sharp Decreases; Eurozone Composite PMI Near 3-Year Low; Germany Services PMI at 6-Month Low

- Gaming the Odds of a Greek Euro Exit With and Without Contagion

- Oil Tanker Rates Lowest Since 1997 as Demand in Europe Plunges to 1996 Level, Production in US at 13-Year High; IMF Smoking Happy Dope

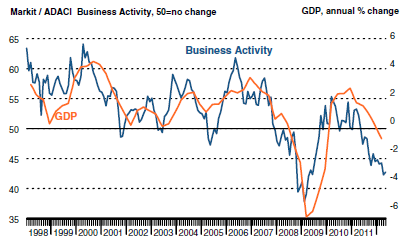

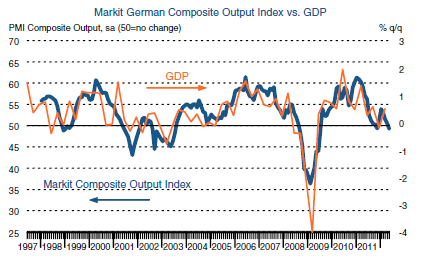

| Posted: 05 Jun 2012 06:57 PM PDT The Markit PMI data from Europe shows still more deterioration led by France, Italy, and Spain. Let's take a look at a few countries. France: Business Activity Continues Contraction at Marked Pace Key points:Italy: Services Activity Continues Contraction at Sharp Rate in May Key Points:Spain: Activity and new business both decline at faster rates Key points:Germany: German Composite Output Index in Contraction Key points:Eurozone: Composite PMI near-three year low in May Key Points:If the ECB is looking for an excuse to cut rates, it sure has one. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Gaming the Odds of a Greek Euro Exit With and Without Contagion Posted: 05 Jun 2012 01:54 PM PDT A key question on trader's minds is who will win the June 17th Greece election and whether it results in a Greek exit of the eurozone. Deutsche Bank gives it assessment in a report called Probability weighting EUR views on Greece Under a variety of assumptions, the market pricing looks consistent with: a) significant odds in favor of Greece remaining part of the EUR zone and EUR/USD trading between 1.25 and 1.30; and, b) a worst case Greek exit global contagion scenario taking EUR/USD to 1.10, but not to levels as low as parity.Deutsche Bank Probability Chart  click on chart for sharper image Odds Not 50-50 Deutsche Bank thinks the probability that New Democracy or Syriza wins is equal, 50% each. I think the odds Syriza wins is about a 2-1 favorite as explained in Greek Polling Ban In Effect Until Election; Latest Results Show SYRIZA Support at 31.5 percent, Well in the Lead Over New Democracy; Why I expect Syriza to Win For an update, please see "Terror-Mongering" in Greece About to Backfire? Will Greeks Vote for "Complete Idiots"? Four Possibilities Note that Deutsche Bank thinks that even if Syriza does win, Greece is as likely to remain in the eurozone as not. That strikes me as being far too optimistic. Even if Syriza stays in for a while, it will eventually run out of money. Contagion Scenarios Finally, please note that the Deutsche Bank contagion scenarios total a mere 28%. What does "contagion" even mean? As I have explained before, Spain has problems of its own making not related to Greece at all. Spain is not going to exit the eurozone solely or even significantly because of Greece. True Contagion The true contagion scenario is not what people think but rather the reverse. Greece exits the eurozone, recovers, and other countries decide to do the same. In the context of the Deutsche Bank article, I fully expect Spain to exit the eurozone. Is that contagion? It depends on why and how you define the word. Finally, even if New Democracy wins, the odds of a Greek exit do not drop to a mere 5% as the above table shows. I would say they are still 50% minimum and depending on your timeframe as high as 85%. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 05 Jun 2012 09:26 AM PDT Bloomberg reports Oil Tankers Squeezed as Rates Drop to Lowest Since '97. Aframaxes, already this year's worst- performing oil tankers, are poised for the lowest annual rates in at least 15 years as Europe's economic stagnation curbs demand, the region's most-accurate shipping analysts said.Comments From Tim Wallace Reader Tim Wallace says ... Hello MishIMF Smoking Happy Dope To that I would add the IMF is smoking "happy dope" to believe the eurozone will contract a mere .3% in 2012 and expand at .9% in 2013. Moreover, the US economy is clearly slowing rapidly and is likely in recession right now. I will have the latest US 3-month oil usage charts from Tim Wallace shortly. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment