Mish's Global Economic Trend Analysis |

- Public Unions Bankrupt Illinois: Unpaid Bills Top $9 Billion as Comptroller Reports "State Treading Water"; Mish's Eight-Point "Bold" Plan to Save Illinois

- Eurozone Manufacturing PMI Hits 34 Month Low; German Manufacturing Hits 33 Month Low; Orders Drop Steeply Across the Board

- Eight of Ten Largest Stocks in Spanish Ibex Index Below Liquidation Value; Madrid Rejects Regional Budgets Representing 32.5% of GDP; Treasury Warns of "Immediate" Intervention

| Posted: 23 Apr 2012 12:54 PM PDT Governor Pat Quinn rammed through the largest tax hikes in Illinois history last year. On January 13, 2011, Governor Pat Quinn signed off on a 67% hike in personal income taxes and a 46% hike in corporate taxes. The result is not what the governor thought. Businesses have fled, more have threatened to leave and Quinn responded with sweeteners. Moreover, Illinois pension plans are still the worst funded in the nation, and the state is still struggling to pay bills. Bloomberg reports Illinois 'Treads Water' as Unpaid Bills Top $9 Billion Illinois's backlog of unpaid bills has risen to more than $9 billion because of pension costs and falling federal aid, leaving the state "essentially treading water," Comptroller Judy Baar Topinka said.Public Unions Bankrupt Illinois Just where was this "bold plan" when Quinn was running for Governor? Nowhere in sight. And now he wants "voluntary" contributions. Give me a break. Illinois is bankrupt and corrupt politicians like governor Quinn, Speaker of the Illinois House, Mike Madigan, and all the union panderers in Chicago ruined the state by giving into "collective bargaining" demands from public unions. Voluntary 3% contributions by unions is not a "bold plan" and will not do a damn thing. Illinois needs to scrap its defined benefit plans immediately and claw back on promised benefits under threat of default. Moreover, Illinois needs to scrap prevailing wage laws and end collective bargaining of public unions immediately if not sooner. Illinois desperately needs a "Bold Plan" before the entire stat looks like Central Falls or Providence Rhode Island, or Detroit Michigan.

Mish's Eight-Point "Bold" Plan to Save Illinois

The $80,000 cap is s suggested starting point for discussion. It may be higher or lower based on point number eight. Now that's a bold plan, and a badly needed one at that. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

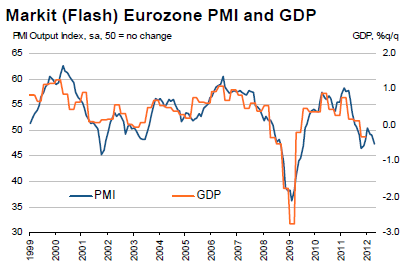

| Posted: 23 Apr 2012 09:55 AM PDT Today, European data shattered two long held beliefs by Markit and in general, unthinking economists everywhere. Shattered Myths

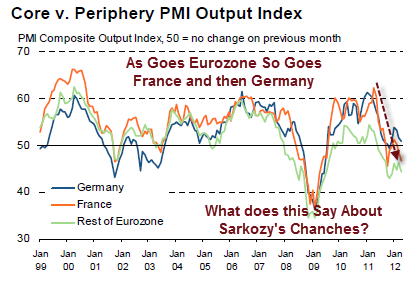

Markit reports Eurozone sees stronger rate of decline at start of second quarter Eurozone Reality Markit Finally accepts reality, albeit with a huge understatement "Prospects do not look good." Really? After 5 months of making silly statements about "short, weak recession" complete with Germany bucking the trend, that is acceptance of reality, sort-of. As Goes Europe, So Goes Germany and France As I have been saying for at least six months, the Eurozone recession will be neither short nor mild. Spain, Greece, and Portugal are in outright depressions and Italy may head there. Take a look at that chart above on the periphery vs. France and Germany. France has now caught up on the downside with the rest of Europe and Germany will follow. Coupled with a huge slowdown in China, and a feeble and faltering recovery in the US, there is zero chance that France and the vaunted German export machine will decouple from the rest of Europe. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 23 Apr 2012 08:37 AM PDT The Spanish hit parade keep right on rolling. Courtesy of Google Translate, please consider a trio of articles forwarded by my friend Bran who lives in Spain. Madrid Rejects Regional Budgets Representing 32.5% of GDP El Economista reports Treasury Rejects Budgets Submitted by Catalonia and Andalusia The Ministry of Finance and Public Administration has returned the draft budget to the regions of Andalusia and Catalonia because it considers its budget rebalancing plan does not fit within the deficit target regions set for this year, 1.5% of GDP.Treasury Warns of "Immediate" Intervention Going one step further, Treasury warns that Any Autonomy may be Subjected to an "Immediate" Intervention" Forced Austerity in the regional governments is coming right up. Spanish IBEX Index  The Spanish stock market has now given back nearly all of its gains since March 2009. Eight of Ten Largest Stocks in Spanish Ibex Index Below Liquidation Value Please consider Eight of Ten Largest Stocks in Spanish Ibex Index Below Liquidation Value The article states it is "ludicrous" that eight of the ten heavyweights trade below their book value. I suggest book values are inflated and the Spanish banking system is insolvent. Certainly credit default swaps on sovereign debt are not encouraging. Check out this nonsense by JP Morgan. "The banking problem is not liquidity, but mainly of confidence," says JPMorgan Pellón mentioning that pointed in recent days that Spanish banks retain about 90,000 million from the program LTRO European Central Bank. Enough money to meet all funding requirements for the remainder of the year.Inflated Book Values, Insolvent Banks Banks may have LTRO funding but it would be nice if the clowns at JPMorgan would advise exactly how Spanish banks are going to pay back those loans. The problem is not confidence nor liquidity, but rather solvency. In the absence of further bailouts, many European banks have negative value. What About the Euro? Moreover, JP Morgan missed another crucial point, best expressed by the question: What happens in a eurozone breakup when Spain exits the Euro? Since that is a significant possibility (I believe likelihood), anyone in Spain with any money and any common sense should get their money out of Spain right now. Capital flight is indeed underway and that flight will continue to pressure Spanish equities until it stops. Capital controls may be just around the corner. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment