| China Manufacturing PMI™ Decreases at Second-Fastest Rate in Three Years Posted: 01 Apr 2012 08:31 PM PDT The slowdown in China continues at an accelerating rate according to the HSBC China Manufacturing PMI™. March data showed manufacturing production falling for the fourth time in the past five months. Factory output was reduced largely in response to lacklustre demand from domestic and external markets. New orders fell at the fastest rate in 2012 so far, while new export business decreased for a second month in succession. Manufacturers reduced their employee numbers as a result, while purchasing activity was also down from one month earlier. There was little change on the price front, with factory gate charges falling modestly, and the rate of input cost inflation remaining somewhat subdued.

Companies reported a renewed decline in manufacturing output during March, with the rate of contraction the steepest since November and the second-sharpest in three years. Behind the overall decrease in factory output was a further decline in total new business. Underlying demand weakness was broad-based across domestic and external markets, with new export business also falling moderately from one month earlier. Rates of decline in both cases were among the sharpest seen since the 08/09 financial crisis.

Key points

- Reduced factory output reflects falling new business from home and abroad

- Manufacturing employment down at sharpest rate in three years

- Input price inflation ticks higher, but remains modest overall

Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Bankruptcy, the Best Way to Deal with Public Unions; Bold New Tactics Long Overdue; Gov. Rick Snyder's Move on Detroit; $1.26 Trillion Pension Gap Posted: 01 Apr 2012 12:16 PM PDT Distressed cities are finally doing what they should have been doing long ago, declaring bankruptcy to force concessions from public unions. Numbers are still a trickle, but at soon as a major city such as Oakland or LA selects that option, we will likely see a torrent of municipal bankruptcies. At a packed, two-day conference on municipal woes sponsored by Michael Stanton, the publisher of The Bond Buyer Distressed Cities Discuss Bold Tactics in a New Fiscal Era. The conference was devoted to a discussion of the strengths and weaknesses of the more powerful tools being used in many cities these days, including receiverships, emergency declarations and even bankruptcy.

Attempts to plug budget holes with one-time transactions are giving way to other approaches, "This is truly a new era for dealing with troubled municipalities," said Stanton.

New woes were unfolding elsewhere even as a capacity crowd of government officials, investors, lawyers and credit analysts were gathering here to discuss the trend.

In Jefferson County, Ala. — which filed the biggest Chapter 9 municipal bankruptcy in American history this fall after its sewer-construction financing fell apart and a court threw out one of its taxes — county commissioners were voting to default on a general obligation bond payment.

In Detroit, city and state officials were sparring over how much emergency aid the city might be able to get, and how much state oversight and control would accompany it.

Stockton, Calif., was in negotiations in a last-ditch effort to avoid becoming the biggest American city yet to declare bankruptcy. And just two hours west of Philadelphia, Harrisburg, the state capital, recently announced that it would default on a payment coming due to general obligation bondholders.

Robert G. Flanders Jr., the state-appointed receiver for Central Falls, R.I., said his city's declaration of bankruptcy had proved invaluable in helping it cut costs. Before the city declared bankruptcy, he said, he had found it impossible to wring meaningful concessions out of the city's unions and retirees — who were being asked to give up roughly half of the pensions they had earned as the city ran out of cash.

"The municipality is on bended knee asking the retirees and unions to come to the table and give up their contract rights," he recalled. "All of that leverage shifts once you have the gumption to pull the Chapter 9 trigger. And guess what? That produces agreements quicker and more effectively than otherwise."

Naomi Richman, a managing director at Moody's Investors Service, wondered aloud whether it might become more acceptable for cities to declare bankruptcy.

"Back in the '80s, the stigma against corporate bankruptcy fell away, and it became viewed as a strategy a corporation might pursue for various reasons," Ms. Richman said. "Recently, with the residential housing collapse, individual bankruptcy has less of stigma in society — it's a strategy that a person might be advised to follow if they have a debt that they can't afford. Could the same thing happen for municipal bankruptcy?" Rhode Island City Offers Gloomy Lesson The Huffington Post reports As Detroit Bankruptcy Looms, Rhode Island City Offers Gloomy Lesson PHILADELPHIA -- Bankers, consultants and elected officials gathered at a conference here on Wednesday to discuss a hot political question for the formerly sleepy municipal bond industry: how to sell the need to protect the rights of bondholders -- the often large, distant financial institutions who extend the credit that keeps towns humming -- when cities enter financial crisis. The issue has most recently been thrown into relief as a Monday deadline for the city of Detroit to accept a consent order to fix the city's budget looms.

"While the economists have declared the recession to have been over for almost three years now, the problems of state and local governments continue to mount," said Bob Kurtter, the managing director for U.S. state and regional ratings at Moody's Investors Service. "Default continues to be rare," he said, but "our ratio of downgrades to upgrades has been negative for the past 12 quarters."

As more cities and states struggle to fill the $1.26 trillion gap between what they have actually set aside for pensions and retirement benefits and what they have promised, municipal accountants will grapple with questions that will increasingly resemble those faced by Detroit or former Rhode Island Supreme Court Justice Robert Flanders when he was appointed last year as receiver for Central Falls, a struggling former factory town in the Ocean State.

From the comments of Flanders and others at the municipal bonds conference, it seems like the industry is in agreement about one thing going forward: someone is going to have to suffer, and it shouldn't be bondholders. Bondholders and Unions Should Both Share the Pain This idea that bondholders should not take losses is ludicrous. Anyone stupid enough to buy Detroit bonds should pay a hefty price. Moreover, since untenable promises made to public unions are generally a leading cause of bankruptcy, public unions should suffer as well. Gov. Rick Snyder Move on Detroit The Christian Science Monitor reports Detroit nears deal to avert bankruptcy, but is it a state takeover? March 27, 2012

With Detroit now formally in a state of "severe financial emergency," city and state officials are grappling with the terms of an agreement to resolve the crisis, which both sides say they expect to be signed by week's end.

So far, Michigan state officials are avoiding talk of a takeover – a toxic term in a majority black city whose elected officials are opposing the appointment of an emergency manager. Detroit officials are calling for more financial support from the state.

While Michigan Gov. Rick Snyder (R) says he wants to avoid assigning an emergency manager to control the city's finances, the agreement being worked out between the city council and the state treasurer's office is expected to force the most extensive financial restructuring ever experienced by Detroit, or any other US city its size.

Governor Snyder now has 10 days to deliver a "consent agreement," according to a new law that allows the state to take financial control of any municipality facing bankruptcy. Since the law passed in March 2011, Michigan has placed four cities and two school districts under emergency management.

The law allows the state to break collective bargaining agreements, privatize city assets, fire local officials, and force a restructuring to keep basic city services flowing.

"It's a big experiment," says Vincent Hutchings, a political scientist at the University of Michigan in Ann Arbor. "Detroit is a high-profile city with a lot of issues."

City officials oppose referring to the final deal as a "consent agreement," which can lead to an emergency manager. The city wants to retain power to approve budgets but will hire a chief financial officer who will report to the mayor, said Deputy Mayor Lewis on Tuesday. The city also wants the state to lend Detroit money – a move that Snyder has refused in the past.

Meanwhile, many Detroit residents are protesting the possibility of the state playing a larger role in management of their city. An open meeting of the state commission was nearly shut down Monday by protesters who shouted, sang, and angrily denounced the state officials for what they see as trying to intervene with the democratic process. One activist filed a request with the Michigan Supreme Court for an emergency injunction to stop Snyder's team from moving forward.

Adding to the drama is the weekend hospitalization of Detroit Mayor Dave Bing, who remains bedridden. $1.26 Trillion Pension Gap The only way to fill a pension gap of that size is to reduce benefits. Tax hikes are out of the question. And the fastest, easiest, and best way to get pension concessions from public unions is to reduce benefits and tell the unions what they get. There is no need to negotiate. Central Falls did not negotiate, they said take 50% or you may end up getting even less. Ultimately, the only way to deal with public unions is to strip them of all power including collective bargaining rights, then claw back ridiculous benefits in bankruptcy court. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

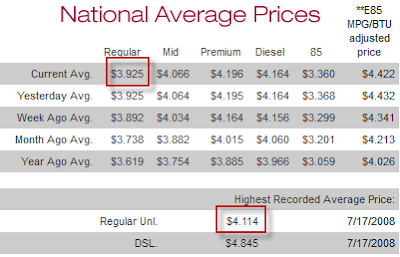

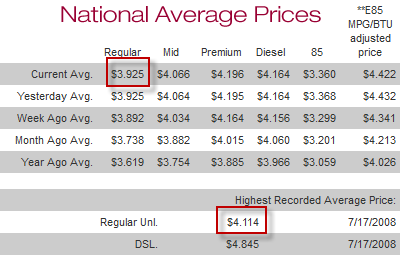

| Gasoline Prices Approach Highest Ever; Who is to Blame? Posted: 01 Apr 2012 02:06 AM PDT National gasoline prices inch ever so higher. The national average is now $3.925, approaching the all-time high of $4.114 on 7/17/2008 according to the Fuel Gauge Report.  Locally, my price in Northern Illinois is about $4.28. Illinois' average is $4.25. Prices in Chicago are higher. Obama Finds Oil in Markets Is Sufficient to Sideline Iran The New York Times reports Obama Finds Oil in Markets Is Sufficient to Sideline Iran. After careful analysis of oil prices and months of negotiations, President Obama on Friday determined that there was sufficient oil in world markets to allow countries to significantly reduce their Iranian imports, clearing the way for Washington to impose severe new sanctions intended to slash Iran's oil revenue and press Tehran to abandon its nuclear ambitions.

One senior official who had met with the Saudi leadership, said: "There was no resistance. They are more worried about a nuclear Iran than the Israelis are."

Still officials said, the administration wanted to be sure that the Saudis were not talking a bigger game than they could deliver. The Saudis received a parade of visitors, including some from the Energy Department, to make the case that they had the technical capacity to pump out significantly more oil.

But some American officials remain skeptical. That is one reason Mr. Obama left open the option of reviewing this decision every few months. "We won't know what the Saudis can do until we test it, and we're about to," the official said.

The new sanctions — which effectively force countries to choose between doing business with the United States and buying oil from Iran — threaten to fray diplomatic relationships with close allies that buy some of their crude from Tehran, like South Korea.

But in a conference call with reporters, senior administration officials said they were confident that they could put the sanctions in effect without damaging the global economy.

"There is no rational reason why oil prices are continuing to remain at these high levels," the Saudi oil minister, Ali Naimi, wrote in an opinion article in The Financial Times this week. "I hope by speaking out on the issue that our intentions — and capabilities — are clear," he said. "We want to see stronger European growth and realize that reasonable crude oil prices are key to this."

By certifying that there is enough supply available, the administration is also trying to gain some leverage over Iran before a resumption of negotiations, expected on April 14. Saudi Arabia Will Act to Lower Soaring Oil Prices Ali Naimi, minister of petroleum and mineral resources in Saudi Arabia, claims Saudi Arabia Will Act to Lower Soaring Oil Prices High international oil prices are bad news. Bad for Europe, bad for the US, bad for emerging economies and bad for the world's poorest nations. A period of prolonged high prices is bad for all oil producing nations, including Saudi Arabia, and they are bad news for the energy industry more widely.

It is clear that sustained high prices are starting to take their toll on European economic growth targets. They are contributing to trade balance deficits and feeding inflationary pressures. It is an unsatisfactory situation and one Saudi Arabia is keen to help address. In an interconnected world, European economic growth is in our national interest. No one benefits from a stagnating European economy and we want to do what we can to help encourage growth.

It is clear that geopolitical tensions in the region, and concerns over supply, are helping to keep prices high.

Yet fundamentally the market remains balanced. It is the perceived potential shortage of oil keeping prices high – not the reality on the ground. There is no lack of supply. There is no demand which cannot be met. Total commercial stocks for OECD nations are within target, and there is at least 57 days forward cover, enough to handle almost any eventuality.

So what can Saudi Arabia actually do?

We want to correct the myth that there is, or could be, a shortage. It is an irrational fear, a fear without basis.

For the record, as things stand today, our inventories in Saudi Arabia and around the world are full. Our Rotterdam inventory is full, our Sidi Kerir facility is full, our Okinawa facility is full – 100 per cent full.

So the story is one of plenty. Supply is not the problem, and it has not been a problem in the recent past. There is no rational reason why oil prices are continuing to remain at these high levels.

I hope by speaking out on the issue that our intentions – and capabilities – are clear. We want to see stronger European growth and realise that reasonable crude oil prices are key to this.

Over the past 200 years, oil has powered incredible, and unprecedented, economic and social progress in Europe and the wider world. It has transformed our lives and will continue to power the global economy for many decades to come. It will only do so if prices reach a more reasonable level – so it is in all our interests to do what we can to achieve this aim. Who is it Blame For High Oil Prices? I am skeptical of the Saudi claim over the long haul. Near-term however, assuming you believe the Saudi story, then who is to blame? The answer is not oil speculators. The answer is central banks pumping liquidity in unheard of amounts coupled with Mideast tensions caused by Obama's policy. Central banks can print money, but they cannot determine where it goes, if anywhere. The Fed wants banks to lend and home prices to rise. Instead, we have high global oil prices and arguably another stock market bubble. So who is to blame? The answer is easy: Obama, the Fed, and central banks in general. Don't look to Mitt Romney for the answer. His war-mongering policies exceed those of president Obama and that would likely make matters far worse. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

No comments:

Post a Comment