| CalPERS Earned 1.1% on Investments in 2011, Plan Assumptions are 7.75% Posted: 24 Jan 2012 09:25 PM PST Pension plans rebounded sharply in 2009 and 2010 from the devastating losses in 2008. However they never got back to even. 2011 was another poor year, and in spite of the start to 2012 I expect this year and/or next year to suffer more losses, or alternatively the market to limp along with no gains for a number of years. In other words, pension plans are already in trouble and things are about to get worse. For example, the LA Times reports CalPERS earns 1.1% on investments in 2011 The nation's largest public pension fund, the California Public Employees' Retirement System, posted a 1.1% return on its investment portfolio in 2011, Chief Investment Officer Joseph Dear told his board.

The 2011 performance was well below the estimated average annual return of 7.75% that the fund's actuaries say is needed to meet current and future obligations to its members.

The $229.5-billion CalPERS provides retirement and other benefits for 1.6 million state and local government employees and their families.

CalPERS' annual investment results, whose volatility has echoed that of the overall markets, have become the focal point in an ongoing debate about looming pension fund liabilities and the ability of future generations of taxpayers to continue financing them. Gov. Jerry Brown has said he wants to overhaul state and local government pension programs, but whether he and the Legislature have the political wherewithal to do so in an election year remains unclear.

During the 2011 calendar year, CalPERS lost 7.95% on its public equity investments, lost 2.29% on its hedge fund investments, earned 12.38% on bonds and earned 9.92% on real estate.

CalPERS had a return of 11.6% for fiscal 2010 and a massive recession-related loss of 23.4% for fiscal 2009. Note those first set of numbers are for the calendar year, the latter set for the fiscal year. Fiscal year returns post on June 30. I have been saying for years that it is going to be next to impossible for pension plans to make their plan assumptions. Even 5% annualized for the next decade will be very hard to get in a stocks and bonds portfolio with bond yields so low. A move to equities risks another 2008-style plunge. Pension benefits and plan assumptions are simply too high. A taxpayer revolt in California over those promises is inevitable. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Japan Faces Moment of Truth: First Annual Trade Deficit Since 1980; New Trend or Simply the Tsunami Effect? Posted: 24 Jan 2012 05:49 PM PST Japan is in deep serious trouble the moment it enters a sustainable period of negative or neutral current account balances. If Japan becomes dependent on foreigners to finance rollovers on its debt either the Yen sinks or interest rates rise. Interest rates at a mere 3% would currently consume all of Japan's tax revenue. Japan's Fiscal Pressure Intensifies Bloomberg reports Japan's Fiscal Pressure Intensifies as Tax-Boost Plan Insufficient Japan's government said it will probably miss its goal of balancing the budget by 2020 even with its proposed doubling of the sales tax, underscoring the scale of the nation's fiscal challenges.

The primary budget deficit, which excludes the cost of servicing debt, will be the equivalent of 3.1 percent of gross domestic product for the year through March 2021, the Cabinet Office said in Tokyo today. Hours after the release, Prime Minister Yoshihiko Noda reiterated his call for opposition lawmakers to engage in talks on boosting the sales levy.

"To balance the budget, the rate needs to rise further," said Takuji Okubo, chief Japan economist at Societe Generale SA in Tokyo, referring to the sales-tax level. "We've passed the point where we can soft-land the fiscal situation. The question is how hard the landing is going to be." Japanese PM Reshuffles Cabinet to Push Tax Hike Please consider Japanese PM reshuffles cabinet to push tax hike Japanese Prime Minister Yoshihiko Noda carried out an anticipated cabinet reshuffle last Friday in a bid to consolidate his grip on power amid continued infighting within the ruling Democratic Party of Japan (DPJ).

Noda dumped Defence Minister Yasuo Ichikawa and Consumer Affairs Minister Kenji Yamaoka, both of whom are prominent supporters of the powerful DPJ faction headed by Ichiro Ozawa. At the same time, he promoted former DPJ president and foreign minister Katsuya Okada to deputy prime minister.

Okada has been given the task of implementing Noda's highly unpopular plan to double Japan's sales tax. Noda described the new lineup as "the best and strongest to push ahead with the inevitable topic of administrative, political and tax reforms," adding, "Mr Okada will not waver or run away from a major task. He is a politician who will produce results."

The government only announced its draft proposals for tax and social security reform on January 6. The plan involves a hike in the consumption tax rate from the present 5 percent to 8 percent in 2014 and to 10 percent in 2015. The government's ambiguous language implies further increases in the future, with some in business circles pressing for a rate as high as 25 percent, according to the Yomiuri Shimbun. Quite the Hike To go from 5% sales tax to 25% would be quite the hike. How long will this Prime Minister last? What happens if tax hikes do not go through or they raise insufficient revenue? First Trade Deficit Since 1980 While pondering the above questions, please consider Japan logs first trade deficit since 1980 Japan logged its first annual trade deficit in 2011 for over 30 years as the aftermath of the March earthquake raised fuel import costs even as slowing global growth and the yen's strength hit exports, threatening to erode the country's ability to fund its huge public debt with domestic savings.

Few market players expect Japan to immediately run a deficit in the current account, which includes trade and returns on the country's huge past investments abroad, as a steady inflow of profits and capital gains from overseas outweigh the trade deficit.

But the trade data underscores a broader trend in which Japan's competitive edge in the global market is eroding and it is increasingly reliant on fuel imports due to the loss of nuclear power, with reactors staying closed after routine checks due to public safety fears following the March disaster.

"What it means is that the time when Japan runs out of savings -- 'Sayonara net creditor country' -- that point is coming closer," said Jesper Koll, head of equities research at JPMorgan in Japan.

"It means Japan becomes dependent on global savings to fund its deficit and either the currency weakens or interest rates rise."

Japan logged a trade deficit of 2.49 trillion yen ($32 billion) for 2011, Ministry of Finance data showed on Wednesday, the first annual deficit since 1980.

Total exports shrank 2.7 percent last year while imports surged 12.0 percent, reflecting reduced earnings from goods and services and higher spending on crude and fuel oil.

In a sign of the continuing pain from slowing global growth, exports fell 8.0 percent in December from a year earlier, roughly matching a median market forecast for a 7.9 percent drop, due partly to weak shipments of electronics parts.

Imports rose 8.1 percent in December from a year earlier, in line with a 8.0 percent annual gain expected, bringing the trade balance to a deficit of 205.1 billion yen, against 139.7 billion yen expected. It marked the third straight month of deficits.

Bank of Japan Governor Masaaki Shirakawa said on Tuesday he did not expect Japan to continue logging a trade deficit as a trend and did not foresee the country's current account balance tipping into the red in the near future.

But Japan's days of logging huge trade surpluses may be over as it relies more on fuel imports, which may weaken the yen in the longer term.

Running a current account deficit would spell trouble for Japan as it means it cannot pay the cost of financing its huge public debt without overseas funds, although few analysts expect this to happen in the foreseeable future. Japan Faces Moment of Truth This is a moment of truth for Japan, perhaps the first of many. The question at hand is critical: Is the trade deficit a new trend or simply the long-lasting spillover from the tsunami? Today's answer may be different than tomorrow's. A prolonged European recession coupled with stubbornly high oil prices and a slowdown in China is the disaster scenario for Japan. That scenario is not at all unlikely. A deep European recession is a given and I believe a serious slowdown in China is a given as well. By pressing for tax hikes, it seems Japan's prime minister feels the same way, regardless of what the Bank of Japan says for public consumption. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Economic Insanity from Gingrich on Marijuana Use: Life imprisonment With No Parole; Who Benefits from War on Drugs? Big-Brother Expansionist Ideas: Gingrich Proposes "Free Radios" for Everyone in Cuba! Posted: 24 Jan 2012 10:25 AM PST Anyone wondering what kind of economically-illiterate, big-brother expansionist ideas Newt Gingrich might embrace as president can find the answer in several recent articles regarding his positions on marijuana usage, food stamps, drug testing, and surprisingly even "free radios". Please consider Gary Johnson hammers Newt for 'hypocrisy' on executing marijuana users Former New Mexico Gov. Gary Johnson went on offense against Newt Gingrich Monday, attacking the former House speaker's proposal to execute marijuana users as hypocritical, considering the GOP contender has himself admitted to smoking pot.

Johnson is currently seeking the Libertarian Party nomination for president, and is a proponent of legalizing the drug.

"Ideas are important, especially in a presidential campaign," said Johnson. "But some of Speaker Gingrich's ideas over the years are nothing short of scary. Under his legislation, anyone coming home to the U.S. and caught carrying enough marijuana (2 oz.) to distribute would be sentenced to life imprisonment with no parole — or if caught twice, would be sentenced to death."

Gingrich defended the legislation, the Drug Importer Death Penalty Act of 1996, in November as a way to get tough on Mexican drug cartels. Newt: Give the death penalty to drug cartel leaders Next up, please consider Newt: Give the death penalty to drug cartel leaders Republican presidential candidate Newt Gingrich says he supports using the death penalty as punishment for leaders of drug cartels who bring drugs into America.

Gingrich made the comments when asked in an interview with Yahoo! News if he still stands by a bill he introduced in Congress in 1996 allowing those convicted of smuggling drugs to be put to death.

"I think if you are, for example, the leader of a cartel, sure," Gingrich told reporter Chris Moody. "Look at the level of violence and the level of violence that they've done to society."

Elaborating, he said: "You can either be in the Ron Paul tradition and say there's nothing wrong with heroine and cocaine or you can be in the tradition that says, 'These kind of addictive drugs are terrible, they deprive you of full citizenship and they lead you to a dependency which is antithetical to being an American.'" Gingrich Lies About Paul's Position on Drug Usage For starters Gingrich purposely lied about Paul's position. Ron Paul never said "there's nothing wrong with drug usage". Indeed he has stated over and over he does not favor their use. What Paul has said, is he does not believe government should prosecute those who take drugs. I don't either. Legalizing drugs would take the profit out of them, stop countless robberies by addicts seeking to get drugs, and lower their overall usage. Primary and Secondary Beneficiaries of Gingrich's Expanded War on Drugs The primary beneficiaries of Gingrich's expanded war on drugs would be the gang-bangers, drug lords, and smugglers from Mexico. Higher costs and reduced supplies mean more profits for those who succeed at smuggling. The war on drugs can never succeed here. Unlike Singapore, the US is not going to put to death everyone who sells marijuana. Nor should we in the first place. It is not the government's role to interfere in the personal lives of citizens. The secondary beneficiary of Gingrich's proposal would be prison guards and union leaders. Indeed it is the unions who were behind California's inane strike-three law. Californian's pay out the nose and unions have benefited massively by the economically inept and morally corrupt ideas Gingrich espouses for the entire nation. Yahoo News Interview with Gingrich Finally please consider Newt Gingrich on drug laws, entitlements and campaigning: The Yahoo News interview Three Republican presidential candidates have shown an openness to handing over control of drugs and medical marijuana to the states. Would you continue the current federal policy making marijuana illegal in all cases or give the states more control?

I would continue current federal policy, largely because of the confusing signal that steps towards legalization sends to harder drugs.

I think the California experience is that medical marijuana becomes a joke. It becomes marijuana for any use. You find local doctors who will prescribe it for anybody that walks in.

Why shouldn't the states have control over this? Why should this be a federal issue?

Because I think you guarantee that people will cross state lines if it becomes a state-by-state exemption.

I don't have a comprehensive view. My general belief is that we ought to be much more aggressive about drug policy. And that we should recognize that the Mexican cartels are funded by Americans.

Expand on what you mean by "aggressive."

In my mind it means having steeper economic penalties and it means having a willingness to do more drug testing.

In 1996, you introduced a bill that would have given the death penalty to drug smugglers. Do you still stand by that?

I think if you are, for example, the leader of a cartel, sure. Look at the level of violence they've done to society. You can either be in the Ron Paul tradition and say there's nothing wrong with heroin and cocaine or you can be in the tradition that says, 'These kind of addictive drugs are terrible, they deprive you of full citizenship and they lead you to a dependency which is antithetical to being an American.' If you're serious about the latter view, then we need to think through a strategy that makes it radically less likely that we're going to have drugs in this country.

Places like Singapore have been the most successful at doing that. They've been very draconian. And they have communicated with great intention that they intend to stop drugs from coming into their country.

In 1981, you introduced a bill that would allow marijuana to be used for medical purposes. What has changed?

What has changed was the number of parents I met with who said they did not want their children to get the signal from the government that it was acceptable behavior and that they were prepared to say as a matter of value that it was better to send a clear signal on no drug use at the risk of inconveniencing some people, than it was to be compassionate toward a small group at the risk of telling a much larger group that it was okay to use the drug.

It's a change of information. Within a year of my original support of that bill I withdrew it.

Ron Paul and Barney Frank have introduced a similar bill almost every year since.

You have to admit, Ron Paul has a coherent position. It's not mine, but it's internally logical.

Speaking of Ron Paul, at the last debate, he said that the war on drugs has been an utter failure. We've spent billions of dollars since President Nixon and we still have rising levels of drug use. Should we continue down the same path given the amount of money we've spent? How can we reform our approach?

I think that we need to consider taking more explicit steps to make it expensive to be a drug user. It could be through testing before you get any kind of federal aid. Unemployment compensation, food stamps, you name it.

It has always struck me that if you're serious about trying to stop drug use, then you need to find a way to have a fairly easy approach to it and you need to find a way to be pretty aggressive about insisting--I don't think actually locking up users is a very good thing. I think finding ways to sanction them and to give them medical help and to get them to detox is a more logical long-term policy.

Sometime in the next year we'll have a comprehensive proposal on drugs and it will be designed to say that we want to minimize drug use in America and we're very serious about it.

Since we are in Florida, can you provide an idea of how your administration would handle relations with Cuba?

I think we need a very aggressive model. I describe it as a Cuban Spring. If you have a U.S. government that says Assad should go, why aren't they aggressively saying Castro should go?

Would you open up trade relations with Cuba as president?

It's probably not part of it, but I think you would look at under what circumstance would you change and could you offer the Cuban people. For example, immediately after a free election, all the embargoes would drop as of that day. You could have the carrot of saying, the second there's a free election, we should do everything we can to help the Cuban economy flourish.

President Obama has opened more air travel to the island. Would you shut down those flights?

No, but I would very aggressively move towards maximizing dissent inside Cuba. Mostly covert, and also just subsidies. Go back and look what we did in Poland for example when we aggressively supported Solidarity.

What kinds of items would you subsidize?

You might try to find a way to give virtually every Cuban a free radio. You might want to try to find a way to maximize your ability to broadcast into Cuba so that you have a continuous alternative model of information. Free Radio Insanity I do not care whether Gingrich is speaking figuratively or literally, the idea of free radios is complete nonsense. Exactly would the founders of the constitution think about giving free radios to everyone in another nation? I will tell you what they would think. They would think just as I do, that the proposal is economic insanity as well as foolish intervention into the affairs of other nations. Icing on the Nutcake If you are seeking icing on the nutcake then check out Gingrich's statement on Ron Paul regarding drug usage: " You have to admit, Ron Paul has a coherent position. It's not mine, but it's internally logical." Ron Paul has a logical position. Gingrich doesn't. The war on drugs has been a miserable failure. Gingrich wants to make it an even bigger failure, and a very costly one at that too. Has Gingrich figured out the cost of arresting and imprisoning everyone who sells drugs? The answer is obviously not. Three Questions for Gingrich - How much will it cost to administer drug tests to everyone getting a government subsidy?

- How much more chipping away at states' rights does Gingrich want?

- How can this proponent of big government even call himself a Republican?

Mish Food Stamp Proposal When it comes to food stamps I have a far better set of ideas than drug testing. - Do not let those on food stamps buy frozen pizza, potato chips, snacks of any kind, soft drinks, etc.

- Explicitly limit food stamp users to generic (store brand vs. name brand) dried beans, rice, peanut butter, pasta, canned vegetables, canned soup, soda crackers, fresh vegetables, fresh fruit, frozen (not bottled) juice, poultry, ground beef, chuck steak, bread, cheese, powdered milk, eggs, margarine, and general baking goods (flour, sugar, spices).

- Calculate a healthy diet based on current prices, number in the family, ages of recipients, and base food stamps allotments on that diet.

My proposal will not only lower the cost of the food stamp program, healthy diets would lower Medicaid and Medicare costs as well. Moreover my proposal would give people a strong incentive to get off the food stamp program without intrusive, costly big-brother ideas like drug testing which cannot possibly work for the simple reason that anyone who fails will steal to get food rather than starve. Also note that Gingrich's proposal would harm innocent kids on the program. My idea would help them nutritionally. Given that Gingrich himself admits "Ron Paul has a coherent, logical position" pray tell why can't we try it? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Premature Dollar Obituaries and Mainstream Economists' Monetary Insanity; Keynes-Inspired Great Depression; Lessons Not Learned Posted: 24 Jan 2012 05:02 AM PST A pair of articles by Austrian economist professor Antal E. Fekete just might have one wondering who is more in the loony bin, mainstream economists like Krugman or those consistently chanting about the death of the dollar coupled with hyperinflation. Premature Obituaries Please consider Premature Obituaries It is open season for wild monetary prognostications. More premature obituaries on the dollar have been posted on the Internet. For example, see Jim Willie's The US Dollar Paper Tiger (Gold-Eagle, January 11) with epitaphs like "the U.S. dollar rising to the cemetery", or "dollar death dance". Or see another article, Jeff Nielsen's entitled Maximum Fraud in U.S. Treasurys (Gold-Eagle, January 3). It betrays maximum misunderstanding about keeping the dollar on a life-support system. It assumes that the Fed and the U.S. Treasury are fighting tooth and nail to keep the value of government debt high lest it collapse in want of support from Japan, China, and other countries.

These views hang the picture upside down. In actual fact, the Fed and the U.S. Treasury desperately want to beat down the value of the dollar. The greatest obstacle frustrating their effort is the stubbornly high and still increasing value of U.S. Treasurys. Captains of the world's monetary system are yanking levers and twisting throttles which are no longer connected to anything. The captains are no longer in control. Yet they continue to wave their batons feverishly and pretend that the orchestra is paying attention. They want Jim Willie, Jeff Nielsen and everyone else to believe that the falling interest-rate structure is the outcome of their deliberate monetary policy. In fact, the Fed and the U.S. Treasury are trying to stop the rate of interest from falling further. They instinctively realize the threat of falling interest rates brings deflation and depression in its train. The dollar is much too strong, contrary to the wishes of policy-makers.

It is not so easy to beat down the value of the dollar as suggested by Keynesian textbooks, even if you have the key to print shop where the presses are running. The dollar's strength prevails in spite of the withdrawal of Chinese and Japanese support of the U.S. bond market, and in spite of the destructive monetary policies of the American guardians of the dollar.

This observation reveals the prevailing profound misunderstanding about the nature of this financial crisis. To set the matter right, in this article I shall recapitulate the argument that I have been presenting on the Internet for the past ten years. ....

Like Mises, I also object to the use of the word hyperinflation, albeit for a different reason. It suggests that the phenomenon is linear and follows the laws of the Quantity Theory of Money. The more money is printed, the higher do prices go.

However, we are here facing highly non-linear phenomena. Our economy is torn to pieces by runaway vibration. We are victimized by the self-destruction of the monetary system subjected to oscillating money-flows boosted by the resonance of fluctuating interest rates resonating with fluctuating prices.

The vampire of risk free bond speculation

When the central bank intervenes in the market to control the rise of interest rates, it inadvertently makes prices fall; and when it intervenes to stop prices from falling, it inadvertently makes interest rates rise. The upshot is that the central bank intervention, rather than tempering movements, aggravates them.

At the present junction the Fed is buying bonds to combat deflation. Bond speculators know this, will buy the bonds first, driving down interest rates in the process. The result is more deflation, not less.

The Keynes-inspired central bank action is counterproductive. Policy-makers are blind and don't see this. They stick to their selfdefeating monetary policy. They actually become the quartermaster general of the depression they are trying to avoid. As if cursed by a particular kind of madness, policy makers saddle society with the vampire of risk-free speculation.

The problem cannot be cured because bond speculation cannot be eliminated. It should be clear that as long as the world does not succumb to a military conflagration such as a world war destroying supplies of goods and production facilities, the danger is not inflation as predicted by the Quantity Theory of Money. The danger is deflation due to risk free-profits with which Keynesian economics inadvertently tickles speculators.

The majority of hard-money analysts call for a hyperinflationary collapse of the dollar. Their analysis is faulty. Like a cornered rat, the dollar is capable of putting up a vicious fight for survival. In the words of Mark Twain, all the obituaries on the dollar are premature. The dollar is not a push-over. A yen-yuan coalition (or any other combination of existing or yet to-be-invented fiat currencies) cannot send it into oblivion.

Cheerleaders for fiat money in academic circles, in the media, and in financial journalism will not be able to live down the shame that will be their lot when the world economy collapses. The excruciating economic pain that people will suffer as a consequence will be their responsibility. The break-down in law and order will be their fault. As history and logic conclusively prove, fiat money is not a viable monetary system. It is prone to succumb to the sudden death syndrome. Whether caused by inflation or whether caused by deflation, sudden death is assured.

It should not be beyond the wit of human intelligence to see this coming and fend off the disaster by making a timely return to sound money, based on a monetary unit of a positive value as mandated by the American Constitution. Essential Agreement I am in general agreement with Fekete's analysis but would debate one essential point. The central bank does not want banks to " buy commodities to prevent prices from falling" as Fekete suggests, rather the central bank wants banks to lend. After all, I rather doubt the Fed wants to see oil at $150 or gold at $3000. Instead, the Fed wants banks to lend, businesses to borrow, businesses to hire, and for that cycle to feed on itself. Three Key Points Regarding the US Economy - The US is a credit-based economy.

- Fractional reserve banking is the enabler for unlimited credit expansion.

- In a credit-based economy it is extremely difficult to generate much inflation without an expansion of credit.

Three Conditions Necessary for Credit Expansion. - Banks must not be capital impaired

- Credit-worthy borrowers must want to borrow

- Banks must feel (rightly or wrongly) they have credit-worthy borrowers to lend to

Money Multiplier Theory Fatally Flawed The money multiplier theory to which most if not all hyperinflationists subscribe is horrendously flawed. It assumes just because money is available it will be lent (not only that, but lent 10 times over). Credit-based fiat-systems just do not work that way ever, and it's especially apparent in a debt-deleveraging cycle. Businesses do not want to expand and falling interest rates clobber those on fixed incomes. The rational thing for consumers to do is cut debt. The rational thing for banks to do is buy treasuries. I have been saying this for years to no avail. A recent post Graphical Representations of Bernanke's Effort to Stimulate Bank Lending shows just how hard Bernanke is spinning his wheels. Bernanke tripled money supply in three years and nearly all of it is parked as excess reserves at the Fed. I talked about this recently in an interview on Capital Accounts: Mish on Capital Account Live TV: Discussion of Money Supply, Inflation, the Fed, and SOPA I certainly do not agree with the approach Bernanke is taking, but it is certainly not going to cause hyperinflation. The fact remains that hyperinflation is a political event, not a monetary event. For a discussion of the politics of hyperinflation and some amusing hyperinflation predictions that have failed already please see Hyperinflation Nonsense in Multiple Places Mainstream Economists' Monetary Insanity With that discussion on hyperinflation looniness out of the way, let's turn our attention to Mainstream Economists' Monetary Insanity also by professor Antal E. Fekete. According to Krugman, in spite of the 'false alarm' sounded by the Austrian economists over the debasement of the dollar, inflation is still only 1.5 percent. 'Who could have predicted that so much money printing would cause so little inflation?' he asks rethorically. 'Well, I could, and I did', he boasts, 'because I understand Keynesian economics that Mr. Paul reviles.'

In the event, unknown to Krugman, I also predicted the same thing. Unlike Krugman I did more than simply predicting that inflation was not the danger. I warned that Keynesianism would lead to deflation and depression. Money-printing has become counterproductive. Krugman doesn't understand that it will boomerang. I stated that, unwittingly, Bernanke is the Quartermaster General of the Great Depression II (see: Front-Running the Fed, www.professorfekete.com, February 9, 2010). He doesn't understand the monstrous mistakes prophet Keynes made concerning the role of speculation in the money-creation magic. The fact is that central bank buying makes speculation risk free in the bond market. In comparison, speculative risks in the commodity market appear forbidding. All the speculator has to do in order to reap risk-free profits is to preempt the Fed. He buys the bonds before the Fed has a chance. Then he turns around and dumps them into the lap of the Fed at a profit. The Fed is helpless: it must buy at the higher price. Keynes completely misrepresented the ability of the central bank to stay in charge, given its compulsive drive to suppress interest rates when confronted with a profit hungry pack of bond speculators.

Friedman's analysis of the Great Depression couldn't be more wrong. In 1933 deflation was brought about not by the gold standard but, au contraire, by abolishing it. Here is what actually happened. Roosevelt has removed the only competition government bonds have, gold. The most conservative investors saw their gold confiscated and, willy-nilly, they were forced into the next most conservative instrument, Treasury bonds. Speculators became emboldened and bid bond prices sky high for risk free profits. Had gold been still available, bondholders would have severely punished the speculators for their daredevilry. They would have sold the overpriced bond and stayed invested in gold until bond prices came back to earth from outer space. Then they would have bought their bonds back at a profit.

The same thing is happening all over again. When a central bank increases the monetary base three-fold in three years, this is a clear invitation for bond speculators to move in and make a killing. But what the central bank utterly fails to understand is that, contrary to its hopes, new money is not going to the commodity market. Speculative risks there are far too great. Instead, new money is going to the bond market where the fun is. Bond speculation is risk-free. Speculators know which side the bread is buttered. Krugman doesn't.

Krugman's joy over the supposed defeat of Austrian economics is premature. Bernanke's Fed in blissful ignorance is still putting money in the hands of speculators which they use to place bets on the further fall of interest rates and commodity prices. The day of reckoning comes when falling interest rates destroy capital and, together with it, destroy budding job opportunities. The lethargy of businessmen will continue. They will not start hiring as long as the interest-rate structure is in falling mode.

Welcome to the world of Keynes-inspired Great Depression. I nearly responded to that article by Krugman as well. I too called for record low rates across the entire yield curve and at a time when oil was $140 to boot. Not every Austrian-minded person (I am not an economist) saw things the way Krugman did. However, it is sad to say, most did. In 2010 I feared Krugman would take up Robert Murphy's Debate Challenge and that Murphy would make an inflation is coming soon claim and get blown out of the water. The debate never happened. Recently, Ambrose Evans-Pritchard proclaimed " America Overcomes Debt Crisis". I took Pritchard to task in Debt and Deleveraging: Did the U.S. Overcome the Debt Crisis? Light at the End of the Tunnel Anywhere? Five-Pronged Solution Click on the link for some interesting charts on the global debt problem. Here is my solution presented in the article. Five-Pronged Solution US monetary policy and ECB monetary policy is partially to blame for these crises as Pritchard says. Reckless fiscal policies by governments everywhere is another part of the problem. The five-pronged solution which Pritchard does not mention is ... - Get rid of the central banks

- Get rid of fractional reserve lending

- Return to a gold standard.

- Minimize governments

- Embrace free market policies

Please see Hugo Salinas Price and Michael Pettis on the Trade Imbalance Dilemma; Gold's Honest Discipline Revisited for a discussion of how a gold standard can fix trade imbalances. That solution prompted "halfacunk" to taunt ... " Remember how you said the money-multiplier is a myth? Well, if it is, then we're not using a fractional-reserve system! Please be consistent." My reply was ... FR Lending was the enabler of the debt bubble. It fueled the housing bubble. Lending does not expand because money is available. However, FR allows it to expand without limit when banks want to lend. I am consistent. Once again I see things from the standpoint of credit and Bernanke's failure to get banks to expand credit. Professor Fekete frames the debate a bit differently, but we both came to the same conclusions on front-running bonds, falling yields, and premature obituaries for the dollar. Few in the Austrian camp got this right. The monetarists certainly got things flat out wrong. And as far as Krugman and the Keynesians go, all one can say is the day of reckoning will arrive, yet the exact timing and nature of the ensuing credit crisis is unknown. Lessons Not Learned One might have thought the Monetarists and Keynesians would have learned something from Japan. Instead, and in spite of debt to the tune of 230% of GDP, they came to the amazing conclusion " Japan did not do enough". Two Rules - There is never enough debt to satisfy Keynesians.

- There is never enough fiat currency to satisfy Monetarists.

I confidently predict Japan will have a currency crisis before the US and when it happens I am equally confident Krugman and the Keynesians will make an excuse for it rather than admitting they were dead wrong. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Greek Bondholders Reject Deal; History Lesson on Defaults; The ECB's Dilemma; Deadline Laugh of the Day Posted: 24 Jan 2012 01:37 AM PST Reuters reports Euro zone ministers reject private bondholders' Greece offer Euro zone finance ministers Monday rejected as insufficient an offer made by private bondholders to help restructure Greece's debts, sending negotiators back to the drawing board and raising the threat of Greek default.

At a meeting in Brussels, ministers said they could not accept bondholders' demands for a coupon of four percent on new, longer-dated bonds that are expected be issued in exchange for their existing Greek holdings.

Greece says it is not prepared to pay a coupon of more than 3.5 percent, and euro zone finance ministers effectively backed the Greek government's position at Monday's meeting, a position that the International Monetary Fund also supports.

The aim of the restructuring is to reduce Greece's debts by around 100 billion euros ($129 billion), cutting them from 160 percent of GDP to 120 percent by 2020, a level EU and IMF officials think will be more manageable for the growth-less Greek economy.

Negotiations over what's called 'private sector involvement' (PSI) have been going on for nearly seven months without a concrete breakthrough. Failure to reach a deal by March, when Athens must repay 14.5 billion euros of maturing debt, could result in a disorderly default. World Will Not End There is so much concern over a disorderly default that I am wondering if the market would rally following news the world did not end (just as it hasn't dozens of times before on defaults). Spain has defaulted 15 times before, France 9 times, Brazil 10 times in the last 115 years, Russia 7 times, and the UK 3 times, China 3 times, and India 3 times. The world did not end then and it will not end now. For discussion, dates, and frog tales, please see Princess Merkozy Kisses Frog, Turns into Hopelessly Indebted Club Med Prince; Berlin Ready to See Stronger 'Firewall' History Lesson on Defaults The history lesson ought to be clear by now: If you are going to default (and Greece will - actually it already has - just not in a manner that will trigger a credit event), then do it sooner rather than later. Look at all this needless bickering for years starting with former ECB president Jean-Claude Trichet's insistence "there will be no haircuts". Greece is now on its third haircut. What could have and should have been a 50 billion euro problem in total is now a 200 billion euro problem with another 100 billion euros waiting on deck. Worse yet, the ECB itself is sitting on 40 billion euros of junk (in a self-inflicted wound) wondering what to do about it. The ECB's Dilemma Courtesy of Google Translate and Zeit Online, please consider The ECB's Dilemma Greece in the negotiations to take on debt rescheduling - and even if a voluntary agreement has been reached, the question remains whether enough investors participate in the end, to establish debt sustainability (and only then the IMF will continue to pay money). This raises the question of what to do with their stocks, the European Central Bank in the amount of about 40 billion €.

The answer is: There is no simple solution.

Let us assume that the ECB is involved in a debt restructuring. That would - through reduced distributions from the central bank profits - a burden to taxpayers. And it would ultimately be a form of state funding: The Federal Reserve would have the money made available to Greece. This can be very difficult to reconcile the official justification, that the intervention served only to keep open the monetary transmission channel. Would immediately begin a debate on the risks arising from the purchases of Italian or Spanish bonds. Anyway, it would be difficult for the central bank to defend its bond program arguments.

Let us assume that the ECB is not involved in a debt restructuring. Then you continue the public debate on the program spared - that this program would be less effective. Because de facto central bank would receive the status of preferential creditors, which have fewer resources in the countries concerned for the operation of non-public liabilities. Private investors have to fear that at first the ECB will be served before they have their turn - go on as in the case of Greece the debt section logically deeper in order to achieve a desired debt ratio, if the ECB will cut out. In this case, affect bond purchases by the Fed might not reassuring to investors, but discourages this: Each bond, which the ECB purchases, means greater potential losses for banks and investment companies.

The ECB has a choice: Either your program is not credible - or ineffective. Door Number Three The third option and most likely one is the ECB will get Greece to buy those bonds back at the discount price the ECB paid, making Greece's problem bigger as noted in Limits of Voluntary Deal Hit as Greek Bondholders Draw Line in the Sand; Separating Fact from Fiction in Selective Reporting. Separating Fact from Fiction in Selective Reporting

The proposal is for the ECB to sell its bonds back to Greece so that Greece will then take a hit.

With that in mind, look at this preposterous claim by a senior official "The bonds' rate "is the only issue," said a senior official directly involved in the negotiations. "We have to accommodate the needs of the Greek economy."

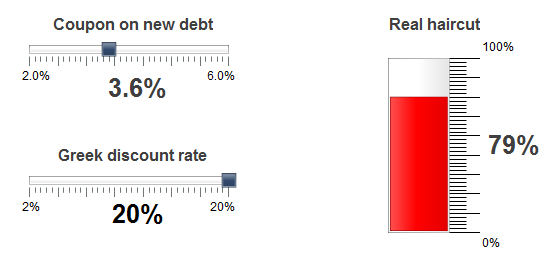

I see two sentences and two lies. Indeed the entire article is crammed pack with lies made by various IIF and EMU officials. Haircut Calculator Revisited Let's go over that Haircut Calculator again. 30 Year Greek Bonds yield 22.5%. Since the calculator tops out at 20% let's assume a discount rate of 20%. Greece and the IMF insist on something under 4%. Let's assume 3.6%. This is what the losses look like.  At 4% with a 15% discount rate, bondholder losses only drop from 79% to 75%. Are the finance ministers really bickering over that feeble percentage difference or are the finance ministers fearing still more losses down the road and would just assume take the total hit now and get it over with? While pondering that question, here is another one to think about. Is Debt to GDP of 120% Sustainable? Reader Andrea from Italy pinged me with this perspective... Hi Mish,

Reading that "The IMF wants to put Greece on a path for a debt-to-GDP ratio of 120 percent by 2020." I could not avoid to think this:

For the sake of comparison, Italy is currently at 120% debt-to GDP ratio, with a much stronger economy than Greece, a better capacity to tackle fiscal evasion (there are huge margins for improvement), a deficit below 3% now and targeted to be 0 by 2013 (let's see if they get there, anyway they will not get extremely far from this), and despite all of this, Italy is a big mess and it is almost impossible for them to get decent rates on the bond market.

So, what they can expect with Greece at 120% debt-to-GDP by 2020? Even a kid can understand that it will never work!

Best regards,

Andrea The IMF and Germany desperately want a deal that will take Greece to a projected debt-to-GDP ratio of 120% by 2020. Why? Even if the plan worked (which it won't) what good would it do? Would someone please put Greece out of its misery? The best chance is a total and complete 100% writeoff right now. Deadline Laugh of the Day Those looking for the laugh of the day can find it in this Bloomberg headline EU to Have No Deadline for End of Greek Talks. For two weeks we heard that a deal had to be reached by Monday (yesterday) or Greece would default. Monday came with no deal, and suddenly there is no need for another deadline. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

No comments:

Post a Comment