Mish's Global Economic Trend Analysis |

- Absurd Threat by Greek Prime Minister: "Hand Over Your Wallet or I Will Give You a Million Dollars"

- Cherry Picking Timeframes on Alleged Leading Indicators; Big Change In LEI on January 26

- Prepare for a Meeting of "Monetary Cardinals" as Euro End-Game Nears; Sarkozy Falling Apart; "Hope Trade" in Extreme Overvaluation

- Graphical Representations of Bernanke's Effort to Stimulate Bank Lending

| Absurd Threat by Greek Prime Minister: "Hand Over Your Wallet or I Will Give You a Million Dollars" Posted: 17 Jan 2012 11:25 PM PST Hedge funds holding credit default swaps on Greek bonds are probably laughing out loud over statements made today by Greek Prime Minister Lucas Papademos. The New York Times reports Greek Premier Says Creditors May Be Forced to Take Losses Taking direct aim at hedge funds and other private holders of Greece's debt, Prime Minister Lucas Papademos says he will consider legislation forcing the creditors to take losses on their holdings if no agreement can be reached in critical negotiations scheduled to resume Wednesday.Laughable Bluff I will post some another snip below, but that is all you need to read to be laughing your head off. If you "force" creditors to take losses, the writedowns can hardly be considered "voluntary" can they? In short, the moment Greece does what Papademos illogically threatens to do, there would be a "credit event" on Greek bonds, exactly what Papademos does not want, and exactly what hedge funds with CDS on Greek bonds do want. Ideally a bluff should carry some measure of risk. Instead, hedge funds are praying Papademos does what he threatens to do. Thus, the Papademos threat is like a robber pointing a gun at you saying "hand over your wallet or I will give you a million dollars". Absurd Statement of the Day Papademos asked Greeks to put their sacrifices in perspective. If all goes well, he said, they could expect "an end to austerity" next year. The only way austerity in Greece will end next year is if Greece defaults. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

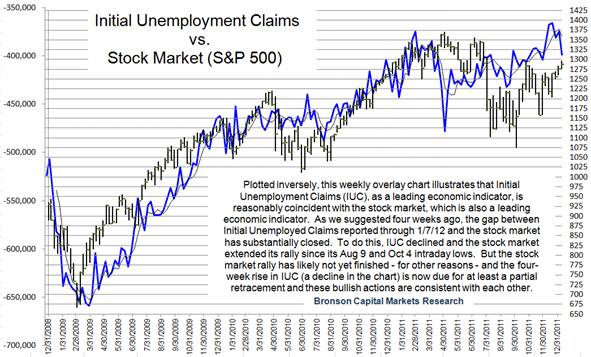

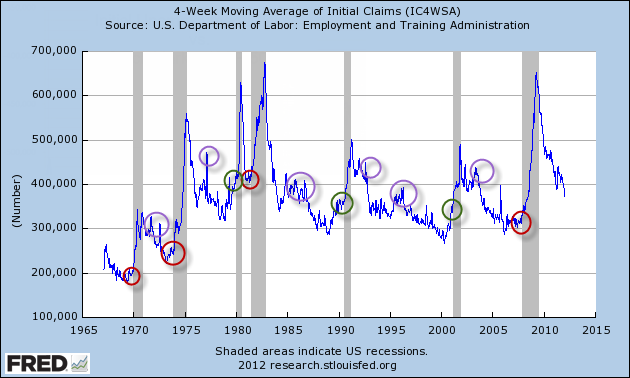

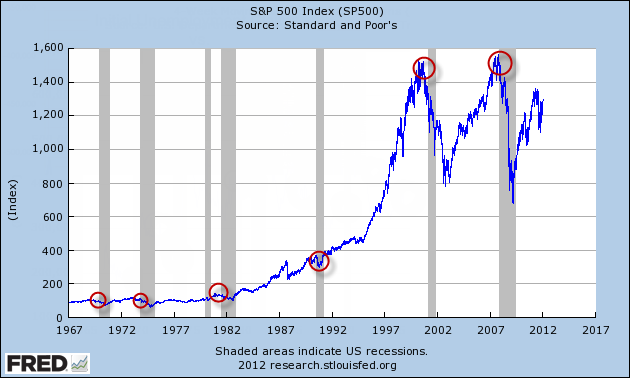

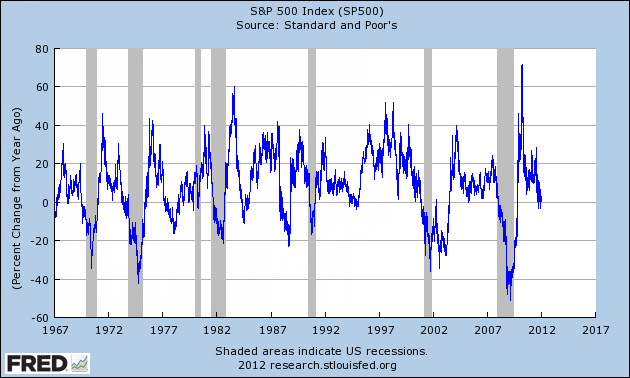

| Cherry Picking Timeframes on Alleged Leading Indicators; Big Change In LEI on January 26 Posted: 17 Jan 2012 02:18 PM PST Bob Bronson makes the claim on the Big Picture Blog that Initial Unemployment Claims Confirm Unfinished Market Rally click on any chart in this post for a sharper image Stock Market vs. Weekly Claims  In addition to other bullish coincident economic data reported yesterday, initial unemployment claims, which are a leading economic indicator, are especially noteworthy. They are a good precursor to the popularly-followed payroll, or jobs, report, a coincident economic indicator.Really? No, Not Really! This is a classic case of picking one tiny timeframe and extrapolating a coincident at best indicator (and possibly even a lagging indicator) into a leading one. Here is proof: Weekly Claims vs. Recessions  Looking at longer-term trends, I count 4 instances in red where weekly-claims was more of a lagging indicator than anything else. A recession started 4 times with weekly claims at or very near the lows. I count 3 recessions in green where a weak case can be made that claims are a leading indicator. However, I can also count six instances in which weekly claims turned up relatively sharply and there was no recession. Unfortunately, Bronson cherry picked not only a timeframe for weekly claims but used it to make the claim that weekly claims are a leading indicator for the stock market which is also a leading indicator for the economy. Stock Market Not a Leading Economic Indicator The stock market is not a leading indicator of the economy. Rather, the stock market is a coincident indicator of sentiment towards equities. S&P 500 vs. Recessions  Far from being a leading indicator, on an absolute basis the S&P has a perfect track record of peaking right before or just as a recession starts. This is just as one might expect from a gauge of equity sentiment which tends to peak right before a downturn in the economy (with everyone extrapolating good times forever into the future). Annualized Percent Change in S&P 500 vs. Recessions  On a percentage change basis, the S&P 500 is not leading, not lagging, and not coincident. Instead it is completely useless mush. Leading Indicators and the Risk of a Blindside Recession John Hussman penned a must-read article on January 9th called Leading Indicators and the Risk of a Blindside Recession Over the past few weeks, investors used to setting their economic expectations based on a "stream of anecdotes" approach have seen their economic views evolve roughly as follows:Warning About Using One Indicator in Isolation Note the key difference between the approach of Hussman vs Bronson. Brosnon extrapolated a coincident (at best) indicator into a leading indicator for the stock market, alleged to be a leading indicator of the economy (which I clearly proved isn't). In contrast, Hussman looks at a broad array of indicators, and the combined analysis in aggregate suggests we will soon be in recession territory. Leading Indicator Battle Here are a pair of charts courtesy of Doug Short and Advisor Perspectives regarding The Great Leading Indicator Smackdown Conference Board LEI  ECRI WLI  ECRI and Hussman vs. LEI I may be wrong, but I side with Hussman and the ECRI, not the LEI. The LEI is way too dependent on the yield curve rather than the direction of the yield curve. The yield curve itself is useless because the lower end is zero-bound. Hussman points out ... Close to half of the weight in the LEI index goes to the two monetary components - the yield curve, and real M2. I suspect that this is a legacy of inflationary business cycles where monetary tightening in response to inflation was the typical event preceding recessions, but it adds noise in the present environment, where the primary economic risks are related to leverage and credit strains.Expect Big Change In LEI on January 26 Please consider Makeup of Leading Economic Indicators Index in U.S. to Change For the first time since 1996, the components of the U.S. leading economic indicator index will change, according to the New York-based Conference Board.At least a portion of the enormous discrepancy between the LEI and the ECRI weekly leading index (WLI) will be resolved to the downside of the LEI on January 26. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 17 Jan 2012 10:36 AM PST Steen Jakobsen, chief economist for Saxo Bank in Denmark, has some very interesting thoughts to share on the sovereign debt crisis in Europe. His six major points are:

Faith in Eurozone Dissipating Fast Please consider More apathy, less austerity - faith in Eurozone dissipating fast written below as a complete guest post in entirety. From Steen ... In my travels to Madrid I made the following observations:Major Agreement I am in essential agreement with all of Steen's points having said the same things on many occasions. I only have a couple small differences. The chart of the S&P does not say much to me. Indeed one can look at various points where indiactors were at extremes and the market kept rising anyway. However, his main point "be nimble and cash-rich now to be able to take advantage of deep discounts coming up later" is 100% spot-on. In regards to Marine Le Pen, I do not know if she is "likely" to defeat Sarkozy in the first round, but certainly EuroSkeptics are on the rise and it is a very reasonable possibility. Regardless, polls show Hollande would beat either Le Pen or Sarkozy, so Sarkozy's days are indeed "likely" numbered. For an analysis of Le Pen, please see

March Polls Le Pen 24% Strauss-Kahn 23% Sarkozy's 20% Strauss-Kahn was forced out over sexual allegations in late Spring. December Polls Round 1 François Hollande 31.5% Nicolas Sarkozy 26% Marine Le Pen 13.5% Francois Bayrou 13% Round 2 François Hollande 57% Nicolas Sarkozy 43% January Polls François Hollande 27% Nicolas Sarkozy 23.5% Marine Le Pen 21.5% Round 2 François Hollande 57% Nicolas Sarkozy 43% Certainly Le Pen has gained much on Sarkozy in just the last month. As Steen commented, the "arrogant Sarkozy is falling apart" and will not win round 2 even if he survives round 1 one on April 22, 2012. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

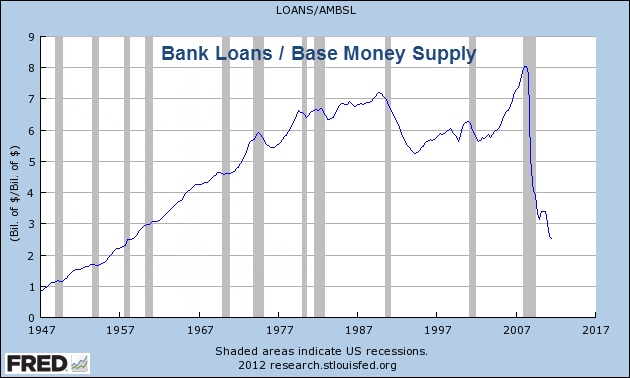

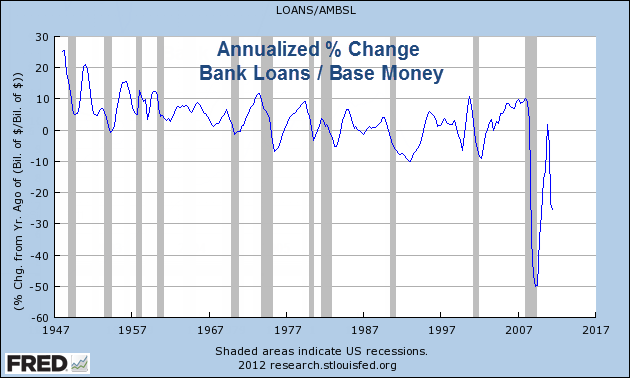

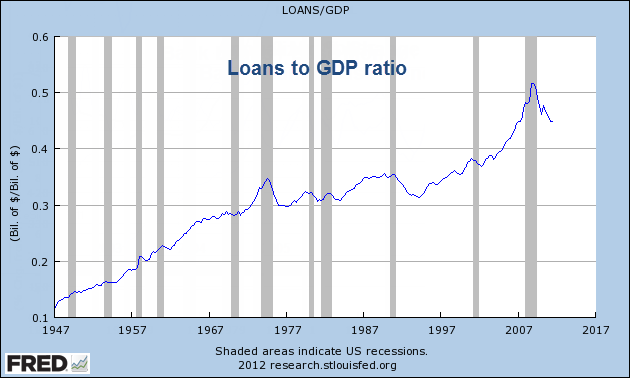

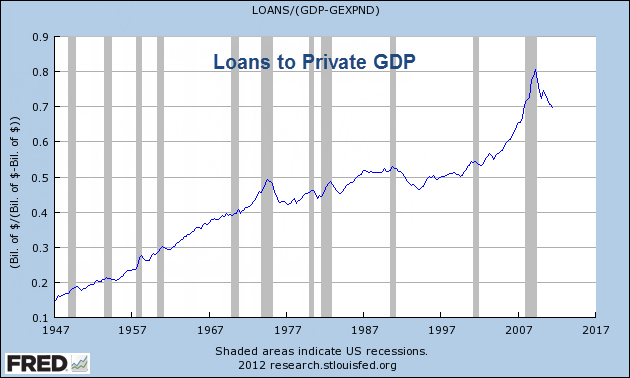

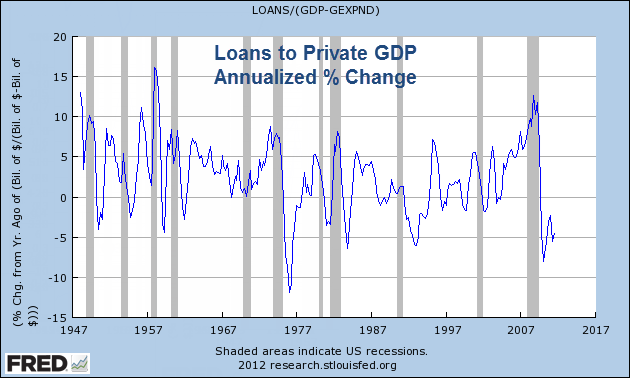

| Graphical Representations of Bernanke's Effort to Stimulate Bank Lending Posted: 16 Jan 2012 11:57 PM PST Bernanke is trying every way he can to get banks to lend (printing coupled with a multitude of lending facilities and Fed programs). It's easy enough to prove the printing: Base money supply is up about $1.8 trillion since the start of the recession. Base Money Supply  Money Multiplier Theory The Money Multiplier Theory (an incorrect theory) suggests this money would be lent out 10 times over causing rampant price-inflation and GDP growth. Alternate (Correct) Bank Lending Theory

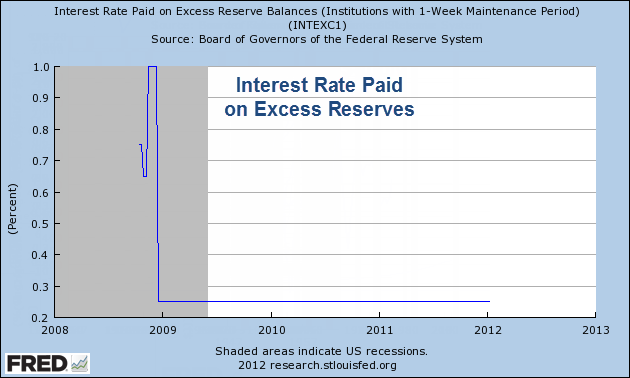

With some charts below created by my friend "BC" let's take a look at Bernanke's efforts to stimulate lending. Bank Loans Divided by Base Money Supply  Annualized Percent Change in Bank Loans Divided by Base Money Supply  Loans to GDP  Loans to GDP Annualized Percent Change  Loans to Private GDP  Loans to Private GDP Annualized Percent Change  M2 Multiplier: M2 Money Supply Divided by Base Money  M2 Velocity: GDP Divided by M2  The above charts show that it is taking more and more money just to keep the economy afloat. US deficit spending is $1.4 trillion dollars, Bernanke is flooding banks with cash, interest rates are at record lows, mortgage rates are at record lows, and velocity of money is falling like a rock. Excess Reserves  Of the $1.8 trillion Bernanke has added to base money supply since the start of the recession, nearly all of it is sitting parked at the Fed as excess reserves. Interest Paid on Excess Reserves  As you can see, banks have parked close to $1.6 trillion with the Fed earning .25 percent annually. This is free money to the banks to the tune of $4,000,000,000 per year for doing nothing. In short, banks would rather have $4 billion in free money at a measly .25 percent than make much more money by lending it out. This indicates two things:

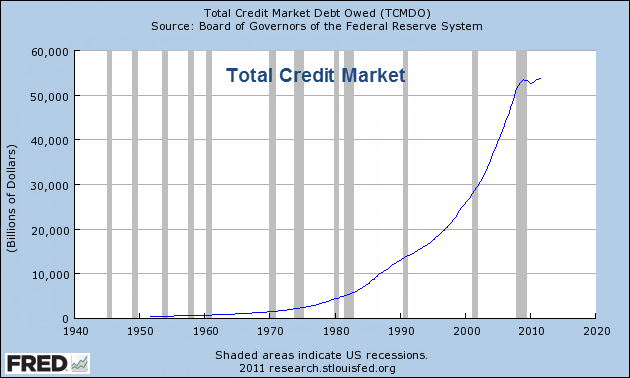

If and when banks do start lending, it will not be because all those excess reserves have tempted them. Rather it will be because banks feel they have credit-worthy borrowers. In the meantime, debt deflation rolls on, distorted of course by global central bank stimulus everywhere one looks, notably (the Fed, ECB, China, Bank of England) and coming up shortly, the Bank of Japan. As I have stated before, competitive global currency debasement is a good environment for gold. Let's wrap this up with one final chart. Total Credit Market  As you can see the total credit market is well over $50 trillion. Yet a large number of misguided souls believe printing $1.8 trillion of which $1.6 trillion is parked as excess reserves will cause hyperinflation. It won't. Hyperinflation is a political event, not a monetary one. Besides, the US has more gold than any other nation. For further discussion, please see Hyperinflation Nonsense in Multiple Places. Yes, the US is going to have a "debt moment", just as Europe is having one now and Japan will have soon enough. However, that moment may be quite a long ways away (or not), but hyperinflation will not be the result when it happens. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment