Mish's Global Economic Trend Analysis |

- Is it Acceptable to Present a $196 Billion Sac-O'-Sheet to Sophisticated Investors as Diamonds-in-the-Rough?

- 2-Year, 10-Year Treasury Yields at Record Lows; Greek 1-Year Yield Tops 72%; Gold Soars $56 to $1882; Bill Gross Anticipates "Twist Again"

- Global Recession, Right Here, Right Now: Japan's Capital Spending Plummets; Eurozone PMI, UK PMI, US ISM ex-Inventory, China Exports in Contraction

- Italy Backs Down on Austerity Measures; Bank of Italy Warns Tax Hikes Needed; German Central Bank Complains EU Treaty "Completely Gutted"

- Zero Jobs Growth, Unemployment Rate Flat at 9.1%; Charts, Graphs, Details

| Posted: 02 Sep 2011 10:42 PM PDT The FHA has filed a $196 Billion lawsuit against 17 banks accusing said banks of "misleading Fannie Mae and Freddie Mac about the soundness of the mortgages underlying the securities". Inquiring minds note BofA, JPMorgan Among 17 Banks Sued by U.S. for $196 Billion. Bank of America Corp. and JPMorgan Chase & Co. (JPM) were among 17 banks sued by the U.S. to recoup $196 billion spent on mortgage-backed securities bought by Fannie Mae and Freddie Mac.Lawsuit Claims Please consider FHFA Sues 17 Firms to Recover Losses to Fannie Mae and Freddie Mac The Federal Housing Finance Agency (FHFA), as conservator for Fannie Mae and Freddie Mac (the Enterprises), today filed lawsuits against 17 financial institutions, certain of their officers and various unaffiliated lead underwriters. The suits allege violations of federal securities laws and common law in the sale of residential private-label mortgage-backed securities (PLS) to the Enterprises.$196 Billion Sac-O'-Sheet The 17 banks are from the FHA filing, the amounts above are from the Bloomberg article. Please note the Deutsche Bank defense: "Fannie Mae and Freddie Mac are the epitome of a sophisticated investor." The DB defense has me asking a pair of questions

The answer to question number 1 is "of course". I am not a lawyer, but I believe the heart of the matter is question number 2. More explicitly, did the banks violate disclosure laws in submitting loans to Fannie and Freddie. I believe the banks not only did so, but purposely and blatantly did so. Bank of America Extremely Exposed Note the Bank of America exposures, and the accompanying Bank of America stock weakness. 2. Bank of America Corporation - $6 billion 5. Countrywide Financial Corporation -$26.6 billion 13. Merrill Lynch & Co. / First Franklin Financial Corp. - $24.8 billion Where is Wells Fargo? By the way, where is Wells Fargo? Is Wells Fargo lily white and if so was is it because they were stupid enough to hold all the mortgage paper themselves? Final Thoughts The FHA took its sweet time filing this lawsuit. I believe purposely so. They have had all the time in the world to gather evidence and make a case. This is a serious case, and Fannie and Freddie have subpoena power. That subpoena power gives the FHFA a big advantage over private investors notes the Wall Street Journal in Big Banks Face Suits on Mortgage Bond Losses Bank of America is scared to death and rightfully so. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 02 Sep 2011 03:35 PM PDT Curve Watchers Anonymous is watching the US Yield Curve once again. Treasuries soared today (yields plunged) on the "unexpected" news the economy created no jobs. Yield Curve as of 2011-09-02  click on chart for sharper image $TYX : 30-Yr Treasuries $TNX : 10-Yr Treasuries $FVX : 05-Yr Treasuries $IRX : 03-Mo Treasuries 10-yr treasuries touched a record low on Friday. The entire yield curve from 3 months to 10 year is at or near record lows. The 30-year long bond is lowest since January 2009. Greek One-Year Yield Soars to 72%  One year yield in Greece is pricing in a certain default with a big haircut to boot. Bill Gross Anticipates "Twist Again" Having missed nearly the entire treasury rally (see Recession Looms in Brazil and Canada; Asia Exports Sink; Global Economy Deteriorates Rapidly led by BRICs; Asia Stagflation; PIMCO Admits Mistake), Bill Gross now likes "longer harder duration". Please consider Gross Extends Maturities on Bet Fed to Embrace Operation Twist Pacific Investment Management Co.'s Bill Gross said he favors longer-maturity debt with the Federal Reserve likely to seek to narrow the difference between short- and long-term borrowing rates as employment growth stagnates.Twist Again Useless at Best I frequently disagree with El-Erian but not this time. The 10-Year yield is under 2%. What practical reason can their possibly be and what practical benefit could possibly result from the Fed attempting to drive yields lower? The answer is none, but monetarist clowns still call for the Fed to do just that. Gold Approaches Record High  It's time to face the facts Fed monetary stimulus is now useless at best. It's also time to face the facts the rally in gold has little if anything to do with inflation. Gold is clearly reacting to further stimulus efforts by the Fed, Eurozone bank stress, or US bank stress. It is always difficult to say "why" something is happening but in this case, bank stress in both the Eurozone and the US is the likely reason for the renewed push higher. Gold may become even more volatile as the ECB and IMF attempt more futile efforts to "save the Euro". These foolish efforts to "save Greece" (in reality save stupid European banks that made foolish loans to Greece) has tripled or quadrupled the pain those banks are going to feel. What may initially have been a 40 billion Euro boondoggle now likely approaches a 150 billion Euro boondoggle and the EU wants to throw yet another 100 billion Euros at it. In the meantime, Italy looks prepared to blow again. How much more of this will citizens of Germany, Finland, and Austria put up with? How much austerity can citizens of Greece, Spain, Portugal, and Italy take? This can easily come to a crisis head as soon as next month, or even next week. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 02 Sep 2011 10:41 AM PDT It's time to stop debating whether or not the US or Europe is headed into recession. The facts show the entire global economy is in recession. Global Recession Supporting Data-Points

Ten Things to Remember

Additional Reads Talk of avoiding recession when the global economy is clearly in one and fundamentals are horrendous is sheer lunacy. In case you missed them, please consider ....

http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 02 Sep 2011 10:28 AM PDT In the wake of fresh sex and bribe scandals of Italian Prime Minister Silvio Berlusconi as well as Italy's backing down on austerity measures, interest rates are once again creeping back up on Italy. 10-Year Italian Government Bond Yields  Italy Drops Plan to Tax Higher Earners From Austerity Bill Bloomberg reports Italy Drops Plan to Tax Higher Earners From Austerity Bill Prime Minister Silvio Berlusconi's government has dropped a planned bonus tax on Italians earning more than 90,000 euros ($131,000) a year from a package of austerity measures that aims to balance the budget in 2013.Revenue Replaced in Unknown Way Allegedly the revenue will be replaced in an unannounced, unknown way. Does anyone believe that? Bank of Italy Warns Tax Hikes Needed The Washington Post reports Bank of Italy warns government's new austerity measures must raise taxes, cut spending The Bank of Italy warned Tuesday that the government's revamped austerity plan must not cut back on its original €45.5 billion ($65.9 billion) proposal to raise taxes and cut spending — and said even with the plan Italy risked economic stagnation.Phase of Recession Not Stagnation I remain in awe of cental bank ability to tell bald-faced lies. The idea that Italy will grow in 2011 and 2012 in the face of a global recession with additional austerity measures is nonsensical. German Central Bank Complains EU Treaty "Completely Gutted" The Telegraph reports EU law "gutted" by bail-outs, growls Bundesbank Jens Weidmann, the bank's president, said monetary union risks losing its democratic legitimacy as EU leaders take a "large step" towards a debt union without legal authority, and sever the crucial link between budget policy and elected parliaments.Riot Act Julian Callow, Managing Director and Chief European Economist for Barclays Capital suggests "Trichet to go to Rome to read the riot act." There will be a riot act alright, and it will come when the people of Greece, Spain, Italy, and Ireland have had enough of austerity measures aimed at bailing out foreign banks. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

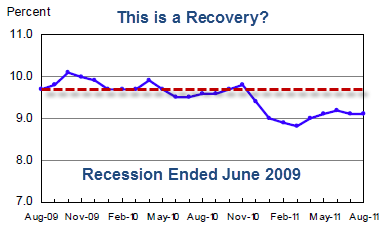

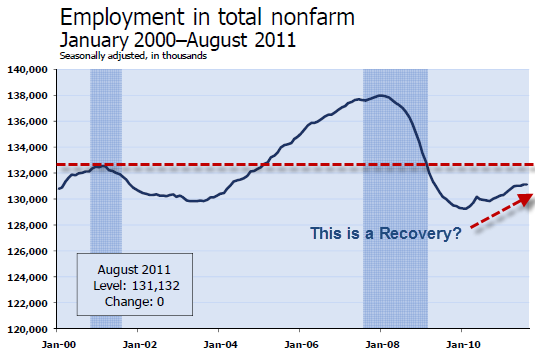

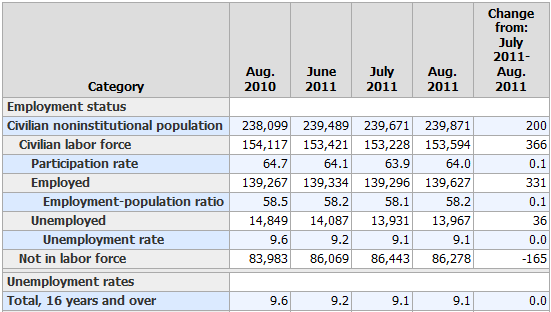

| Zero Jobs Growth, Unemployment Rate Flat at 9.1%; Charts, Graphs, Details Posted: 02 Sep 2011 08:27 AM PDT Jobs Report at a Glance Here is an overview of today's numbers.

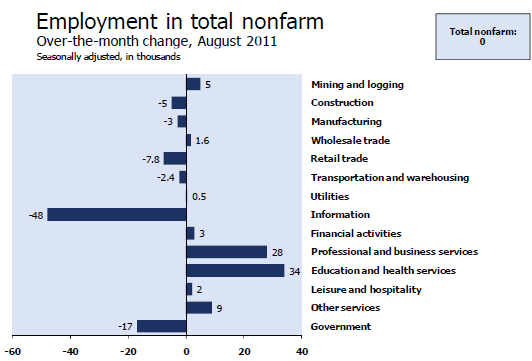

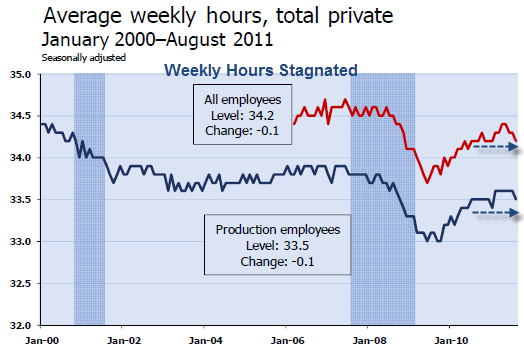

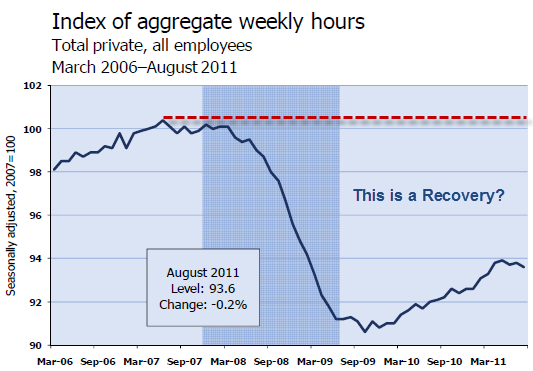

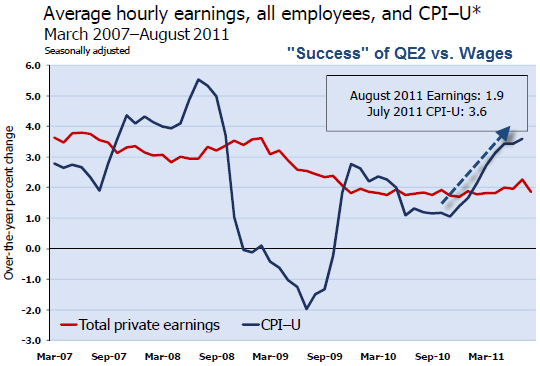

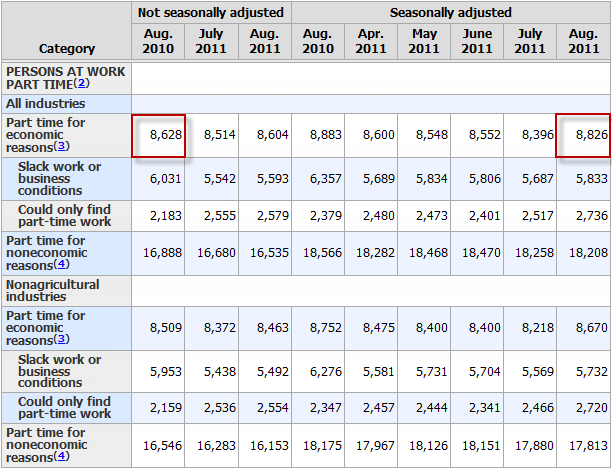

Recall that the unemployment rate varies in accordance with the Household Survey not the reported headline jobs number, and not in accordance with the weekly claims data. For a change, the labor force actually rose today. This is a welcome sign. However, were it not for people dropping out of the labor force for the past two years, the unemployment rate would be well over 11%. August 2011 Jobs Report Please consider the Bureau of Labor Statistics (BLS) August 2011 Employment Report. Nonfarm payroll employment was unchanged (0) in August, and the unemployment rate held at 9.1 percent, the U.S. Bureau of Labor Statistics reported today. Employment in most major industries changed little over the month. Health care continued to add jobs, and a decline in information employment reflected a strike. Government employment continued to trend down, despite the return of workers from a partial government shutdown in Minnesota. Unemployment Rate - Seasonally Adjusted  Nonfarm Employment - Payroll Survey - Annual Look - Seasonally Adjusted  Notice that employment is lower than it was 10 years ago. Nonfarm Employment - Payroll Survey - Monthly Look - Seasonally Adjusted  click on chart for sharper image Between January 2008 and February 2010, the U.S. economy lost 8.8 million jobs. Ignoring the effects of the census, in the last 11 months of a recovery 2+ years old, the economy averaged about 117,000 jobs a month. That is very poor as recoveries go. In the last 4 months the economy has averaged 40,000 jobs a month, a downright pathetic number. Statistically, 127,000 jobs a month is enough to keep the unemployment rate flat. Nonfarm Employment - Payroll Survey Details - Seasonally Adjusted  Average Weekly Hours  Index of Aggregate Weekly Hours  Average Hourly Earnings vs. CPI  "Success" of QE2 Over the past 12 months, average hourly earnings have increased by 1.9 percent. The Consumer Price Index for All Urban Consumers (CPI-U) was up 3.6 percent over the year ending in July. Not only are wages rising slower than the CPI, there is also a concern as to how those wage gains are distributed. BLS Birth-Death Model Black Box The BLS Birth/Death Model is an estimation by the BLS as to how many jobs the economy created that were not picked up in the payroll survey. The BLS has moved to quarterly rather than annual adjustments to smooth out the numbers. For more details please see Introduction of Quarterly Birth/Death Model Updates in the Establishment Survey In recent years Birth/Death methodology has been so screwed up and there have been so many revisions that it has been painful to watch. The Birth-Death numbers are not seasonally adjusted while the reported headline number is. In the black box the BLS combines the two coming out with a total. The Birth Death number influences the overall totals, but the math is not as simple as it appears. Moreover, the effect is nowhere near as big as it might logically appear at first glance. Do not add or subtract the Birth-Death numbers from the reported headline totals. It does not work that way. Birth/Death assumptions are supposedly made according to estimates of where the BLS thinks we are in the economic cycle. Theory is one thing. Practice is clearly another as noted by numerous recent revisions. Birth Death Model Adjustments For 2011  BLS Back in Outer-Space Do NOT subtract the Birth-Death number from the reported headline number. That is statistically invalid. However, in my estimation the BLS is back in outer-space. It is clear the economy is slowing and the BLS model has not picked it up. The model is horrendously wrong at economic turns. -18,000 may look reasonable but bear in mind that January and July are revision months where the BLS adjusts for prior errors. I believe the BLS has missed another economic turn, and the BLS is terribly wrong following turns. Household Data  click on chart for sharper image In the last year, the civilian population rose by 1,772,000. Yet the labor force dropped by 523,000. Those not in the labor force rose by 2,295,000. Were it not for people dropping out of the labor force, the unemployment rate would be well over 11%. Table A-8 Part Time Status  click on chart for sharper image There has been no improvement in part-time employment in a full year. 8.8+ million workers want a full time job and cannot find one. Table A-15 Table A-15 is where one can find a better approximation of what the unemployment rate really is.  click on chart for sharper image Distorted Statistics Given the total distortions of reality with respect to not counting people who allegedly dropped out of the work force, it is hard to discuss the numbers. The official unemployment rate is 9.1%. However, if you start counting all the people that want a job but gave up, all the people with part-time jobs that want a full-time job, all the people who dropped off the unemployment rolls because their unemployment benefits ran out, etc., you get a closer picture of what the unemployment rate is. That number is in the last row labeled U-6. While the "official" unemployment rate is an unacceptable 9.1%, U-6 is much higher at 16.2%. Things are much worse than the reported numbers would have you believe. Moreover, the unemployment rate is barely better than it was a year ago. It would actually be worse than a year ago were it not for people dropping out of the labor force. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment