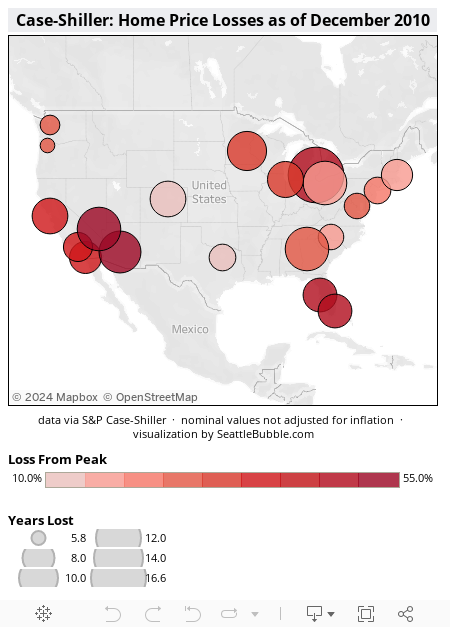

Tim Ellis at the Seattle Bubble blog sent me an email along with an interesting map of data on Case Shiller 20 metropolitan housing market index in Tableau form. Please give the table a few seconds to load.

HousingPanic, a particularly vitriolic BubbleBlog — which is saying something — asks: Realistically, how overvalued are Phoenix home prices?

Obviously, I consider this a profoundly silly question, but to lurk among the BubbleBloggers and their seething commentariat is to acquire an education in a slice of America invisible from this side of the sewer gratings. Notwithstanding the idiotic economic analysis, which is really no worse than the static-market fallacies paraded as profundities in the pages of the Arizona Republic, these sites — and not just HousingPanic — are infested with a cult-like fever to inflict suffering — at second hand, to be sure — on people who are in fact guilty of nothing except failing to have drunk the BubbleBlogger KoolAde.

That's all one. I don't care. The whole of the last century was dominated by the bad behavior of viciously angry wretches, but look where it got them. The BubbleBloggers will someday bawl balefully in private, but they will never, ever admit that they have been very publicly very foolish. You will know and I will know and in the secret chambers of their hearts they will know they were wrong all along. But as long as you don't hold your breath waiting for that contrite admission of error, you should be fine.

Here's where I do start to care. Whenever the subject of Phoenix comes up in a BubbleBlog, the assembled Brown Shirts pile on, for whatever reason. ...

Which brings me back to HousingPanic's question. We keep our own home sales price statistics, so we have no doubt that values are down from their high in December. How much? Right now, about 4%. Could they go lower? Certainly. Will they drop by the huge amounts HousingPanic and his flying monkeys seem to yearn for? This seems very unlikely.

What seems much more likely is that Phoenix will recover from the hangover of last year's buying binge and get back to a steady rate of growth — historically 6% a year. The reason this should happen is very simple: Population growth. ...

Greg Swan, super Phoenix bull drones on with 21 preposterous reasons why Phoenix will not crash. All of his reasons were rebutted at the time and in detail by myself and others so many times and in so many places, I could fill up pages listing them.

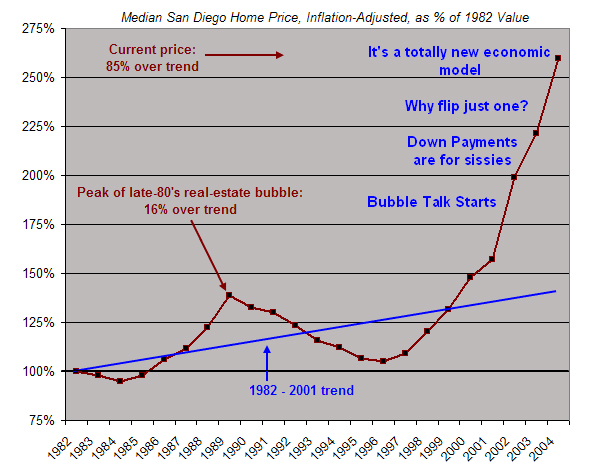

To name a single name, Professor Piggington was among the first with a complete analysis, not of Phoenix per se, but a thorough, and sound analysis why the population argument did not hold up.

The first chart above is mine. I added the annotations on the second chart, created by Professor Piggington.

Here is my favorite quote at the time.

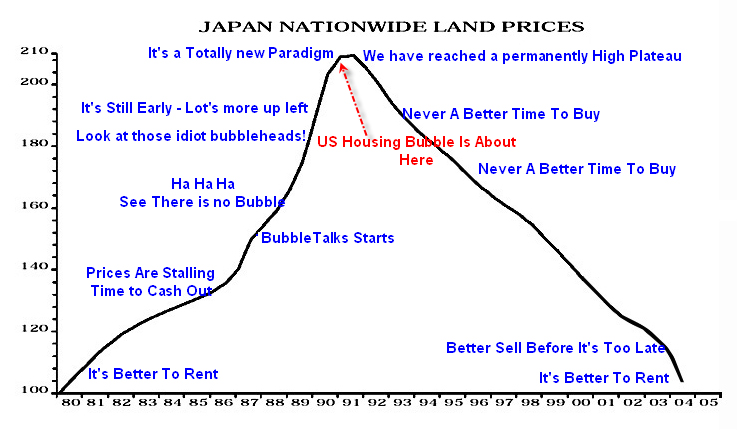

Gregory J. Heym, the chief economist at Brown Harris Stevens, is not sold on the inevitability of a downturn. He bases his confidence in the market on things like continuing low mortgage rates, high Wall Street bonuses and the tax benefits of home ownership."It is a new paradigm" he said.

We now have the truth. It was not a "new paradigm". Price-to-rent and price-to-wage matters.

Doug Swan "Notwithstanding the idiotic economic analysis, which is really no worse than the static-market fallacies paraded as profundities in the pages of the Arizona Republic, these sites — and not just HousingPanic — are infested with a cult-like fever to inflict suffering — at second hand, to be sure — on people who are in fact guilty of nothing except failing to have drunk the BubbleBlogger KoolAde. ... Right now, [prices are about 4% lower]. Could they go lower? Certainly. Will they drop by the huge amounts HousingPanic and his flying monkeys seem to yearn for? This seems very unlikely."

Who's the Flying Monkey?

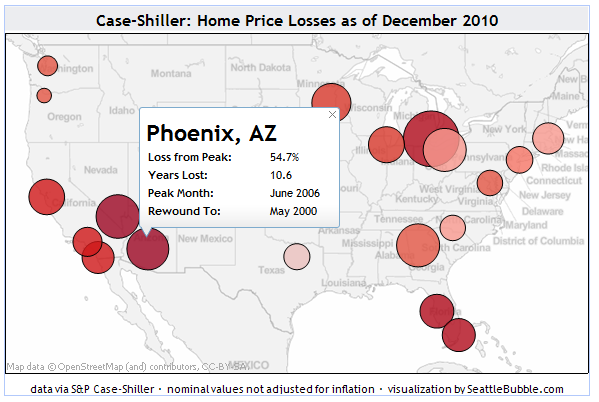

It was Greg Swan's idiotic self-serving economic analysis and hype that helped lure dumb speculators into "can't lose" Phoenix. Prices are now 54.7% off the peak in June 2006.

Greg Swan called housing bears "flying monkeys" right as his area peaked. I believe congratulations are in order. It's not easy to be that boldly inept.

You nailed it on the CDs. I just got done with an FDIC exam and they requested shock testing 400 basis points up and nothing down. Hard to go below zero.

In terms of 5 to 7 year CDs a 15 year GNMA is probably a better way to go. Don't buy them at a premium and look at average life of 4 to 5 years. They are zero risk based as well.

Anyway nice job I could not agree with you more.

Here is a snip from my post regarding new borrow-short lend long schemes. Refer to the link at the top for a discussion of absurdly low CD rates offered by Bank of America and Citigroup, or for the full discussion about the duration mismatch problem banks are getting themselves into.

The Next Borrow-Short Lend-Long Guaranteed to Blow Scheme

Banks are setting aside billions of dollars to do something that until now was rarely heard of: making big loans to cities, states, schools and other public borrowers that otherwise might have turned to the bond market.

When Riverside, Calif., was ironing out a bond offering recently to expand its performing-arts center, several banks pitched a radical idea: Why not take out a loan instead? The city scrapped the bond plan and borrowed $25 million from City National Bank in Los Angeles.

"This was a method we'd never even heard of before," says Scott Catlett, the city's assistant finance director. He says Riverside now intends to seek a bank loan for a conference center that it had planned to build with bonds.

J.P. Morgan Chase & Co. is devoting billions of dollars to direct loans this year to both refinance deals and for new projects, according to a bank official. Last year, the bank made a few hundred million dollars of direct loans to municipalities. Now, the bank would consider making a single loan for hundreds of millions of dollars, the official said. It also is dispatching teams to explain the concept to wary public borrowers.

Citibank also is courting municipal borrowers with direct loans, according to several bond issuers. A spokesman for the Citigroup Inc. unit declined to comment.

"This used to be unheard of," says Eric Friedland, managing director of public finance at Fitch Ratings, noting that in the past, banks would occasionally loan a municipality less than $1 million to finance projects too small for a bond offering. For bigger loans, they would form a syndicate with other lenders.

It remains to be seen what land mines may be lurking for lenders and borrowers. Some municipalities are going through significant struggles, raising questions about whether they will prove good credits. And direct loans are less liquid, meaning banks can't sell them as easily as bonds.

For banks, this is a potentially lucrative business at a time when they are sitting on cash that isn't earning huge interest and are reluctant to make loans for mortgages and other areas they see as risky.

In the event of a bankruptcy, analysts say, it is unlikely that a bank extending a direct loan would be given priority over bondholders.

The city saved hundreds of thousands of dollars in issuance costs, says Mr. Catlett, the assistant finance director. Plus, he says, the interest rate is 3.85% versus at least 5% if it had floated a public offering. The term is slightly lower—21 years versus perhaps 30 years in the bond market.

"This was all new to us," he says. "I don't know now when we'll go back to the bond market. This is easier."

Fed or FDIC Should Stop this Fraudulent Scheme Now

The Fed or FDIC should step in right now. There is no way banks can secure cost of funds for 21 years for 3.85%. Moreover, the risk of default is hardly zero, and banks will not be first in line should default happen.

I think borrowing-short and lending-long is fraudulent. How can you lend something for 21 years when you only have the right to use it for 3, 5, or 7?

Want to know what those banks thinking? This is what ....

They are too big too fail

The Fed will bail them out

Cities won't default but who cares anyway because the Fed will bail them out

They have a hot pile of cash the Fed crammed down their throats at 0% and they want to put it to use

They got burnt badly on mortgages and home equity loans so they need to find something new

One idiot bank made an absurdly risky deal so like sheep they all want to do it

Right now they are all thinking there is nothing to lose from this. The Fed or Congress will bail them out at taxpayer expense if they get in trouble.

Then, when this does get out of control and blows sky high, they will all scream, "no one could possibly have seen it coming".

I's now official. Japan's demographic time bomb has gone off. However, don't look for a big crater, at least just yet, because this has started off with a whimper and not a bang.

Japan's public pension fund, the world's largest, said it may become a net seller of bonds to cover payments in the world's most rapidly aging society.

The Government Pension Investment Fund, which oversees 117.6 trillion yen ($1.4 trillion), in September forecast that it would sell 4 trillion yen in assets in the business year ending March 31 to fund payouts. Sales may be less than that in the year starting April as bonds reach maturity, said Takahiro Mitani, president of the fund, known as GPIF.

"We will likely be a net seller in the market," Mitani, a former executive director at the Bank of Japan, said in an interview in Tokyo yesterday. "We certainly have to come up with an adequate amount" to pay pensions, he said, declining to elaborate on the amount.

Sales by the fund, which helps oversee public pension funds for Japan's 37 million retirees, come as the first of Japan's baby boomers is set to turn 65 in 2012, making them eligible for pension payments.

The GPIF, historically one of the biggest buyers of Japanese debt, held 82.4 trillion yen in domestic bonds, or 70 percent of its assets, as of September, according to the fund's latest quarterly financial statement. That compares with 12.6 trillion yen in Japanese stocks, or 10.7 percent, 9.6 trillion yen, or 8.2 percent, in foreign bonds and 11.5 trillion yen, or 9.7 percent, in overseas stocks, the report shows.

GPIF doesn't plan to start investing in so-called alternative assets such as commodities, real estate, infrastructure, private equity or hedge funds because the risks don't suit its strategy, Mitani said. 'Too Early'

"It's too early to get into alternative investments now," Mitani said. "Japanese investors are conservative and it's hard to justify to the public investing in asset classes such as commodities, real estate and hedge funds."

Japan's 10-year bond yield is the lowest in the world, data compiled by Bloomberg show. Japan's gross domestic product shrank an annualized 1.1 percent in the three months ended Dec. 31, the Cabinet Office said on Feb. 14, and China's economy overtook Japan's as the world's second largest for 2010.

People aged 65 or older will account for 29 percent of the country's population in 2020 and almost 40 percent in 2050, according to the statistics bureau. They accounted for 23 percent population at the end of 2010, the highest among the Group of Seven countries, data compiled by Bloomberg show. That compares with 12 percent in 1990.

Japanese pension funds posted the lowest annualized growth among 12 countries between 2004 and 2009, at 2 percent in U.S. dollar terms and unchanged in yen terms, according to the survey. Brazil reported the highest growth, 24 percent in dollars, the report showed.

Thoughts and Implications

There is not going to be a huge exodus of Japanese bonds anytime soon. However, the world's largest fund has gone from being a buyer of bonds to a seller of bonds. The amount is not trivial.

82.4 trillion yen in domestic bonds is about 1 trillion in US dollars. That is a lot of pent-up supply, especially when the government is running an annual deficit of of about $240 billion with no external buyers at all.

Those factors put huge long-term upward pressures on interest rates.

Deflation Irony

The irony in this madness is that all the Japanese people want is their money back. They are not looking for appreciation. They do not have absurd pension plan assumptions like the 8% expected returns we see in the US. They do not want stocks, or real estate. They just want cash, and they want it to be worth something.

Yet, the Japanese government was hell-bent for two decades attempting to generate inflation which would have weakened the value of those bonds.

Recently, those bond holdings have been rising with a strengthening yen. However, lingering debt from preposterous deflation fighting efforts of building bridges to nowhere must be paid back.

Horns of a Dilemma

Japan choices are to default on its debt, print money to fund interest on the debt, raise taxes effectively robbing savers of their money, or undertake huge spending cuts.

The dilemma stems from years of Keynesian and Monetarist stupidity.

Japan's government pledged to balance the nation's main budget over the coming decade under its first fiscal-overhaul plan, approved Tuesday, laying the groundwork for the daunting task of tackling the country's massive debt.

Highlighting the challenge of such an undertaking, the government estimated that if growth remains modest, it may have to fill an annual budgetary gap of about 22 trillion Japanese yen (US$242 billion) by the fiscal year ending March 2021. If Tokyo were to raise that amount only by increasing the 5% consumption tax—one gauge being used—it would need to increase the tax nearly threefold.

Prime Minister Naoto Kan's government will kick off the fiscal-reform campaign by capping annual spending for the next three fiscal years and keeping new government bond issuance below 44.3 trillion yen next fiscal year. The debt amount is estimated the same as in the current fiscal year that started in April. Tokyo also promised to make "utmost efforts" to lower the amount in the following years.

The budgetary blueprints represent the first fiscal-reform plans adopted by the Democratic Party of Japan since it swept to power about nine months ago. They offer the clearest picture yet of how Mr. Kan's economic team intends to lower the nation's public-debt level, which at nearly twice Japan's yearly economic output is the worst among advanced economies.

Japanese government bonds rose as investors welcomed the plan. Lead September JGB futures finished the day up 0.34 at 140.82, while the 10-year JGB yield fell to 1.185%, its lowest level since January 2009.

But questions linger about feasibility of the framework. Absent from the blueprint are detailed spending-cut plans, such as how much to scale back individual budget categories like defense and education. There also aren't timetables for specific tax increases despite Mr. Kan's calls for doubling Japan's consumption tax in the coming years.

"The government has yet to provide details of how it can achieve the goal," said Masashi Shimominami, a bond-market analyst at Mizuho Securities. Some investors also remain skeptical over whether Mr. Kan will rally enough political support for heavier taxes on consumption, Mr. Shimominami said.

The release of the plan comes as Japanese officials shift their policy focus to fixing budgetary woes after receiving a wake-up call from Europe's deepening debt crisis. "We must make sure we avoid a situation where we lose trust in the government bond markets just like Greece and, as a result, interest rates rise sharply, putting our finances in a state of default," the guidelines said.

No Political Will For Budget Cuts

As in the US, there is no political will for budget cuts. The best the government could come up with was a plan to freeze spending for 3-years. Whoop-to-do. Bear in mind that an aging demographic will require more health care.

Will growth be sufficient to make a long-term dent in Japan's debt? I scoff at the notion. Moreover, rising energy prices will take a big bite of of Japan's trade surplus.

By the way, in case you missed it, Japan's trade surplus went negative last month. Supposedly it's a one-time thing.

Japan posts first trade deficit in almost two years

Weaker exports to key markets gave Japan its first trade deficit in 22 months, Ministry of Finance data has shown.

The trade deficit was 471.42bn yen ($5.7bn; £3.52bn) in January, with exports up 1.4%. Analysts had expected export growth to be closer to 7%.

Japan has struggled to boost exports as a stronger yen dents demand.

It recently lost its position as the world's second-largest economy to China. Changing scenario?

However, analysts said they expect exports to rebound.

That should help drive economic growth in Japan, albeit at a pace that is slower than many experts may have predicted.

One of the main reasons for the slower growth was weaker demand from China, where the government is battling inflation and signs that its economy may be overheating.

Japan is counting on increased sales to China when China is clearly overheating and will have to cut back. How do you think that fantasy is going to work out?

So, it's back to tax hikes. To do it all with tax hikes, Japan would need to hike the VAT by 200%, from 5% to 15%. Is that going to fly with the voters?

Nonetheless, let's assume Japan does hike taxes. Those tax hikes would strengthen the yen, which in turn would hurt Japan's export growth and corporate profits.

My suspicion is Japan will print money, cheapening the yen, as the most convenient way out. Printing money will make matters worse in the long haul of course, but it will put off making any tough choices now.

No comments:

Post a Comment