Mish's Global Economic Trend Analysis |

- Ex-Goldman Sachs Managing Director is Leading Candidate to Replace Trichet as ECB President

- Is this more like 2007 or 1998?

- Gas Pump Prices Hit Highest Level Ever for Mid-February; Gas Price Seasonality, Where to from Here?

| Ex-Goldman Sachs Managing Director is Leading Candidate to Replace Trichet as ECB President Posted: 12 Feb 2011 01:54 PM PST ECB President Jean-Claude Trichet's term expires in October. Alex Weber president of Bundesbank (Germany's Central Bank), an inflation hawk was widely recognized to be the leading candidate to replace Trichet. However, that idea came to a crashing end last week when Alex Weber resigned from Bundesbank. Supposedly Trichet's replacement is a wide-open race. However, Mario Draghi, an Ex-Goldman Sachs Managing Director has the clear inside track. Please consider Axel Weber Resigns Bundesbank, Throws ECB Race Open Bundesbank President Axel Weber resigned, ending three days of confusion and opening the field for candidates from Finland to Italy to become the next chief of the European Central Bank.Philosophical Reasons For Weber Leaving Weber is not leaving for "personal personal" per se. He is leaving because of huge feuds with current President Jean-Claude Trichet, and the likelihood he would be in disagreement with the the rest of the ECB as well. For example, please consider ECB's Trichet Rejects Weber's Call to End Bond Purchase Program European Central Bank President Jean-Claude Trichet rejected Bundesbank President Axel Weber's call to end the bond purchase program that has provided a lifeline for European governments and banks trying to shore up their finances.Weber was never in favor of the ECB's bond program to begin with, and that caused a feud at the outset. Weber felt the ECB was not only violating the Maastricht Treaty, but making unsound decisions on monetary policy as well. Given Weber was in a distinct minority on many decisions he decided to say to hell with it. Mario Draghi is now recognized as the leading candidate to replace Jean-Claude Trichet. Mario Draghi's Background Inquiring minds are interested in Mario Dragh's Background Mario Draghi is a member of the Governing and General Councils of the European Central Bank and a member of the Board of Directors of the Bank for International Settlements. He is also governor for Italy on the Boards of Governors of the International Bank for Reconstruction and Development and the Asian Development Bank. In April 2006 he was elected Chairman of the Financial Stability Forum, which became Financial Stability Board in spring 2009.Mario Draghi's Role In Greek Debt Swaps Under Review Please consider Mario Draghi and Goldman Sachs, Again March 17, 2010SEC Names ex-Goldman Sachs Employee to Oversee Asset Managers and Hedged Funds While on the subject of ex-Goldman Sachs employees turning up in high-power jobs, please consider SEC Taps Goldman Sachs Executive as Division Head The Securities and Exchange Commission has named Goldman Sachs Asset Management Chief Investment Officer Eileen Rominger to head its division overseeing asset managers and hedge funds.All we need now to complete the picture is for an ex-Goldman employee to run for president of the United States and for another ex-Goldman employee to replace Bernanke at the Fed. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Is this more like 2007 or 1998? Posted: 12 Feb 2011 09:21 AM PST In Thursday's Breakfast with Dave, Dave Rosenberg asks the question Is this the time to be going long? My question is a bit different, but this is what Rosenberg had to say. Sorry, but that time has passed. But we will probably get another kick at the can because we are sure that the "event risk", which caused so much turbulence and buying opportunities in 2010 will come around again in 2011. But this is one overextended U.S. stock market, that is for sure.When Will Global Imbalances Matter? Everyone is partying, upping forecasts, jumping on the bandwagon, etc. Bernanke is openly bragging about his successes. Rosenberg asked and answered his question, but I have a slightly different one: Is this more like 2007 or more like 1998 with 2 more years of partying before another crash? No one knows for sure. Heck, most are not even aware of the question, oblivious to how overvalued this market is. If you are in the that group, please see Negative Annualized Stock Market Returns for the Next 10 Years or Longer? It's Far More Likely Than You Think. As in 2007, everyone thinks they can or will get out in time. Mathematically it's impossible. Moreover, dip buying is now so firmly entrenched (again), that few will recognize the turn when it happens. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

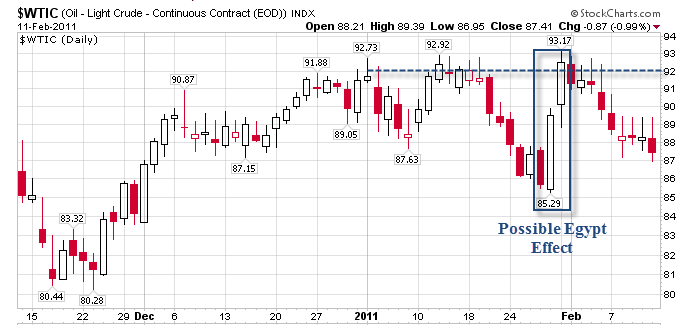

| Gas Pump Prices Hit Highest Level Ever for Mid-February; Gas Price Seasonality, Where to from Here? Posted: 12 Feb 2011 12:24 AM PST Yahoo!Finance reports Gas pump prices highest ever for this time of year U.S. gasoline prices have jumped to the highest levels ever for the middle of February. The national average hit $3.127 per gallon on Friday, about 50 cents above a year ago.Crude Futures - Monthly Chart  click on chart for sharper image Crude futures for now have stalled right at 50% retrace level of the 2008 plunge in spite of the recent turbulence in Egypt. Unleaded Gasoline Futures - Monthly Chart  click on chart for sharper image Unleaded gasoline futures and gas pump prices follow the price of crude as one might expect. Note the seasonal nature of the moves. Gasoline prices (and crude futures) tend to rise from January until June or July in most years. In 2007, there was a ramp from the beginning of the year that ended in April, followed by a pullback until July. From then it was straight up for a full year. 2009 was back to the familiar pattern of continued strength from the beginning of the year until July. 2010 had a July low instead of a high, similar to 2007. Crude Futures - Daily Chart  click on chart for sharper image Prices at the pump may be up, but crude prices are down since the start of the year as noted by the dashed line. Prices at the pump will head lower eventually if crude prices keep sliding. Inability for crude prices to continue higher with events in Egypt and the Mideast might be meaningful. Moreover, interest rate hikes in China could start weighing on commodity prices in general, especially if those hikes come at a pace faster than expected. There are a lot of variables in play, including seasonality, rate hikes in China, the extremely overbought reflation trade, Quantitative Easing, and price action weakness (except for a 2-day pop now taken back) in the face of events in Egypt. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment