Mish's Global Economic Trend Analysis |

| Challenge to Keynesians "Prove Rising Prices Provide an Overall Economic Benefit" Posted: 19 Oct 2014 08:33 PM PDT The ECB has been concerned about falling consumer prices. I propose that's 100% stupid, yet that's the concern. When the euro declined vs. the US dollar, the ECB was happy that inflation would inch back up. The fear now is that falling oil prices will take away the alleged gain of a falling euro. With that backdrop, credit the Financial Times for the absurd headline of the week: Eurozone Fails to Benefit from Weak Currency as Oil Price Slides. Pity the policy makers given the job of rescuing the eurozone from deflation.Pity the Keynesian Fools Financial Times writers Delphine Strauss and Claire Jones say "pity the policy makers." I say pity the fools who believe the thesis of their article. There is absolutely no benefit to rising consumer prices. Things are even worse if prices rise but wages don't. The very essence of rising standard of living is more goods at lower prices thanks to innovation and rising productivity. And there is no reason to believe wages will rise (or keep up with prices) if prices do rise. Challenge to Keynesians I challenge Strauss and Jones (or anyone else but especially Keynesians and Monetarists) to prove rising prices provide an overall economic benefit. Sure, those with first access to money benefit (the banks, the already wealthy, and government bodies via taxation). But that is at the expense of everyone else. The absurd underlying notion behind the battle cry for inflation is that if prices fall people will stop buying things and the economy will collapse. Reality Check Questions

Bonus Question If falling prices stop people from buying things, how are any computers, flat screen TVs, monitors, etc., ever sold, in light of the fact that quality improves and prices decline every year? Deflationary Spiral Nonsense I have discussed this many times before, most recently in Deflationary Spiral Nonsense; Keynesian Theory vs. Practice; Eurozone Policymakers Concerned About Falling Prices The idea that falling prices are bad for the economy is ridiculous. Taking out insurance against falling prices is even more absurd.Asset Deflation vs. Consumer Price Deflation What central bankers should fear is falling asset prices, more specifically, loans made on assets in an asset bubble. The irony is central banks create asset inflation by fighting something everyone on the planet should welcome. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

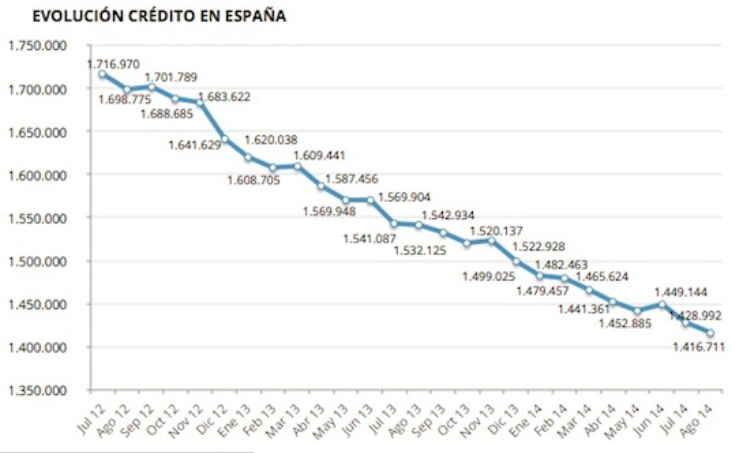

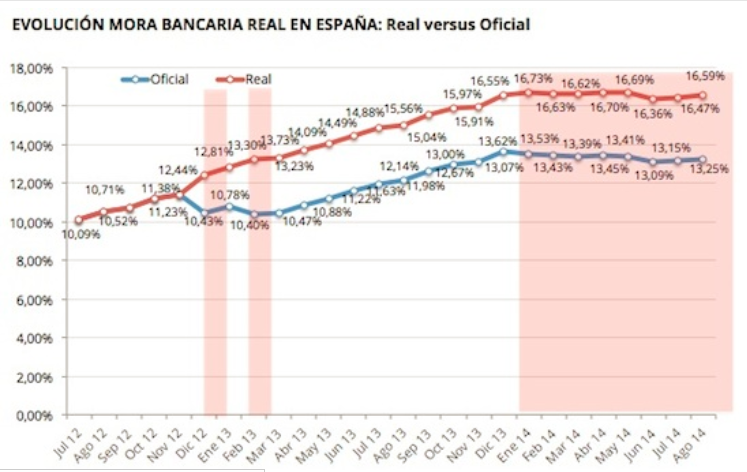

| Nonperforming Spanish Loans Near All-Time High as Overall Credit Shrinks Posted: 19 Oct 2014 09:25 AM PDT Huky Guru posted a couple of interesting charts on his blog today about shrinking credit but rising percentage of nonperforming Spanish bank loans: NPLs of banks rebounded to 16.59%. Seven points higher than in the 1994 crisis. Spanish Bank Shrinking Credit  Nonperforming Loans  The "real" numbers are normalized to account for a change in methodology. Today's number is just off the all-Time high of 16.73 percent in January of 2014. The "official" high was 13.62% in December of 2013. Both sets of numbers are "far above the crisis in 1994, when nonperforming loans peaked at 9.15%." The above charts provide further evidence the recovery in Spain is imaginary. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment