Mish's Global Economic Trend Analysis |

- BRICs Under Attack: S&P Cuts Brazil's Credit Rating to One Notch Above Speculative

- Will Prices Rise Significantly When Velocity of Money Picks Up?

- Stupidity is Logical and Understandable; So, How Stupid Will Things Get?

- Monetary Perspective on QE and Tapering

- China Output Contracts at Quickest Pace in 18 Months

| BRICs Under Attack: S&P Cuts Brazil's Credit Rating to One Notch Above Speculative Posted: 24 Mar 2014 10:24 PM PDT BRICs (Brazil, Russia, India, and China) cannot seem to get much love lately. Today, it's Brazil's turn to say "show me the love". Reuters reports S&P Cuts Brazil Credit Rating. Standard & Poor's cut Brazil's sovereign debt rating closer to speculative territory on Monday in a blow to President Dilma Rousseff, whose efforts to stir the economy from a years-long slump have eroded the country's finances.Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

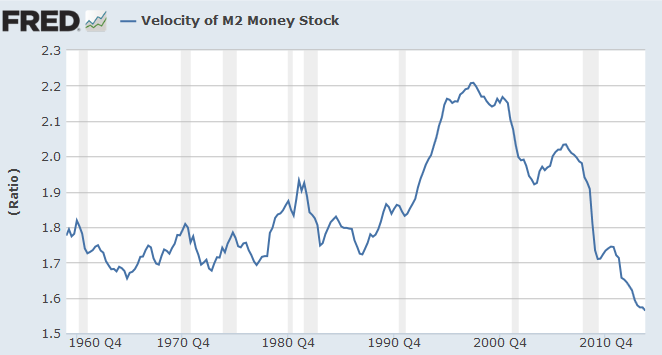

| Will Prices Rise Significantly When Velocity of Money Picks Up? Posted: 24 Mar 2014 12:18 PM PDT Several people have written recently telling me that price inflation is under control only because the velocity of money (the alleged rate at which money circulates) is falling. Reader Mark pinged me with this statement "Falling velocity is deflationary. It indicates people are saving their cash." Others have expressed similar opinions, typically in reference to this chart by the Fed. Velocity  Discussion of Ratios That chart looks ominous. Is it? First, please note the chart says velocity is a "ratio". A ratio of what? Velocity = Value of Transactions/Supply of Money. The value of transactions = Price * Transactions. In other words V = (P)(T/M) where where V stands for velocity, P stands for average prices, T stands for volume of transactions, and M stands for the money supply. Multiplying both sides by M yields the frequently cited equation: M(V) = P(T). Economists use real GDP as a measure of P(T). Thus M(V) = GDP. And of course V = GDP/M The ratio in the above chart is Real GDP/M2. Clearly velocity is falling. Velocity Theory The widely presented theory is "prices will rapidly rise if velocity increases." One problem with making such assumptions is in regards to measurement. What is Money? Is it M1, M2, M3 (discontinued), MZM, TMS1, or TMS2? Each one will give you a different measure of velocity. The Fed provides Three Measures of Velocity. And what about GDP? Recall that government spending, no matter how useless, adds to GDP. If the government paid people to spit at the moon it would add to GDP by definition. And as stupid as that sounds, it would have been less destructive than bombing Iraq to smithereens, making enemies in the process, and reducing the supply of oil at the same time. If GDP is debatable and money is debatable, and prices cannot be precisely measured in the first place, can velocity mean much? Three Important Statements Regarding Velocity

Is Velocity Like Magic? Also consider some similar observations made by Frank Shostak in the Mises Daily article Is Velocity Like Magic? Velocity Has Nothing To Do With the Purchasing Power of MoneyConclusion Most of the discussion to date regarding the velocity of money has been ridiculous.

Given GDP = P(T), you can repeat the above four statements substituting GDP for prices. Doing so, please note that rising prices with falling GDP would be the dreaded stagflation scenario, something Keynesian theory once suggested was "impossible". In short, it may very well be that prices rise with rising velocity, but they may also rise with falling velocity. Thus ... Velocity is an essentially meaningless result in an essentially meaningless equation. Rising or falling velocity will not cause anything to happen. Yet, the debate over the importance of velocity rages on. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Stupidity is Logical and Understandable; So, How Stupid Will Things Get? Posted: 24 Mar 2014 11:10 AM PDT As president Obama arrives in Europe to meet German chancellor Angela Merkel, Pressure mounts on Merkel Over Sanctions in Ukraine Crisis. When Angela Merkel, the German chancellor, meets Barack Obama, US president, at The Hague nuclear security summit on Monday, she will come under pressure to back economic sanctions against Russia.Stupidity is Never Difficult to Imagine Cordes finds sanctions "difficult to imagine" but Merkel's CDU party chief says further sanctions are "inevitable". Upping the ante, German EU energy commissioner, Oettinger, a ranking CDU politician wants increased sanctions without waiting for further aggression from Moscow. Oettinger says sanctions, which hit economic relations, involving exports, imports and investment are "logical and understandable" Since sanctions won't work and are a sure-fire Negative Sum Game, this is what Oettinger is really saying: "Stupidity is Logical and Understandable". Russia Imposes Sanctions on 13 Canadians, Including MPs While waiting for inevitable stupidity from Germany, the Globe and Mail reports Russia imposes sanctions on 13 Canadians, including MPs. The Russian government has banned entry to 13 Canadian senior civil servants and politicians in retaliation for punitive actions that Ottawa levied on Moscow elite over the annexation of Crimea and the destabilization of Ukraine.Stupidity Is ...

With all that going for stupidity, especially with major egos involved (see Buffoon Bluffery; What are Sanctions Really About?), no one can precisely answer the question "How stupid will things get?" Here's one thing we do know for sure: Failure is Truly Success! Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Monetary Perspective on QE and Tapering Posted: 24 Mar 2014 01:42 AM PDT In Reflections on the Yellen Taper-Hike Announcement; What Does the Fed Know? I quoted the opinion of Saxo Bank Chief economist Steen Jakobsen. Steen commented "Please, do not think for one minute that FOMC have any clue about the economy six months from and even less so looking into 2015." I am certainly in agreement with Steen, and gave my own look into what the Fed knew or didn't in Hilarious Transcripts of Fed Minutes from 2008 Reveal Completely Clueless Fed. Opinions aside, let's take a look at facts from a monetary point of view. My friend "BC" pinged me with the following chart. Monetary Base vs. Loans and Leases  click on any chart for sharper image Note that the adjusted monetary base is playing catchup to loans and leases of all commercial banks. When that happens, and I believe it will, taper or no taper, will base money be sufficient to cover all credit? Not quite. Taking a lead from "BC", here is a chart I put together. Credit Market Instruments Liability vs. Monetary Base  This is precisely what fractional reserve lending has wrought. Total credit liabilities approach $60 trillion. Those liabilities are backed up by about $4 trillion in base money supply. Some people might object the above chart reflects money substitutes and not money. Fair enough. So how much base money covers checking and savings accounts? Monetary Base vs. Checking Plus Savings Accounts  Some readers will recognize the above chart as True Money Supply "TMS2" vs. Base Money Supply. TMS2 consists of currency plus all the individual components of checking and savings deposits. In terms of how much base money covers savings and checking accounts, you can see about $6 trillion is missing. Loans and Leases are another matter as is Total Credit Liability. So when the Fed says it will "taper", let me ask some simple questions:

Bonus Question: What is this likely to mean for gold? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| China Output Contracts at Quickest Pace in 18 Months Posted: 23 Mar 2014 11:58 PM PDT The HSBC Flash China Manufacturing PMI shows Output Contracts at Quickest Pace in 18 Months. The overall PMI index, new orders, and production were all lower. In the face of an explosion of credit, still growing imbalances, malinvestments, property and other bubbles, it is a mystery why anyone expects China to make efforts to "stabilize growth". To stabilize growth implies more bad loans and more SOE malinvestment. Given China's massive housing vacancies, support for still more housing is ridiculous. More malinvestment is possible of course, but the longer China attempts to keep the credit party going, the worse the ultimate implosion. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment