Mish's Global Economic Trend Analysis |

- Baby Boomers Reluctant to Retire; What About the Fed's Retirement Thesis?

- Keynes Is Dead, Abenomics Fizzles, US Fails to Reach Escape Velocity, Stimulus Fatigue

- China Abandons Disastrous Cotton Stockpiling Program; Lessons Not Learned; What About Stockpiling Money?

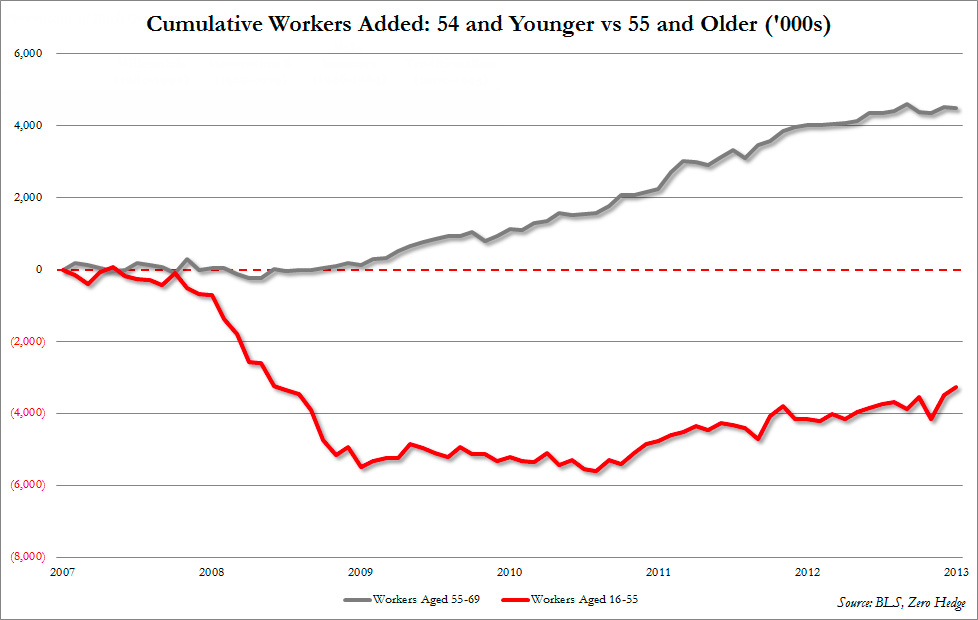

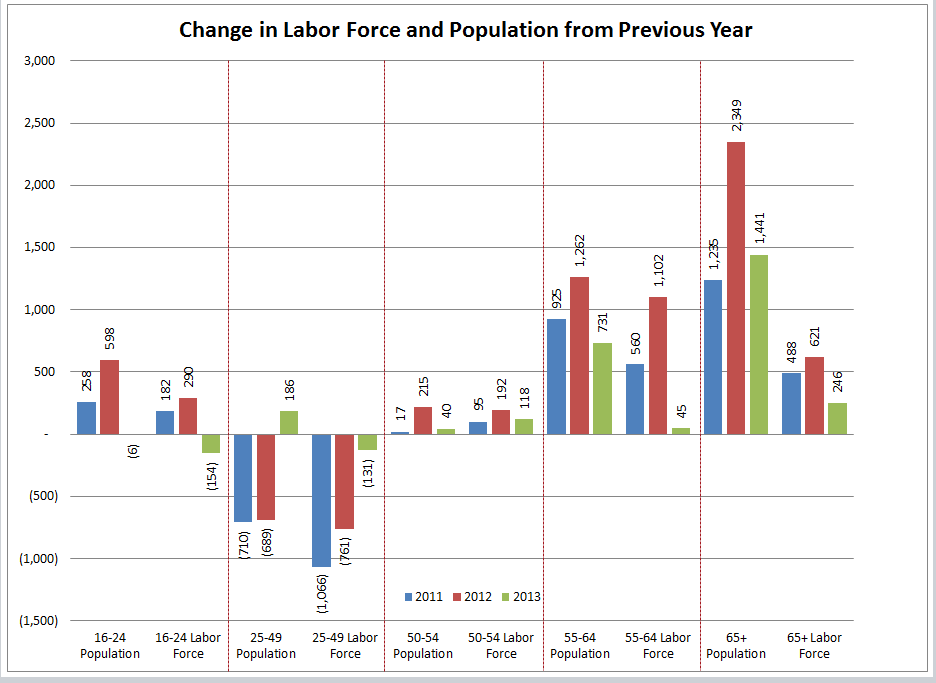

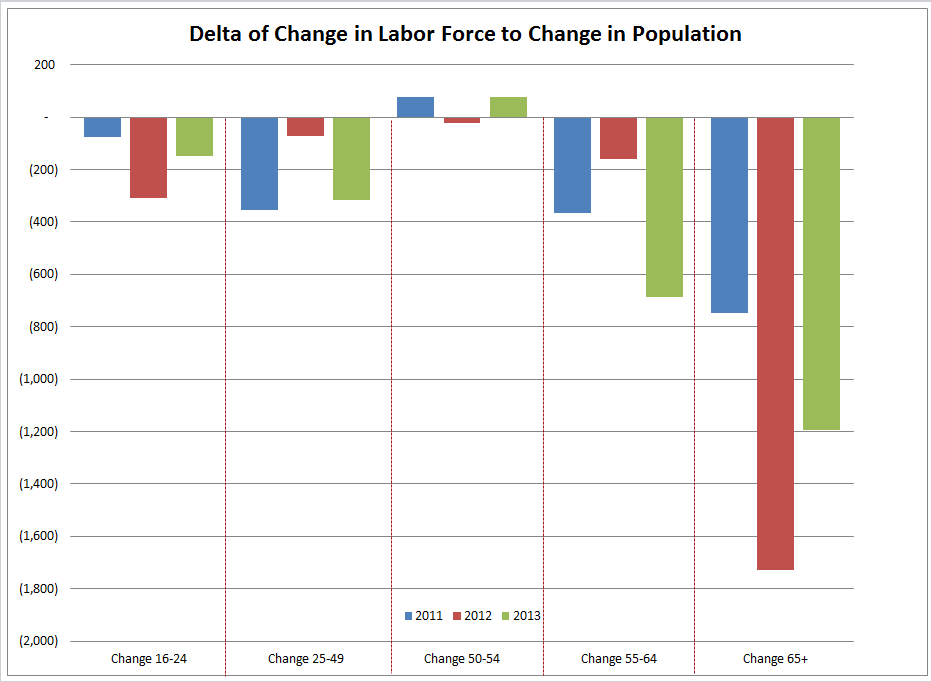

| Baby Boomers Reluctant to Retire; What About the Fed's Retirement Thesis? Posted: 21 Jan 2014 08:37 PM PST A new Gallup survey shows Many Baby Boomers Reluctant to Retire. True to their "live to work" reputation, some baby boomers are digging in their heels at the workplace as they approach the traditional retirement age of 65. While the average age at which U.S. retirees say they retired has risen steadily from 57 to 61 in the past two decades, boomers -- the youngest of whom will turn 50 this year -- will likely extend it even further. Nearly half (49%) of boomers still working say they don't expect to retire until they are 66 or older, including one in 10 who predict they will never retire.ZeroHedge Cries "BS" On Retirement Thesis In Spot The Labor Force Collapse Culprit, ZeroHedge produced a chart that allegedly debunks the thesis that the participation rate is declining because of retirement.  On the basis of that and similar charts ZeroHedge concludes So enough with all this "they are retiring" bull**it, and call it for what it is: millions of Americans of all ages, but mostly of prime working age, bailing out of the labor force by the millions because of equal or better opportunities elsewhere, opportunities which almost without exception are increasingly reliant on the ever more unsustainable and insolvent US welfare state. Off the Mark I have no desire to start "blog wars" but ZeroHedge is way off the mark. His chart neither proves nor disproves the retirement thesis. It only shows more people than ever before are working longer. To properly understand what is happening one must look at the raw numbers as well as the number of people moving from one demographic group to the next. I did just that on December 17, 2013 in Fed Study Shows Drop in Participation Rate Explained by Retirement; Let's Explore that Idea, in Depth and in Pictures. Yes people are working longer, but in relation to the number of people moving from one demographic group to the next, huge numbers of retirement-aged people have dropped out of the labor force en masse, as the following charts show. Change in Labor Force and Population From Previous Year  In the above chart, the change in labor force and the change in population in hard numbers (not percentage terms) are side-by-side. Consider the numbers for 2012 for age group 65+: The population rose by 2,349,000 but the labor force only rose by 621,000. What happened to the rest? Retirement? To make it even easier to see, please consider this final chart, with subtractions made. Delta of Change in Labor Force to Change in Population  The decline in labor force relative to the growth in population is heavily concentrated in the 65 and older demographic. As noted previously, the November Fed study on the Causes of Declines in the Labor Force Participation Rate by Shigeru Fujita at the Federal Reserve Bank of Philadelphia concludes "The decline in the participation rate in the last one-and-a-half years (when the unemployment rate declined faster than expected) is entirely due to retirement." The above charts prove that the analysis by the Fed is indeed reasonable. People are indeed working longer than ever, but the massive increase in the number of people moving into the 65 and older demographic allows for both a rising participation rate in that class as well as mass retirement. To be fair, we do not know why some retired. I strongly suspect many did so because their unemployment benefits ran out, and to get some money coming in from Social Security, they retired. I call this "forced retirement". Regardless, it's a huge mistake to fail to go through the proper math, as the above analysis shows. Finally, none of the above is proof the employment situation is reasonable. It's not. Over the past few years, huge numbers of people have dropped out of the labor force via disability fraud, by staying in school longer then they really want, and by forced retirement. I do agree with ZeroHedge in that the unemployment rate is realistically way higher than reported. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Keynes Is Dead, Abenomics Fizzles, US Fails to Reach Escape Velocity, Stimulus Fatigue Posted: 21 Jan 2014 12:46 PM PST Economist Andy Xie has an interesting article in CaixinOnline that contains his views on 2014. I agree with nearly all his viewpoints but one. Please consider Breaking Out Is Hard by Andie Xie. The global economy is unlikely to accelerate in 2014. The hope that the U.S. economy is reaching escape velocity won't pan out. Abenomics is likely to fizzle out in 2014. Emerging economies will likely remain in low gear. The chances are that the global economy, weighted by nominal GDP at current exchange rates, will grow at 2 percentLone Disagreement So what is it above that I disagree with? Nothing much. His global growth forecast is arguably too high, but that's about it. My major disagreement is with something in his article I did not quote above. Xie believes the "Nikkei is at a lofty level" and he is "surprised by how many investors are taken in by Abenomics." From my perspective, Xie has this backwards. Belief in Abenomics is not the issue. It surely isn't going to work. And when it doesn't work, what is prime minister Abe likely to do? I believe the answer is what all Keynesian fools do: embark on still more printing and competitive currency debasement, coupled with still more fiscal stimulus, in a further foolish attempt to make such policies work. If Abe manages to force up wages, stops QE, and lets the Yen rise, then I would be worried about the Nikkei. Instead, all indications are that Abe would double down, which in turn would further trash the Yen. That is why holding a yen-hedge on the Nikkei may be a smart thing to do. Like Xie, I think Abenomics is a failure. Unlike Xie, I think the Nikkei has risen because of the failure of Abenomics, not because of unfounded belief in the policy. Moreover, Japanese stocks are a relative value compared to most things, and arguably an outright value play as well, taking into consideration metrics like book value, debt levels, and PE ratios. Other than the debate on the Nikkei, I think Xie pretty much nailed the state of the global economy. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Posted: 21 Jan 2014 09:21 AM PST Inevitably, bad things happen when governments interfere in free markets. Here's an interesting example regarding cotton stockpiling. In 2011, China put a floor on the price of cotton and started a stockpiling program. In general terms, if a floor (on anything) is too high, the result is overproduction and forced stockpiling. If a ceiling is too low (hoping to stop price inflation), as is the case in Venezuela right now, merchandise disappears from the stores and a black market thrives. (See Venezuela's Hyperinflation Anatomy; Army Storms Caracas Electronics Stores; Total Economic Collapse Underway; Could This Happen in US?) With cotton, China set the support price too high, resulting in massive overproduction and huge stockpiles. As an interesting twist, there appeared to be shortages in spite of the huge stockpiles. How? Because the floor price was set too high, Chinese textile mills could get a better price by importing cotton. Ironically, all Chinese production went into stockpiles instead of textile mills, and the Chinese clothes mills had to import, driving up prices worldwide. As a result of non-free market intervention China is stuck with half the world's cotton supply and falling prices as well. The Financial Times discussed this situation in China abandons failed cotton stockpiling programme. However, the Times failed to mention the free market principles as to why the program was such a disaster. Lessons Not Learned Curiously, China still has a soybean reserve program in place. The Financial Times notes "A representative for the Heilongjiang Soybean Industry Association said his group hoped that some sort of improved stockpiling policy would remain in place." Of course producers want stockpiling programs. Stockpiling causes artificially high prices. What About Stockpiling Money? Central banks around the world have distorted the supply of a commodity far more important than cotton: money. And what applies to cotton and soybeans also applies to money and interest rates on money. The Fed created massive bubbles in the stock market in 2000 and 2007 via interference in the free market. The results were as every Austrian economist expected. The dotcom and housing bubbles blew sky high. In both instances, the Fed's response was more of the same policies that caused the bubbles. Supposedly the cure is the same policy that created the disease: more loose money! And like the previous two bubbles, the Fed cannot see this one either. Global Lessons Not Learned It's not just the Fed that's clueless. China soaks up every dollar it can, hoping to keep its export-driven economy churning along at artificially high growth rates. Chinese banks and State Owned Enterprises (SOEs), are in far worse financial shape than US banks. In Europe, adoption of the Euro is bound to fail. Actually the euro has already failed (it's just not widely recognized yet). As I look around, I see central bankers giving themselves a pat on the back for fixing the "great financial crisis". Yet nothing is fixed. Decades of blowing bubbles of increasing amplitude over time have taught them nothing. Timing is uncertain, but monetary and interest rate manipulations by central banks will end the same way China's cotton stockpiling ended: in disaster. A currency crisis awaits. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment