Mish's Global Economic Trend Analysis |

- Obamacare Support at Record Low 35%; Obamacare Named "Lie of the Year"; Bait and Switch; Obamacare Roundup; Meltdown Coming?

- Wall Street Is My Landlord; Blackstone's Home Rental Bonds Yet Another Sign of Renewed Credit Bubble

- China Interest Rate Crisis Continues: 7-Day Interest Rate Doubles to 10% in One Week; China Bans Words "Cash Crunch"

| Posted: 23 Dec 2013 07:14 PM PST It's been a while since I commented on Obamacare. Given news comes out every day, nearly all of it negative, I have shown restraint. Tonight, here's a recap of what you may have missed. Obamacare Support at Record Low 35% Today, December 23, a CNN poll finds Obamacare support at all-time low. Poll Details

I have gathered a huge number of Obamacare links in the past few weeks that I did not have time to comment on. Here are a few of them. This is by no means a complete list. Obamacare Roundup, Last Two Weeks

The final link above is interesting. The URL title is "obama-administration-secretly-extends-health-care-enrollment-deadline". I guess it's not much of a secret. Please note the political spectrum in the above links encompasses everything between the Huffington Post and Fox News. That's quite an accomplishment! Meltdown Coming? Let's finish up with a highlight from the Washington Post: Sen. Joe Manchin (D-W.Va.) says Obamacare could suffer 'complete meltdown' Sen. Joe Manchin (D-W.Va.) said Sunday that Obamacare could be headed for a "complete meltdown" if costs rise too fast and people are unhappy with their coverage.Even Democrats are distancing themselves from this disaster. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

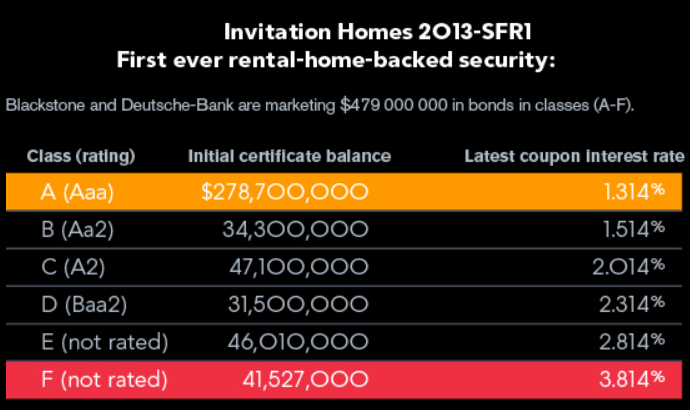

| Wall Street Is My Landlord; Blackstone's Home Rental Bonds Yet Another Sign of Renewed Credit Bubble Posted: 23 Dec 2013 10:11 AM PST Blackstone Group LP, the world's largest private equity firm, became the largest owner of rental homes in the U.S. , acquiring 41,000 homes in the past two years. In October, Blackstone offered the first-ever "rental-home-backed" security on Wall Street. The bond is backed by just a fraction — 3,207 — of the rental properties owned by Blackstone. Monthly rent checks from the properties will be used to service the $479.1 million security. See Bloomberg's Blackstone's Big Bet on Rental Homes for a giant infographic. Inquiring minds may also be interested in a related Bloomberg article, Wall Street Is My Landlord. Let's focus on the credit aspect of what's in the Blackstone/Deutsche "Invitation Homes", first-ever rent-based bond offering. Here is a snip from the gigantic infographic in the first link above. Invitation Homes Bond Offering  What do investors get for their money? A Bond Credit Rating Table courtesy of Wikipedia will help explain.

Whether or not one really believes the Aaa tranche truly deserves that rating, all those investors get is a coupon rate of 1.314%. Those buying the class "D" offering, rated Baa2, get a "lower medium grade" bond, two steps above junk (again assuming the class really deserves that rating). Those investors get a 2.314% return. Classes E and F, both "unrated" are highly likely to be pure garbage in my estimation. Blackstone Lures Investors to Home-Rental Bonds Feel warm and fuzzy with these bonds? If so please consider Blackstone Lures Investors to Home-Rental Bonds. Investors in Blackstone (BX) Group LP's debut sale of bonds backed by U.S. rental homes are agreeing to accept more risk than in traditional mortgage deals by at least two measures -- along with an unproven business.13-Point Deal Summary

What the biggest risk? Whalen says "The largest danger may be that Blackstone will be allowed to sell the Invitation Homes business or take it public before the securities mature". I disagree. I think the biggest deal-based risk is that individual properties can be sold over time, leaving increasing amounts of garbage in the loan portfolio. That thought alone makes me suspicious as to how Blackstone picked properties to go into this pool in the first place. Final Thoughts Without a doubt, Blackstone picked individual properties carefully, and every property placed in the pool was to maximize value for Blackstone, not investors. That is to be expected, but Blackstone went steps further, nearly to the point of detailing how investors are likely to be gored by this deal. Investors chasing this deal for paltry returns are picking up pennies in front of a steamroller. This is the way it is at the peak of every credit bubble. The only surprising thing is how quickly investors were willing to repeat their last mistake. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 23 Dec 2013 01:21 AM PST A "cash crunch" is on in China. But don't call it that, because China banned use of the term last week. The New York Times reports China Rates Approach Crisis Levels Despite Central Bank Measures. An exceptional bid by China's central bank to curb soaring interest rates and relieve pressure on the financial system appeared to have come up short on Monday, as Chinese money market rates shrugged off the measure and continued to approach the crisis levels seen in June.China Bans Words "Cash Crunch" Last Friday, the Financial Times reported China presses media to tone down cash crunch story. Chinese propaganda officials have ordered financial journalists and some media outlets to tone down their coverage of a liquidity crunch in the interbank market, in a sign of how worried Beijing is that the turmoil will continue when markets reopen on Monday. Don't worry. There isn't a cash crunch because China says so. Heck, China even banned the words. That should be proof enough. Besides, a quick check shows the Shanghai composite index is up a bit today at the time of this writing. Clearly, central bankers everywhere have everything perfectly under control. For now. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment