| More Obamashock! Glitches Hit Paper, Phone Applications; Obamacare Glitch Great Quotes Posted: 26 Oct 2013 06:44 PM PDT Millions of Existing Plans Dropped I posted my personal experiences on Obamacare, as well as those of a reader, in Tips on Navigating Obamacare Costs on HealthCare.Gov - My Personal Experience - Obamashock! Just in case anyone thought "ObamaShock!" was an isolated incident, the Weekly Standard reports Millions of Americans Are Losing Their Health Plans Because of Obamacare. While the Affordable Care Act was making its way through Congress in 2009 and 2010, President Obama famously promised the American people over and over again that if you like your health plan, you can keep it.

"Let me be exactly clear about what health care reform means to you," Obama said at one rally in July 2009. "First of all, if you've got health insurance, you like your doctors, you like your plan, you can keep your doctor, you can keep your plan. Nobody is talking about taking that away from you."

But the president's promise is turning out to be false for millions of Americans who have had their health insurance policies canceled because they don't meet the requirements of the Affordable Care Act.

According to health policy expert Bob Laszewski, roughly 16 million Americans will lose their current plans.

Because the Obama administration's regulations on grandfathering existing plans were so stringent as many as 16 million are not grandfathered and must comply with Obamacare at their next renewal.

Millions of people are now receiving letters from their carriers saying they are losing their current coverage and must re-enroll in order to avoid a break in coverage and comply with the new health law's benefit mandates––the vast majority by January 1. Most of these will be seeing some pretty big rate increases. Obamacare in Rural Areas The New York Times reports Health Care Law Fails to Lower Prices for Rural Areas As technical failures bedevil the rollout of President Obama's health care law, evidence is emerging that one of the program's loftiest goals — to encourage competition among insurers in an effort to keep costs low — is falling short for many rural Americans.

While competition is intense in many populous regions, rural areas and small towns have far fewer carriers offering plans in the law's online exchanges. Those places, many of them poor, are being asked to choose from some of the highest-priced plans in the 34 states where the federal government is running the health insurance marketplaces, a review by The New York Times has found.

Of the roughly 2,500 counties served by the federal exchanges, more than half, or 58 percent, have plans offered by just one or two insurance carriers, according to an analysis by The Times of county-level data provided by the Department of Health and Human Services. In about 530 counties, only a single insurer is participating.

"There's nothing in the structure of the Affordable Care Act which really deals with that problem," said John Holahan, a fellow at the Urban Institute, who noted that many factors determine costs in a given market. "I think that all else being equal, premiums will clearly be higher when there's not that competition."

The Obama administration has said 95 percent of Americans live in areas where there are at least two insurers in the exchanges. But many experts say two might not be enough to create competition that would help lower prices. Glitches Hit Paper, Phone Applications Politico reports " The online website signup procedure is such a disaster that President Barack Obama is urging Americans to go ahead and try to get health coverage by mailing in a paper application, calling the helpline or seeking help from one of the trained "assisters."" Please consider 'Glitches' hit Obamacare paper, phone applications too But the truth is those applications — on paper or by phone — have to get entered into the same lousy website that is causing the problems in the first place. And the people processing the paper and calls don't have any cyber secret passage to duck around that. They too have to deal with all the frustrations of HealthCare.gov — full-time.

"We're confident by the end of November, HealthCare.gov will be smooth for a vast majority of users," said Jeff Zients, the former White House aide and management expert brought into oversee the repair drive.

But for now, with HealthCare.gov crippled by design flaws and a morass of messy code, the president and health officials have been using a variety of posts and announcements to urge people to try low-tech ways of enrolling. Basically they are saying while the front door is stuck, try the side.

Of course, reading an 800 number on national TV — as the president did in the Rose Garden the other day — created a flood of callers who couldn't get through. That led to another wave of frustration and Obamacare punch lines. But Health and Human Services Secretary Kathleen Sebelius tweeted on Thursday that HHS bulked up the call center to include more than 10,000 trained representatives.

Even before the tech problems, the government had a private contractor, Serco, to handle paper applications, which were expected to come primarily from less Web-savvy people. On Thursday, the company's program director John Lau told the House Energy and Commerce Committee that it had completed between 3,000 and 4,000 applications.

But Serco will be flooded with paper applications if the website glitches persist, predicted John Gorman, founder of the Gorman Health Group, which has advised some of the insurance exchanges. "Serco is going to be swimming in paper within the next two to three weeks," he said. Obamacare Glitch Great Quotes Inquiring minds looking for the most telling and colorful comments made about Obamacare "glitches" can find them on Politico. Here's a particularly funny one.

"We're going to do a challenge. I'm going to try and download every movie ever made and you are going to try to sign up for Obamacare — and we'll see which happens first." — Jon Stewart to Secretary Kathleen Sebelius on "The Daily Show," Oct. 7 Nonetheless Obama insists the Obamacare show must go on. And what a horror story it is. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

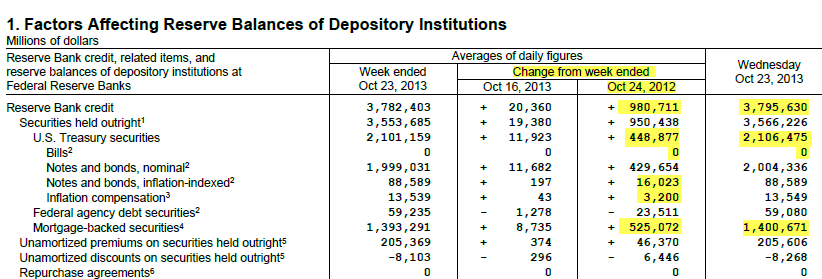

| New Tools! More Pure Bank Profit! Posted: 26 Oct 2013 10:52 AM PDT Inquiring minds are monitoring the Fed's Balance Sheet.  click on chart for sharper image click on chart for sharper image One more week like this and the FED balance sheet will be $1 trillion more than last year at this time. Currently now at $980 billion with this past week adding $20 billion. Breakdown From Year Ago - Total Credit: +980.711 Billion to $3.796 Trillion

- US Treasuries: +448.877 Billion to $2.106 Trillion

- Mortgage Backed Securities: +525.072 Billion to $1.401 Trillion

Of US treasuries, the Fed added (and holds) precisely $0 in short-term bills. Of US Treasuries, the Fed added 16 Billion in Inflation Indexed notes Obviously inflation is not a concern to the Fed. Bank profits are. Excess Reserves  The Fed is pumping money into the economy at at rate of $85 billion a month. Banks cannot use the money and are not lending it. The money piles up as excess reserves and the Fed (taxpayers) pays interest on excess reserves. Nonetheless, the Fed has a clever idea! It proposes a new tool to pay banks even more interest on money banks don't lend and cannot use (as an alternative to shrinking money supply). New Tools! With little fanfare or analysis by mainstream media as to what is really happening, Bloomberg reports Fed Gets Bigger in Markets as QE Prompts New Tools. The Federal Reserve is getting more involved in debt markets as it tries to compensate for the impact of its almost $4 trillion balance sheet on short-term interest rates.

Policy makers are testing a new tool intended to improve their control of near-term borrowing costs. The facility would allow banks, broker-dealers, money-market funds and some government-sponsored enterprises to lend the Fed unlimited amounts of cash overnight at a fixed rate in exchange for borrowing Treasuries in so-called reverse repo transactions.

The facility is the latest innovation from a central bank that has participated on an unprecedented scale in U.S. debt markets since the credit crisis began in 2007. It's designed to help policy makers -- buying $85 billion of bonds a month -- siphon off excess cash in the banking system when they begin to tighten policy. Three rounds of so-called quantitative easing have enlarged the Fed's balance sheet to almost $3.8 trillion.

The new tool -- called the fixed-rate, full-allotment overnight reverse repo facility -- also is aimed at helping Fed officials address distortions in the market caused by their securities purchases.

"It will serve to put whatever floor they want under rates," said Lou Crandall, chief economist at Wrightson ICAP LLC in Jersey City, New Jersey. "You're providing pretty broad-based access to Fed balances as an investment option."

While the Fed gained the ability in 2008 to pay interest on cash it holds in the form of excess bank reserves, that tool has limited effect in anchoring borrowing costs because only banks could park their funds at the central bank, Crandall said. By now offering to pay a fixed rate to a wider range of counterparties for their cash overnight, policy makers should be able to improve their control of near-term rates, he said.

"By offering a new, essentially risk-free investment, one would expect that anyone with access to such a facility would generally be unwilling to lend instead to someone else" at a lower rate, New York Fed President William C. Dudley said in a speech in New York Sept. 23. Where Does It End? From the Bloomberg article, one person sees things correctly. ... With "the amount of bonds that have been piling up on the Fed's System Open Market Account" there "has been a collateral shortage," said Jim Bianco, president of Bianco Research LLC in Chicago. "What worries me about the Fed is that in reacting to the fact that their actions have created an unintended consequence in a free market, instead of saying 'Oh, maybe we ought to re-think these actions,' their answer is 'No, we'll go manipulate that problem now.' Where does this end?" Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

No comments:

Post a Comment