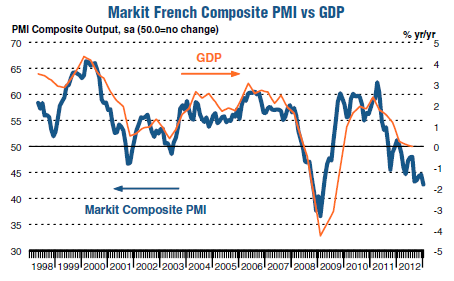

| Germany Rebounds but ... France Economic Implosion Accelerates; Record Decrease in Service Employment in Italy Posted: 06 Feb 2013 03:47 PM PST A quick look at economic data from Markit shows a recovery of sorts in Germany (it will not last) and a contraction in France at the steepest rate in four years. Meanwhile, Italy saw a PMI survey-record decrease in services employment in January. France - Sharpest Contraction in Four Years The Markit France Services PMI®, shows service sector business activity falls at sharpest rate since March 2009. Key points:

- Final Markit France Services Activity Index(1) at 43.6 (45.2 in December), 46-month low.

- Final Markit France Composite Output Index(2) at 42.7 (44.6 in December), 46-month low.

Historical overview:

Summary:

French service providers signalled a further reduction in business activity during January. Moreover, the rate of contraction accelerated to the fastest since March 2009. Incoming new business fell at a slower pace, but there were accelerated declines in both backlogs and employment. Input prices rose further, but output charges decreased at a sharper rate.

The seasonally adjusted final Markit France Services Business Activity Index slipped to 43.6 in January from 45.2 in December. The latest reading was indicative of a marked rate of contraction that was the sharpest for almost four years.

The amount of new work placed with French service providers was down for a tenth successive month in January. Outstanding business in the French service sector decreased at a faster rate in January. The latest fall was the sharpest since August 2009.

Faced with spare capacity, French service providers cut employment further in January. The pace of job shedding quickened to the sharpest for just over three years. Manufacturers also signalled a faster decline in staffing levels during the latest survey period. Consequently, overall employment in the French private sector fell at the sharpest pace in over three years.

Input costs faced by French service providers continued to rise in the latest survey period, with panellists commenting on higher prices for fuel, raw materials and salaries. Prices charged by French service providers fell further, with the latest drop the steepest since November 2009. Take another look at that chart of French GDP vs. the PMI. It should be easy to decipher where GDP is headed. Spain Employment Drops at Accelerated Pace The Markit Spain Services PMI® shows Slowest fall in activity for 19 months. Key points:

- Activity and new orders decline, but at slower rates

- Cost inflation moderates

- Further sharp fall in employment

Summary:

Although the Spanish service sector remained in contraction at the start of 2013, both activity and new business declined at slower rates during the month and confidence among firms with regards to the 12-month outlook improved. That said, employment continued to fall during January, and at an accelerated pace.

The headline seasonally adjusted Business Activity Index rose to 47.0 in January, from 44.3 in the previous month. The latest reading signalled a further solid reduction in activity during the month, although the rate of contraction was the weakest in the current 19-month sequence of decline.

New orders decreased at a solid pace in January, although the rate of decline eased to the slowest since August 2011. Backlogs of work decreased further in January as new orders fell. The rate of depletion in outstanding business remained marked, but slowed over the month to the weakest since August 2011.

In contrast to the trends in activity and new business, employment fell at a faster pace during the month. Moreover, the rate of job cuts was the sharpest for a year. Germany Rebounds The Markit Germany Services PMI® shows strongest rise in German service sector activity since June 2011. Key points:

- Final Germany Services Business Activity Index at 55.7 in January, up from 52.0 in December

- Final Germany Composite Output Index at 54.4 in January, up from 50.3 in December

Summary:

January data pointed to resurgent growth across the German service sector, with business activity and new order volumes both rising at the fastest rate since June 2011. Adjusted for seasonal influences, the final Markit Germany Services Business Activity Index picked up from 52.0 in December to 55.7 in January. The index highlighted back-to-back monthly rises in business activity for the first time since May 2012.

Higher levels of service sector output were underpinned by stronger intakes of new business in January. Latest data pointed to a robust and accelerated rise in new work, which contrasted with the declines recorded throughout the eight months prior to December. The overall improvement in new business was driven by a solid rise in the Transport & Storage sector.

Increased service sector staffing levels were recorded during January, which marked a third rise in employment in the past four months. That said, the rate of job creation was only marginal and slightly weaker than the long-run survey average. Italy - Record Decrease in Services Employment The Markit Markit/ADACI Italy Services PMI® shows Survey-record decrease in services employment in January. Key points:

- Rate of job losses sharpens amid faster drop in business activity

- Slower, albeit still marked, decrease in new work

- Future expectations highest in ten months

Summary:

Italy's services workforce shrank at a survey-record pace in January, as business activity also decreased at an accelerated rate. New work levels fell more slowly, however, with firms increasing in confidence about growth in output over the coming year.

Business activity compared to one month ago fell from December's post of 45.6 to 43.9 in the first survey period of the year. This latest reading was the lowest since last July, and signalled that the sector's ongoing sequence of contraction extended into a twentieth straight month.

Reflecting the sustained (and accelerated) decrease in business activity, Italian service providers continued to slash staff numbers during January. Moreover, the decline in employment over the month was the most marked since data collection commenced over 15 years ago.

Behind the weakness in the sector was a further drop in the level of incoming new business, which panel members suggested was in part due to a loss of clients since December. Although slower than in the final two months of 2012, the rate of decline in new work was nevertheless still sharp in the context of historical data.

Increased cost burdens were mostly absorbed by businesses in January, with charges falling on average for the eighteenth month in a row amid increased competitive pressures. Eurozone Divergence Hits Record High The Markit Eurozone Composite PMI® shows (as do the above reports) national divergence hits record high. Key Points:

Final Eurozone Composite Output Index: 48.6 (Flash 48.2, December 47.2)

Final Eurozone Services Business Activity Index: 48.6 (Flash 48.3, December 47.8)

Summary:

Although signalling a further deterioration in output of the Eurozone private sector economy, the rate of decline has now eased for three straight months. Both manufacturing production and service sector business activity declined at the slowest rates since last March, with similar modest rates of decline seen in each sector.

Inflows of new orders fell at the slowest pace since last February, dropping at reduced rates in both manufacturing and services. Goods producers continued to see the steeper rate of contraction.

A diverse picture was seen among the four largest euro members, with strong growth in Germany – output grew at the fastest rate for just over a year-and-a-half – contrasting with ongoing downturns in France, Italy and Spain. Output in France fell at the steepest rate of these four countries, registering the fastest monthly decline since March 2009 and causing the gap between the headline indices for France and Germany to increase to the widest in the survey history. The rate of decline also accelerated slightly in Italy, but eased to a 19-month low in Spain. I will have detailed comments on the divergences between Germany, France, and Italy in a followup post. Here's a hint: This is not a good thing for the eurozone. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Boehner Opposes Delay in Spending Cuts Without Reforms; House Passes Bill Requiring Balanced Budget Plan From Obama by April 1; Anyone Believe Either Will Happen? Posted: 06 Feb 2013 10:37 AM PST Government Executive reports House passes balanced budget bill. The House on Wednesday passed legislation that directs President Obama to submit a balanced budget plan to Congress this spring.

The Require a Plan Act (H.R. 444) compels Obama to submit a supplemental budget by April 1 if his fiscal 2014 budget blueprint does not include a plan to balance the government's books. That supplemental budget would outline a long-term deficit reduction strategy and timeline for balancing the budget. The chamber approved the legislation, shepherded by Rep. Tom Price, R-Ga., and the GOP leadership, after debating it Wednesday morning.

The Democratic-controlled Senate is unlikely to take up the bill. DBA (Dead Before Arrival) Given the senate will not take the measure up, the bill is nothing more than political grandstanding. Besides, there is not much merit to the idea anyway. Congress is in control of the budget, so it is up to Congress to present a plan to balance the budget (which, other than Senator Rand Paul, they will not do). No Delay in Automatic Spending Cuts? Here's one for the "I hope it's true, but I'll only believe it when I see it category" : Boehner Opposes Delay in Spending Cuts Without 'Reforms'. House Speaker John Boehner said he will oppose any delay of $1.2 trillion in automatic U.S. spending reductions set to begin March 1 unless Congress replaces them with other "cuts and reforms."

"At some point, Washington has to deal with its spending problem," Boehner, an Ohio Republican, told reporters at a Washington news conference today. "I've watched them kick this can down the road for 22 years that I've been here. I've had enough of it. It's time to act."

The March 1 deadline marks another fiscal showdown between the administration and Republicans, who control the House of Representatives. Boehner and other Republicans have said for weeks that they expect the spending reductions to take effect, and that they won't accept any tax increase to prevent them.

"Deep, indiscriminate cuts to things like education and training, energy and national security will cost us jobs and slow down our recovery," Obama said at the White House yesterday in urging adoption of a short-term plan. "This doesn't have to happen."

Democrats who control the Senate debated alternatives for replacing the spending cuts during their retreat yesterday in Annapolis. They agreed they should pursue a measure to replace the cuts with a combination of new tax revenue and a different set of spending reductions, said a Senate Democratic aide who spoke on condition of anonymity because the meeting was private. The lawmakers didn't decide on details or how long the spending cuts should be delayed, the aide said. Mish Point of View Congress is squabbling over $20 billion here and $12 billion there. The deficit is over a trillion dollars a year for as far as the eye can see. Reporters, Obama, and Democrats all talk as if there is "$1.2 trillion in automatic U.S. spending reductions" on the way. There isn't, and reporters ought to know better. In fact, there are no cuts at all that I can see. Rather, there is a reduction in projected increases, and even those reductions are back-end loaded. Even if the reductions represented true cuts, the cuts are spread out over 10 years, a pathetic $120 billion a year, when a total of a $1 trillion in cuts is needed to balance the budget. Furthermore, the above math assumes the economy will grow as fast as the Congressional budget office assumes (and I assure you it won't). The very best thing that could theoretically happen would be automatic "cuts" coupled with additional, meaningful "real" cuts. The odds of that combination are roughly zero percent. The best one could possibly hope for in practice is for the automatic cuts to kick in. Unfortunately, Spoiled Brat Syndrome is highly likely to get in the way. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

No comments:

Post a Comment