Mish's Global Economic Trend Analysis |

- Survey of European Banks Shows a Sharp Cutback in Lending; Three Reasons LTRO Will Not Get Banks to Lend

- Obama Releases Details on His Plan to Bail Out Banks, Fannie Mae, Hedge Funds, Wall Street, Fixing MERS and Screwing Taxpayers at Same Time; Key Aspects of Plan as Presented vs. Reality

- Rare Triumph of Freedom and Common Sense: Indiana Senate Sends Right-to-Work Bill for Governor Daniels’s Signature

- French Consumption Drops Most Since 1997, Increased VAT Supposed to Help

- Trim Tabs Fearless Forecast: US Payrolls +45,000 Jobs; Analysis of Jobs, Wages, GDP, Weekly Claims, Housing; Forced Lifestyle Changes; Boomer Drag on GDP Trends

| Posted: 01 Feb 2012 08:32 PM PST The LTRO may have ignited the bond markets and the stock market but it did not do anything for bank lending. The New York Times reports Survey of European Banks Shows a Sharp Cut in Lending Banks in the euro area cut lending sharply at the end of 2011, according to data published Wednesday, raising concern that Europe was on the verge of a credit crisis that could lead to a deeper recession than expected.Three Reasons LTRO Will Not Get Banks to Lend Contrary to popular belief the LTRO is not going to do much if anything to get banks to lend. Here are the reasons.

There is much ongoing debate about whether or not LTRO funding will be used to speculate in government bonds and if so how much. The bulk for the money so far as been to rollover debt, but the temptation to borrow from the ECB at 1% and buy 3-year Spanish bonds yielding 2.89%, 3-year Irish bonds yielding 5.43%, or 3-year Italian bonds at 3.8% is extremely high. Note that even 2-year bonds are in play. For example, 2-year Italian bonds yield 3.17%. Thus, the idea that none of the LTRO will go into government bonds is unlikely to hold up under scrutiny. Indeed banks are salivating to double or triple the €489bn they borrowed in December. For details please see You Ain't Seen Nothin' Yet; Another Trillion (or Two) Euro LTRO Coming Next Month The LTRO is good for bank profits, for now, but please remember that speculation in government bonds is what got European banks into trouble in the first place. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 01 Feb 2012 12:10 PM PST Today, under guise of helping "responsible homeowners" president Obama published details of Plan to Help Homeowners and Heal the Housing Market Key Aspects of the President's Plan as Presented

State of the Union Analysis I did an analysis of the proposal based on sketchy details, immediately following the president's State of the Union Address. Obama Proposes Mortgage Bailouts, Handouts, Copouts Exactly One Paragraph After Stating "Top to Bottom: No Bailouts, No Handouts, and No Copouts"; How the Taxpayer Ripoff Works. $10 Billion?! Really?One key point that I did not consider at the time came for reader David who said "A refinanced mortgage is a properly documented mortgage. So this also helps to clean up the mess of all the MERS, notes with broken signatures, improperly registered, etc." There is also a change in availability, one has to be current to take advantage. So taking those points into consideration.... Five Key Aspects of the President's Plan in Reality

Addendum: Reader Barry comments on "responsible" taxpayers. Hello MishMike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 01 Feb 2012 10:45 AM PST In a triumph of freedom and common sense over forced union slavery, the Indiana Senate Sends Right-to-Work Bill for Governor Daniels's Signature. Indiana will become the nation's 23rd right-to-work state after its Senate exempted nonunion employees from paying dues when working alongside their unionized colleagues.The bill does not go far enough. What's needed is the termination of all public union collective bargaining rights nationally. Cities and states are in trouble because politicians have been in bed with unions, driving up costs and taxpayers have to foot the bill. It's time to end union insanity, and more importantly union slavery. This bill is a step in the right direction. To understand why, please consider ...

Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| French Consumption Drops Most Since 1997, Increased VAT Supposed to Help Posted: 01 Feb 2012 09:54 AM PST Courtesy of Google Translate, please consider French Consumption Drops Most Since 1997 Last year, consumption of French manufactured goods, food and energy fell by 0.5% on average, the largest drop since 1997. Even during the 2008-2009 recession, the decline was not as marked. December was particularly bad (- 0.7%), raising fears of a difficult early 2012 against a backdrop of rising unemployment. Paradoxically, the government relies on the announcement of a social VAT to encourage the French to bring forward purchases before the increase in the rate in October.Increased VAT Supposed to Help!? Straight from the economically insane department, French president Nicolas Sarkozy wants to improve sales by increasing taxes. His belief is consumers will make major purchases before the rise in taxes. Lovely. What about the collapse in sales afterword? What about the need to hire then fire masses of workers because companies ramp up production now in expectation of increased sales now (that may or may not even happen), only to get rid of them later? The idea that borrowing sales from the future will accomplish anything good is preposterous. Generally politicians make such proposals in attempt to speed up the economy by carefully timing tax credits to help their election chances. In this case Sarkozy proposed the opposite way to bring forward sales. Bear in mind that Sarkozy's VAT increase would happen in October but French presidential elections are in April and May. Those elections are too soon for Sarkozy to benefit from his proposal. Taxpayers would likely put off purchases of major consumer goods as long as possible. Thus, an increase in sales (demand pulled forward) would likely be in July, August, and September, not February, March, and April. Challenger François Hollande jumped all over Sarkozy's increased VAT proposal. He has a more populist message, far more likely to resonate with voters: Hollande Vows to Tax the Rich, Take Pay Cut. Election politics aside, the French economy is slowing far more rapidly than most expected. Increased taxes whether on everyone or just the rich, certainly will not help. Such economically inane programs will intensify the strength and the length of the European recession. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

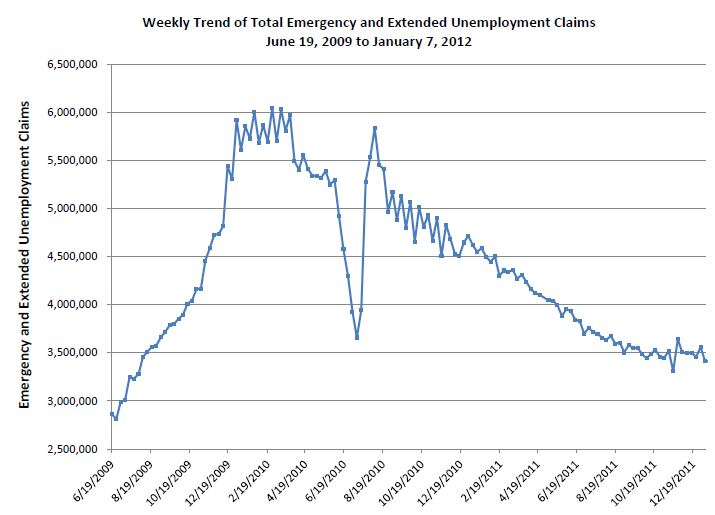

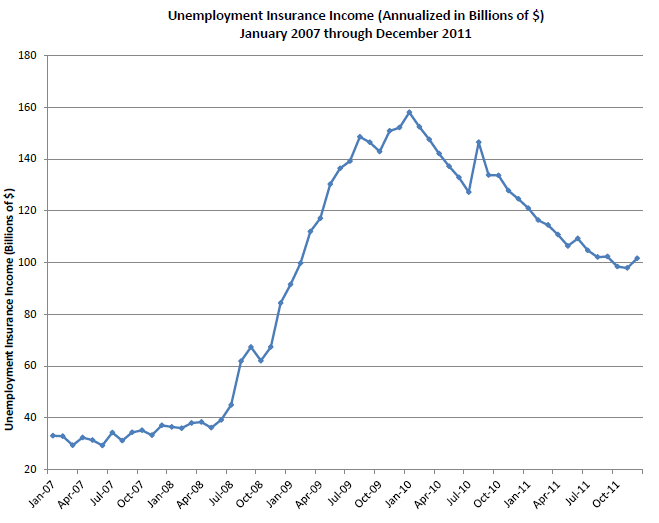

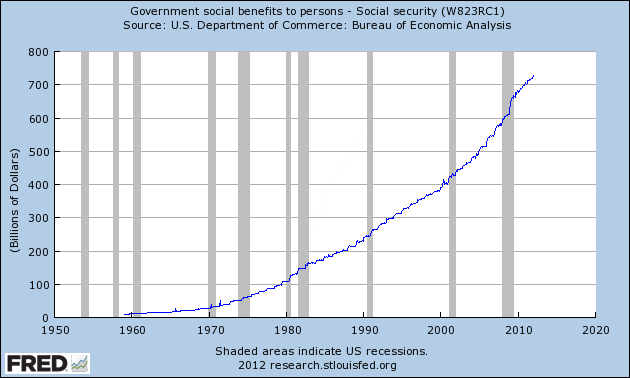

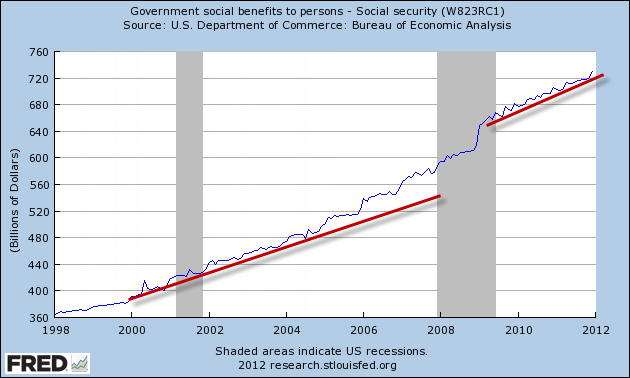

| Posted: 31 Jan 2012 11:20 PM PST Last month Trim Tabs estimated December payroll growth was 38,000. ADP estimated payroll growth at 325,000. I estimated +78,000. The BLS reported +200,000. For details, please see Nonfarm Payroll +200,000 ; Labor Force Drops Another 50,000 ; Those Not in Labor Force Rises by 194,000 ; Unemployment Rate 8.5% Was this a miss by Trim Tabs? ADP? Me? Here is the correct answer, whether or not you believe the BLS: I don't know and no one else does either. Seasonal Adjustments The BLS numbers are subject to massive revisions. Literally millions of jobs are revised away (or added) months, even years later. December and January are typically the hardest months to estimate, subject to huge seasonal adjustments and later revisions. Economic Turning Points Economic turning points compound the problem greatly. The BLS readily admits its birth-death adjustments are hugely wrong at turning points. Are we at an economic turning point now? I think so, and a turn in supporting data is all I need to convince me. If so, the BLS can be off on its numbers by a great deal. Trim Tabs Fearless Forecast The following weekly macro analysis and forecast (via email) is from Madeline Schnapp, Director, Macroeconomic Research, Trim Tabs. The above title is mine. Jobs: Based on our analysis of real-time income tax withholdings, we estimate that the U.S. economy added only 45,000 jobs in January, little changed from 38,000 in December.Unemployment Insurance and Weekly Claims Here are two of the many charts from the report. Weekly Trend of Claims  click on chart for sharper image Trim Tabs writes ... "At its peak in February 2010, the federal government's emergency and extended unemployment benefits programs provided assistance to 6.0 million people. Since then, the number of people receiving benefits has steadily declined, and they totaled only 3.4 million as of the week ended January 6. Since only 2.2 million jobs have been created since the recession started in December 2007—fewer than the number of people no longer receiving benefits—it is likely that 1.0 million or more people now lack both benefits and jobs." Emphasis added. Involuntary Retirement I think it is much worse than that. Technically it could be as high as 3.5 million (assuming no one with expiring benefits ever found a job). It would only be a million or so, if all of them did. Neither of those extremes is likely so I will make a rough guess that 2 million lost benefits and still have no job. However, many of those with expiring benefits likely took what I call "forced retirement". They wanted a job, needed a job, yet had no job and no prospects of a job. To survive, those of sufficient age retired involuntarily to collect social security benefits. Weekly Trend of Benefits  Trim Tabs writes "According to the BEA, the loss of income from extended and emergency unemployment insurance benefits has amounted to $57 billion since January 2010. In the past twelve months, the loss of income amounted to $23 billion, which is equal to about 13.4% of the estimated $188 billion increase in wages and salaries in 2011. In 2012, we estimate that expiring benefits will reduce incomes by approximately $25 to $50 billion.". It's safe to assume the loss of income is substantial, and it's about to get "more substantial". However, one does need to factor in involuntary retirement and subsequent social security payments. Social Security Benefits  Social Security Benefits Detail  That's quite a jump. Boomer demographics is clearly at play. But how much is "involuntary retirement"? Regardless, one thing is certain: That exponential trend is not remotely sustainable. Forced Lifestyle Changes One final point about social security: Retirement income does not match employment income. The presumption is "it doesn't have to". Just how valid is that presumption? Even if it is valid, how many have sufficient savings to retire with the same lifestyle? For someone with a mortgage and underwater on their house with rising food and energy costs, the presumption is not likely to be correct and/or savings are not likely to be sufficient. The obvious result is a "forced lifestyle change" and less spending. This boomer drag on GDP trends is enormous, yet few see it. Moreover, interests rates of 0% on CDs does not help any. Those on fixed income have been clobbered by Fed policies. I have talked about this numerous times but here is a quick recap of a pair of recent articles.

Recession Rationale Stacked Up Recent earnings reports have contained numerous misses, economic data has been generally weak in the US and very weak in Europe, and the Fed did not pledge to hold interest rates to zero through the end of 2014 for no reason. Recession rationale is stacked up, we just need coincident indicators to confirm. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment