| Moody's Warns Against Collateral Proposal; In Response, Finnish PM Warns Finland will Not Sign Second Greek Bailout Without Collateral; Merkel Madness Posted: 23 Aug 2011 03:45 PM PDT The battle over Greek collateral for additional loans to Greece has heated up on multiple fronts in five countries. Let's start with a look at a warning from Moody's. FX Street notes Moody's warns that Greek bailout might be delayedMoody's rating agency warned on Monday that EU countries which demand collateral agreements with Greece might delay the payment of the next 8 billion euro tranche of the rescue fund for Athens, push it into default and hamper the fight against the crisis in the Eurozone.

Last week Finland negotiated a bilateral deal with Greece; soon Austria, the Netherlands and Slovakia demanded similar guarantees. Greek Finance Minister Evangelos Venizelos asked the European Commission, the ECB and the IMF for help with solving possible further disputes with countries demanding collateral agreements.

Moody's considers the Greek-Finnish agreement a sign that some Eurozone countries and politicians are not capable of implementing measures necessary to maintain stability in the region. It adds additional pressure on France and Germany to take an even stronger position and present a clearer plan than the one agreed on last week. Germany has already expressed its objection towards the pact with Finland, pointing out that such agreements should be consulted with and approved by all of the Eurozone members.

Angela Merkel and Nicolas Sarkozy held a meeting last week and announced a battery of new measures to have a new, powerful and "true European economic government". Both leaders rejected the idea of euro bonds, which disappointed investors. They proposed to establish a common economic government for EU for 2½ years that would help strengthen national fiscal solvency and asked that the 17 euro zone countries must have a public debt ceiling rule in their constitutions. They suggested a tax on financial transactions in September and more powers to the European Commission. Merkel Madness Pray tell what "new, powerful and true European economic government" is on the horizon without common fiscal policy of common bonds? Is this Merkel Madness or is she playing the Jean-Claude Juncker card "You have to lie when it gets serious"? Regardless, it is Finland who has the cards given the stance of Finnish Prime Minister Finnish Prime Minister Jyrki Katainen. Finland will Not Sign Second Greek Bailout Without Collateral The Euro Observer reports Finland puts Greek bailout package under pressure The US-based ratings agency in a note on Monday (22 August) predicted other eurozone countries will reject a deal between Finland and Greece for Athens to put around €600 million in an escrow account in case it is unable to pay back Helsinki's part of its second bailout.

"A proliferation of collateral agreements would ... imply that the some euro-area countries would bear disproportionately large shares of the risk associated with the provision of financial support ," it said. "We expect other euro-area members to ultimately reject the Finland-Greece deal ... but the message sent by the calls for such agreements confirms that Europe is conflicted over the very decision to provide financial support to its members, not just the amount of support."

Finnish Prime Minister Jyrki Katainen has warned that if the collateral deal is thrown out, Finland will not sign up to the second Greek bailout.

Katainen's position, which has already seen Austria, the Netherlands and Slovakia explore possibilities for their own collateral arrangements with Greece, attracted criticism from Dutch finance minister Jan Kees de Jager on Monday.

"The Netherlands is no supporter of this proposal ... It is not compatible with the principle of equal treatment of all euro countries," de Jager said in an open letter to the Dutch parliament.

The potential proliferation of collateral requests is not the only emerging risk to the EU's self-imposed deadline to get the new bailout arrangements ratified by all 17 eurozone countries by the end of September.

The German central bank in its latest monthly report indicated that the eurozone deal, which also involves provisions for the EU bailout fund, the EFSF, to buy bonds from struggling euro economies, might breach German law by marking a new surrender of sovereign fiscal powers to Brussels.

"Far-reaching extra risks will be shifted to those countries providing help and to their taxpayers, and entail a large step towards a pooling of risks from particular EMU [European Monetary Union] states with unsound public finances," the Bundesbank said.

"Unless there is a fundamental change of regime involving a far-reaching surrender of national fiscal sovereignty, it is imperative that the 'no bail-out' rule – still enshrined in the treaties - should be strengthened by market discipline, rather than fatally weakened."

The bank's statement lends weight to a legal challenge to the bailout deal filed in Germany's constitutional court ahead of the judge's verdict, due in the coming weeks.

So not only might Finland, Austria, Slovakia, and the Netherlands tell the EU, the ECB, and the IMF to "go to hell", a correct constitutional ruling in Germany might end the discussion once and for all. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| 2-Year Treasuries at Record Low .21% Yield; LIBOR Exceeds 2-Year Yield; Is this Crazy? Posted: 23 Aug 2011 11:58 AM PDT Nearly the entire treasury yield curve is at or near record low yields as Bloomberg notes in Treasury Auctions Two-Year Notes at a Record Low Yield on Refuge DemandThe Treasury sold $35 billion of two-year notes at a record low yield of 0.22 percent as investors continue to seek the world's safest securities as a refuge from financial market turmoil and a slowing economy.

Record Lows

The 10-year note yields dropped on Aug. 18 to the historical low of 1.97 percent. Yields on five- and seven-year notes fell that day to records of 0.79 percent and 1.31 percent.

Two-year note yields reached a record low of 0.1568 percent on Aug. 9.

The two-year note auction yield was less than the previous record low of 0.395 percent on June 27 and compared with the average forecast of 0.221 percent in a Bloomberg News survey of eight of the Fed's primary dealers.

Bid Pattern

Indirect bidders, an investor class that includes foreign central banks, purchased 31.6 percent of the notes, compared with 27.7 percent at the July 26 offering and an average of 31.1 percent for the past 10 auctions.

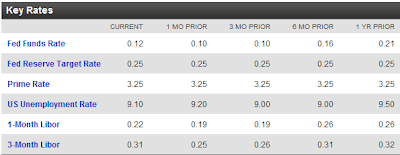

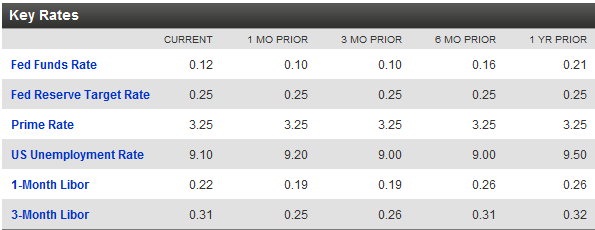

Direct bidders, non-primary dealer investors that place their bids directly with the Treasury, bought 15.9 percent of the notes, versus 20 percent last month and an average of 15.1 percent at the last 10 auctions. So much for the potty notion that foreign governments were about to dump US treasuries. Not to fear, I am sure that silly notion will be revived next week if not tomorrow. Treasuries Invert With LIBOR If you were waiting for the yield curve to invert before you were willing to admit the likelihood of recession, you have in inversion of sorts, not with treasury yields bur rater treasury yields to LIBOR (the rate at which banks lend to each other). Overnight, 3-month, 6-month, and 1-year LIBOR rates exceed yield on 2-year treasuries.  The above from Bloomberg Key Rates. Current LIBOR is .31% and that is a higher yield that treasuries all the way through 2-year, and nearly matches 3-year treasuries at .36%. Flashback March 10, 2011: Pimco Dumps All Remaining Treasuries in Total Return Fund; Six Reasons to Fade Bill Gross Pimco's Bill Gross has been dumping US government debt in favor of other alternatives including emerging-market opportunities. Looking ahead, I think it's more likely to be a bullish setup for treasuries than not.

First, please consider the news.

Bloomberg reports Pimco's Gross Eliminates Government Debt From Total Return Fund

Six Reasons to Fade Pimco

I view this setup as favorable for US Government bonds. For starters there is no Pimco selling pressure, only potential buying pressure when Gross changes his mind.

Second, everyone seems to think the end of QE II will be the death of treasuries. While that could be the case, sentiment is so one-sided that I rather doubt it, especially is the global recovery stalls.

Third, the US dollar is towards the bottom of a broad range and any bounce could easily wipe out gains in higher yielding emerging-market debt.

Fourth, the global macro picture is weakening considerably with overheating in China, state government austerity measures in the US, and a renewed sovereign debt crisis in Europe on top of a supply shock in oil. Emerging markets are unlikely the place to be in such a setup.

Fifth, chasing yield means chasing risk, and that is on top of currency risk. Chasing risk is highly likely to fail again at some point, the only question is when.

Sixth, several interest rate hikes are priced in by the ECB this year. Will all those hikes come? I rather doubt it, and if the ECB doesn't hike, look for the US dollar to rally, perhaps significantly. Nearly everyone but economist Dave Rosenberg dismissed US recession talk in March, few do so now and investors are no longer looking for gains, but rather simply a safe place to not lose money. The US dollar did not rally yet as I had expected but the rest of what I said was spot on. Bear in mind I see no value in US treasuries now, and there was little value even then. So are 2-year yields at .21% crazy? Hardly. It's the search for safe, liquid hiding places that has compressed US yields. Risk in equities heading into a recession, with Europe already in recession and Asia slowing rapidly, is enormous. Moreover, that 1 month LIBOR is .31% while 1-month Treasuries sit at 0% is not crazy either, except perhaps in reverse (the spread is not high enough). Distrust between banks is high and rising and for good reason. Even on this nearly 3% up day in the markets, Bank of America is trading down nearly 3% and at one point touched as low as $6.01, down about 6.5%. The risk trade is off and it may be off for longer than most think. For reasons, please see Another "Lost Decade" Coming Up; Boomer Retirement Headwinds; P/E Expansion and Contraction Demographic Model; Negative Returns for a Decade Revisited Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Another "Lost Decade" Coming Up; Boomer Retirement Headwinds; P/E Expansion and Contraction Demographic Model; Negative Returns for a Decade Revisited Posted: 23 Aug 2011 03:03 AM PDT Inquiring minds are digging into a Federal Reserve Bank of San Francisco report that models equity prices and P/E ratios based on demographics. The outlook is not promising to say the least. Interestingly, the report matches articles I wrote earlier this year based on cycles, not demographics. First let's take a look at the Fed report, then another look at my previous articles on P/E expansion and contraction followed by a new chart that suggests another "lost decade" is in progress right now. Please consider Boomer Retirement: Headwinds for U.S. Equity Markets?Historical data indicate a strong relationship between the age distribution of the U.S. population and stock market performance. A key demographic trend is the aging of the baby boom generation. As they reach retirement age, they are likely to shift from buying stocks to selling their equity holdings to finance retirement. Statistical models suggest that this shift could be a factor holding down equity valuations over the next two decades.

Demographic trends and stock prices: Some evidence

To examine the historical relationship between demographic trends and stock prices, we consider a statistical model in which the equity price/earnings (P/E) ratio depends on a measure of age distribution.

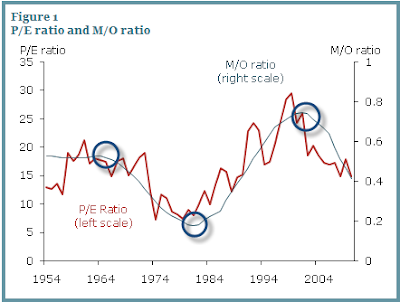

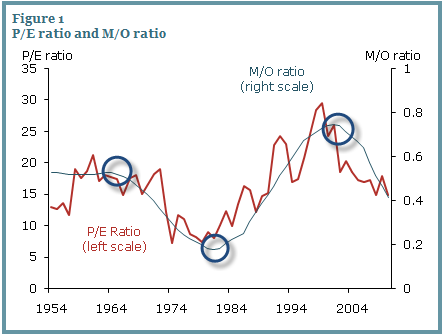

We construct the P/E ratio based on the year-end level of the Standard & Poor's 500 Index adjusted for inflation and average inflation-adjusted earnings over the past 12 months. We measure age distribution using the ratio of the middle-age cohort, age 40–49, to the old-age cohort, age 60–69. We call this the M/O ratio.

Figure 1 displays the P/E and M/O ratios from 1954 to 2010. The two series appear to be highly correlated. [Circles added by Mish for later reference]

Between 1981 and 2000, as baby boomers reached their peak working and saving ages, the M/O ratio increased from about 0.18 to about 0.74. During the same period, the P/E ratio tripled from about 8 to 24. In the 2000s, as the baby boom generation started aging and the baby bust generation started to reach prime working and saving ages, the M/O and P/E ratios both declined substantially. Statistical analysis confirms this correlation. In our model, we obtain a statistically and economically significant estimate of the relationship between the P/E and M/O ratios. We estimate that the M/O ratio explains about 61% of the movements in the P/E ratio during the sample period. In other words, the M/O ratio predicts long-run trends in the P/E ratio well.

Demographic headwinds for U.S. stock prices

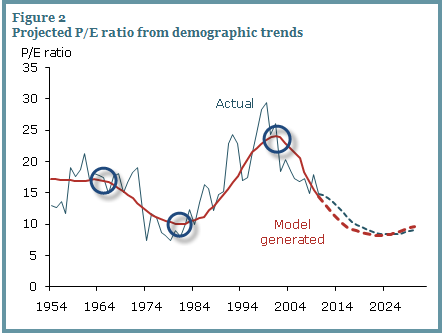

This evidence suggests that U.S. equity values are closely related to the age distribution of the population. Since demographic trends are largely predictable, we can forecast the path that the P/E ratio is likely to follow in the next few decades based on the predicted M/O ratio. Figure 2 compares the actual and model-implied P/E ratios for the sample period ending in 2010. We calculate the path for the model-implied P/E during the sample period by feeding in actual M/O ratios. We call the long-run path of the P/E ratio predicted by the model the "potential P/E ratio" and designate it P/E*. Figure 2 shows that the P/E* (red dashed line) is highly correlated with actual P/E during the sample period.

To generate a forecast for actual P/E from 2011 to 2030, we must first project P/E* for that period. To obtain this future P/E* path, we calculate the projected M/O ratio from 2011 to 2030 by feeding Census Bureau projected population data into the estimated model. Figure 2 shows that P/E* should decline persistently from about 15 in 2010 to about 8.4 in 2025, before recovering to 9.14 in 2030.

We are also interested in forecasting the potential path for stock prices. Since we have forecast a path for the P/E ratio, predicting stock prices is straightforward if we can project earnings, the E part of the ratio. For this purpose, we assume that, in the next decade, real earnings will grow steadily at the same average 3.42% annual rate by which they grew from 1954 to 2010. To obtain real earnings, we deflate nominal earnings by the consumer price index.

The model-generated path for real stock prices implied by demographic trends is quite bearish. Real stock prices follow a downward trend until 2021, cumulatively declining about 13% relative to 2010. The subsequent recovery is quite slow. Indeed, real stock prices are not expected to return to their 2010 level until 2027. On the brighter side, as the M/O ratio rebounds in 2025, we should expect a strong stock price recovery. By 2030, our calculations suggest that the real value of equities will be about 20% higher than in 2010. P/E Expansion and Contraction Drive Share Prices Not Earnings Figure 2 above ought to scare the daylights out of long-term buy-and-hold types because it is expansion and contraction of P/Es that most determines share prices, not earnings. I covered that idea in depth in Negative Annualized Stock Market Returns for the Next 10 Years or Longer? It's Far More Likely Than You Think. I used Crestmont's matrix S&P 500 Nominal Returns + Dividends as the starting point for the following tables and analysis.

The table below shows a sampling of years (some high valuation years and some low) along with annualized returns for two decades.

Annualized Rates of Return for Select Years

Click on any table to see a sharper image

Note how much the starting PE valuation matters. Someone who started investing in 1929 received an annualized rate-of-return of 0% for two full decades, even if they religiously reinvested dividends every year.

However, someone investing in 1982 received an excellent annualized rate-of-return for two full decades (12% for the first decade and 9% annualized for 20 years).

Note year 2000. Starting valuations were the highest in history. It should not have been a surprise to discover that 10 years later, the annualized rate-of-return was -2%.

Bear in mind, the Case-Shiller normalized PE for the year ending 2010 is 23. Does that bode well for the next decade?

Of course no one knows what this year or next year will bring.

Take a look at 1996 in the above table. In spite of several years of huge stock market gains, the annualized rate-of-return to date sits at 3.

Cycles of PE Compression and Expansion

Over long periods of time PE ratios tend to compress and expand. Unless "it's different this time", history says that we are in a secular downtrend in PEs. From 1983 until 2000, investors had the tailwinds PE expansion at their back. Since 2000, PEs fluctuated but the stock market never returned to valuations that typically mark a bear market bottom.

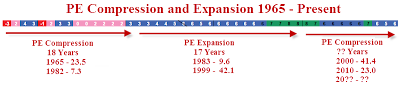

Moreover, demographically speaking, the current decade not only starts with very rich valuations, but also comes at a time when peak earnings of boomers have passed. Those boomers are now heading into retirement and will need to draw down savings, not accumulate large houses and more toys. There is much more in the above article including a look at fundamental reasons why valuations are currently stretched far beyond what analysts tell you. Please take a look if you have not done so already. PE Compression and Expansion 1965 - Present Also take a good look at that P/E Compression Expansion Chart 1965 to Present and compare to the charts by the San Francisco Fed. The P/E ratios will not exactly match because I use normalized earnings but the time periods match and the overall trends match as well. Starting in 1965 there was P/E compression for 18 years. Staring in 1983 there was P/E expansion for 17 years. That marked capped the biggest bull market in history. Now What? My model suggests 17-18 years of P/E compression. The Fed article suggests even longer! If so, where are stock prices headed?  Bear in mind, I do not subscribe to the San Francisco Fed idea " real earnings will grow steadily at the same average 3.42% annual rate by which they grew from 1954 to 2010". We are in the midst of a massive debt-deflation cycle similar to the one that has plagued Japan for over two decades. There is no reason to expect earnings growth to match prior averages. Value Traps Not only will we be in a lengthy period of P/E compression, debt-deflation and related issues suggest earnings will compress as well. This compounds greatly the "Value Trap" problem I have mentioned several times recently, notably Value Traps Galore (Including Financials and Berkshire); Dead Money for a Decade. Here is the conclusion of " Negative Annualized Stock Market Returns for the Next 10 Years or Longer? It's Far More Likely Than You Think" Where to From Here?

Hopefully you now realize that expectations of rising earnings being tremendous for the stock market is a fallacious construct. Such talk ignores high valuations, the long-term trend in valuations, and demographics. Moreover, it's debatable if earnings are likely to rise in the first place.

With that in mind, people chasing this market as well as those fully invested do not realize how lucky they have been.

Last week I received an email from someone who fears being out the market. I heard the same thing in 2007. I suggest people ought to fear being fully invested with no hedges. The same applies to pension funds. Note that most pension plan assumptions are on the order of 8% annualized rates-of return, and pension funds are typically 100% invested, 100% of the time.

However, I do not know where the market is headed this year, nor does anyone else. 2011 may turn out like 1998 or it may turn out like 2008.

Either way, history strongly suggests that 10-year and 20-year returns looking ahead are likely to be low, if not negative.

Investing, like life, is a marathon not a sprint. Sometimes the prudent thing to do is sit on the sidelines waiting for better opportunities, even if it means enduring cat-calls and taunts from those who do not have any understanding of risk or history. That was written in February 2011. At the time, and for the next couple months I received many emails from people who feared being out of the market. Given valuations, demographics, and trends in P/E compression, the fear should be about being in this market unhedged, not being out of it. As noted by me previously, and now by the San Francisco Fed, this sorry state of affairs could last for years. Alternatively, stocks might crash once again to get to more reasonable valuations. Either way, the picture is not pretty for those following buy-hold-and-forget-about-it strategies. Someone retiring now does not have until 2027 (the Fed's prediction), to get back to even. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

No comments:

Post a Comment