| Libyan Rebels, Gulf Cooperation Council Seek No-Fly Zone; President Obama, NATO Discuss the Possibility; How Do You Make a No-Fly Zone? Posted: 07 Mar 2011 06:02 PM PST In order for the United Nations to act on a no-fly zone, all 5 permanent members of the UN Security council would have to agree. Those members are China, France, the Russian Federation, the United Kingdom and the United States. Both China and Russia are against military action. However, NATO is another matter, and in response to a request from the six states of the Gulf Cooperation Council, president Obama and NATO are discussing the possibility. Gulf Cooperation Council Requests No-Fly ZonePlease consider Qaddafi Airstrikes Spur NATO Talks of a Libya No-Fly ZoneLibyan government warplanes repeatedly bombed rebel positions near the oil hub of Ras Lanuf, adding urgency to discussions among U.S. and allied governments about imposing a no-fly zone.

President Barack Obama said members of the North Atlantic Treaty Organization are consulting on a "wide range" of potential responses to the turmoil in Libya, including military options. Arab Gulf nations advocated a no-fly zone as oil rose to the highest level in 29 months in New York.

U.K Foreign Secretary William Hague told Parliament that discussions at the United Nations Security Council on a resolution authorizing a no-fly zone are focused on setting a "clear trigger" for UN action and the legal basis for military actions. NATO defense ministers plan to meet March 10 and 11 in Brussels to discuss potential military and humanitarian actions in response to the Libyan clashes.

"I can't imagine the international community and the United Nations standing idly by if Qaddafi and his regime continue to attack their own people systematically," NATO Secretary General Anders Fogh Rasmussen told reporters yesterday in Brussels. "NATO has no intention to intervene in Libya, but as a defense alliance and security organization, our job is to conduct prudent planning for any eventuality."

Obama said yesterday he authorized $15 million for aid organizations in addition to the $2 million the U.S. has already provided to support emergency evacuations of foreign workers who fled to the borders of Egypt and Tunisia.

The six Persian Gulf states of the Gulf Cooperation Council called on the United Nations to impose a no-fly zone over Libya to protect civilians caught in the battles, the group's Secretary-General, Abdul Rahman Al Attiyah, said in Abu Dhabi after a meeting yesterday.

NATO is already increasing its surveillance of Libyan airspace, said the U.S. ambassador to NATO, Ivo Daalder.

The U.S. alliance has been flying Airborne Warning and Control System radar planes for 10 hours a day over the Mediterranean Sea and will increase that to round-the-clock coverage, Daalder told reporters on a conference call yesterday. Information from that monitoring and from NATO planning will be assessed by defense ministers, he said.

Decision Time

"Towards the end of the week, we will be in a position to know what it would take to do a no-fly zone," Daalder said. "We will have a pretty good idea what kinds of options are available."

White House press secretary Jay Carney said yesterday that it is "premature" to discuss sending weapons and supplies to the rebels. While providing arms to the rebels 'is one of the range of options that is being considered,'' Carney said, "it would be premature to send a bunch of weapons to a post office box in eastern Libya. We need to not get ahead of ourselves in terms of the options we are pursuing." Rebels Requests No-Fly ZoneCBS News Reports Libya rebels beg for no-fly as bombings persistCBS News was en route to the front line when a government warplane dropped two bombs on a road leading there. The shrapnel from those bombs was still warm when CBS News arrived at the blast site.

Near the craters was the wreckage of a pickup truck. A family with three children was in it when Qaddafi's air force struck. Two of the children died.

The survivors were slashed by shrapnel. The circling warplanes made for a very jumpy day on the front line

Britain, France Seek No-Fly ResolutionYahoo! News reports Britain, France ready Libya no-fly zone resolutionA British-French resolution demanding a no-fly zone over Libya could go before the UN Security Council as early as this week, diplomats said Monday.

While Moamer Kadhafi's offensive against rebels is intensifying, any demand for military action would set off a new diplomatic battle at the Security Council.

Anticipating opposition, Britain's foreign minister has insisted that there must be "a clear legal basis" for the zone and set other conditions.

"You should expect something on Libya this week," one UN diplomat told AFP on condition of anonymity, confirming that France and Britain are drawing up a resolution. "There is a feeling of urgency now."

"There are elements of a text ready which can be distributed to the council. It could well be this week," said a British diplomat.

Britain and France have made the most aggressive calls among Western powers for a no-fly zone to hamper Kadhafi's offensive. The United States has said it is studying the possibility while warning of the major military operation it would entail.

The UN Security Council unanimously passed sanctions against the Kadhafi regime and ordered a crimes against humanity investigation on February 26. Any new move toward military action is likely to face tough resistance from China, Russia and other members of the 15 however.

Russia's Foreign Minister Sergei Lavrov last week called the no-fly zones "superfluous" and said international powers should concentrate on the existing sanctions.

"We do not consider foreign and especially military intervention a means to resolve the crisis in Libya," Russian news agencies quoted Lavrov as saying Monday. "The Libyans must resolve their problems themselves."

China's foreign ministry also indicated last week that it was cool to military action.

India, also a member of the Security Council, has opposed no-fly zones, though diplomats said it could be swayed if the Libya fighting worsens. How Do You Make a No-Fly Zone?Slate Magazine addresses the question: How Do You Make a No-Fly Zone?American politicians are debating whether to establish a no-fly zone over Libya to prevent Muammar Qaddafi from bombing rebels. The Pentagon and White House advisors warn that such an operation would be complicated and tantamount to war, while several senators say it could be accomplished with relative ease.

How do you set up a no-fly zone?

Generally speaking, the first step in creating a no-fly zone is to blow up nearby anti-aircraft guns, missile batteries, radar installations, or anything else that might be used to shoot down a no-fly air patrol. Not every military commander takes that step: NATO planes didn't wipe out the air defenses in northern or southern Iraq, or the former Yugoslavia, prior to launching patrols. But Defense Secretary Gates has made it clear that he won't send combat planes into Libya without first laying the proper groundwork. If his plan were put into action, the United States would destroy Qaddafi's defenses, then send pairs of fighter jets, mostly F-15s and F-16s, to fly around the country in irregular patterns for six-hour shifts. If the pilots were threatened by ground-based fire, they would engage in evasive maneuvers—quick acceleration, climbing, diving, and sweeping—to thwart the gunners before noting their position and responding with missile strikes.

Some fighter pilots get pretty stoked about patrolling a no-fly zone, because it's one of the few missions that might actually lead to air-to-air combat. (The last American flying ace—that's a pilot who shoots down five or more enemy planes—earned his title during Vietnam.) But those looking for a dogfight in the no-fly zone have usually been disappointed. NATO pilots shot down just one Iraqi plane during the 1990s, and it had barely entered the zone when it was destroyed. After that incident, neither Saddam Hussein nor Slobodan Milosevic wanted to risk his expensive aircraft in a showdown with American pilots, so they kept their planes on the ground and hidden as best they could. Pilots report that no-fly zone patrols involve a few hours of boredom, and a few minutes of excitement evading any ground-based defenses that weren't destroyed ahead of time. Count me in the group that thinks this would be a piece of cake. The Libyan air force would be no match for US fighter pilots. The first few Libyan planes that attempted to fly would be immediately blasted from the sky and that would end the flight attempts right then and there. Addendum:Several people thought what I wrote above implies definitive support for a no-fly zone. It doesn't. I can make a case either way. Here is the no-fly zone case. - We were invited to the party, not only by the rebels but by the Gulf Cooperation Council.

- The mission is easy to define with easy goals.

- The mission curtails little risk.

- The mission has a low cost.

- The US and Europe both have a strategic interest should Qaddafi suddenly decide to start blasting the refineries in a final act of desperation.

Some will find that list compelling, others not. In general terms, I think all 5 of those conditions are necessary before one can even think about a military option. Compare those points to Vietnam, Iraq, and Afghanistan and it is tough to explain how any of those wars met any of the above conditions (simplifying point 5 to the general case "strategic interest"). Nonetheless, I have a great deal of sympathy for the one-point position "this is not our battle". Either way, I strongly oppose sending in US ground troops in any circumstances. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

| Hussman on QE and the "Iron Law of Equilibrium"; Will Stocks Be Firm Until QE II Ends? Posted: 07 Mar 2011 10:23 AM PST Inquiring minds are reading John Hussman's latest post Quantitative Easing and the Iron Law of Equilibrium. The Iron Law of Equilibrium: Every security that is issued must be held by someone until it is retired.

There are three corollaries to that Law: 1) No security can be under- or over-owned. Prices and expected returns adjust to ensure that the exact quantity outstanding is the exact quantity held. The investor's challenge is to ask whether those prices and expected returns are reasonable; 2) The outstanding stock of issued currency and money market securities always remains effectively "on the sidelines" and held by someone - until the time those securities cease to exist; 3) Money never goes "into" or comes "out of" a secondary market. It is always "home."

If you think carefully about equilibrium, it helps to clear up all sorts of fallacies that people hold about the financial markets. For example, the currency and money market securities that are held by investors will - in aggregate - never "find a home" in any other form or any other market. If somebody takes their cash and tries to buy stock, they get the stock and the seller gets the cash. Nothing disappears, and nothing is created - only the owner changes. As I wrote years ago in the Freight Trains and Steep Curves piece that anticipated the recent financial strains, the mountain of money-market securities held by investors is not a reflection of "liquidity looking for a home," but is rather a measure of how dependent borrowers are on short-term sources of credit. Investors are holding a lot of money market securities because a lot of money market securities have been issued, and those securities will stick around until they are retired.

As I noted last week, an understanding of equilibrium is particularly important when it comes to the Federal Reserve's program of Quantitative Easing (QE), so some further discussion may be helpful.

Essentially, QE has added to what will soon be $2.4 trillion of non-interest bearing cash and bank reserves, which someone will have to hold. The first effect of QE is therefore to immediately drive the interest rate on near-substitutes of cash (such as 1-month and 3-month T-bills) to nearly zero. This happens because any significant positive interest rate would induce people to try to shift their holdings from non-interest bearing cash to T-bills, and they bid up T-bills to the point where they are indifferent between the two. In the end, all the T-bills that have been issued are held, and all the cash is held (if interest rates could not be pressed lower, the competition between interest-bearing stores of wealth and zero-interest cash would make cash a "hot potato," causing it to rapidly lose value relative to goods, services, and everything else, which is what we call inflation).

Technically, the Fed is buying Treasury securities and creating currency and bank reserves to pay for them. This would simply be an asset swap were it not for the fact that the U.S. is running a budget deficit of about 10% of GDP, so the Fed's purchases don't even absorb the amount of newly issued Treasury debt. The government budget constraint is simple: spending = taxes, plus the change in Treasury securities held by the public, plus the change in Treasury securities held by the Fed (base money creation). So the overall effect of QE is to reduce the amount of debt that the public would otherwise have to buy, and to instead create money and bank reserves to indirectly finance government spending.

The main effect of QE on the financial markets has little to do with stimulating spending, and everything to do with the fact that the currency and bank reserves bear zero interest, and yet have to be held by someone. In equilibrium, QE requires that the interest rates on near-cash securities must also be nearly zero.

Of course, a similar process happens for riskier and longer-term assets, but the resulting returns are less exact. For stocks, we've seen investors drive prices up to the point where probable 10-year returns are only about 3.2%. But of course, you can get a 3.2% 10-year return by having zero returns for 1-year, and returns averaging about 3.6% for the next 9 years. So depending on the overall profile of returns expected by investors, it's quite possible that near term stock returns have already been driven to zero on a risk and maturity-adjusted basis. The key point, in any event, is that the primary function of QE is to distort market equilibrium by raising the price and depressing the future prospective returns on nearly every asset class.

If you look at the commodity markets, the same factors are at play. Regardless of whether one expects modest or significant inflation, it's clear that the inflation expectations of the market are generally positive. So people expect that a year or two from now, goods and services will be more expensive. But if they are holding cash or money market securities, it is clear that interest earnings will not make up for those higher prices. So what do people predictably do? They hoard commodities now. When does it stop? At the point where commodities are priced high enough that they are expected to have the same negative return, relative to a broad basket of consumer goods, as cash is expected to have.

Keep in mind that commodities aren't really a good inflation hedge once inflation is well anticipated. Rather, commodities tend to "overshoot" in the early stages of inflation, and then typically lose ground relative to the broad CPI as inflation proceeds. For example, in 1975, the CRB shot to about 5 times the level of the CPI. By the early 1980's, the ratio had dropped to half that level, and continued to decline during the subsequent disinflation.

It is widely believed that the rise in commodity prices reflects the effects of China, India and other developing countries, but this long-term growth story certainly didn't prevent commodities from collapsing in 2008. It's a well-known result in resource economics that even when a resource is exhaustible and in significant demand, the price does not rise at a spectacular rate. Rather, except when there are new shocks that were previously unanticipated, the price of an exhaustible resource will tend to increase at roughly the rate of interest (Hotelling's rule).

Certainly, concerns in Libya and elsewhere are creating some additional short-term pressures, but it should be clear that the primary force behind the rise in commodity prices is that QE has suppressed real interest rates to negative levels. If anything, QE is one of the primary forces driving up food and energy prices globally, contributing to extreme difficulty among the impoverished of the world, and adding to social tensions and resulting violence.

With the notable exception of the spike in the CRB triggered by the OPEC oil embargo in 1973, which preceded the movement of real interest rates, a significant portion of commodity price fluctuations reflects pre-emptive hoarding and release of commodities as surrogates for future consumption of goods and services, in response to the difference between expected inflation and the interest rate available on money-market securities. Sideline Cash Myth RevisitedCorollaries two and three above are simply another iteration of the sideline cash myth that Hussman and I have written about many times before. The myth is "cash is waiting to come into the market driving up the price of stocks". The reality is that except for IPOs and debt offerings, for every buyer of a security there is a seller. Thus, no matter how many shares of stock anyone buys, the amount of sideline cash does not change. However, the Fed did succeed in changing short-term sentiment towards equities and commodities alike, and that sentiment change has been to the upside. Will Stocks Be Firm Until QE II Ends?Based on continually bullish surveys, it appears that most market participants expect a positive market bias to commodities and equities until Quantitative Easing stops. While that could be the case, it is not necessarily so. Recall the stock market and commodities started rising on the Fed's QE announcement,months before the program actually started. Might not equities and commodities sell off months ahead of the end of QE II? Of course everyone expects QE III and QE IV. However, those expectations may not translate into reality and it's also possible those expectations have already been priced in, if not more than priced in. CRB Overshoot, Are We There Yet?Hussman points out the tendency of the CRB to "overshot" to the point where commodities have have a large negative value in further hoarding. The same applies to equities. We may (or may not be) at such a point already. Yet, Bernanke denies any responsibility for commodity price pressures while conveniently taking credit for the rise in the stock market. Such a position is clearly not defensible. Stock Market ValuationsHussman wrote "As of last week, the estimate from our standard methodology is that the S&P 500 is priced to achieve total returns over the coming decade averaging about 3.2% annually. That said, this long-term estimate does not reduce into a forecast for near-term returns, or even returns over the next year or two." I think 3.2% is in the high side. For details, please see Negative Annualized Stock Market Returns for the Next 10 Years or Longer? It's Far More Likely Than You ThinkWhatever the rates of return are, I side with Hussman in regards to skew. Returns are highly unlikely to be uniform. Moreover, given the current structural headwinds and fiscal constraints, I believe there is a much greater than even chance the next five years will not be as good as the subsequent five years. Finally, even if Hussman's model is correct, 3.2% annualized returns will cause massive additional stress on poorly-funded pension plans and their unsustainable assumptions of 7.5 to 8% annual returns. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

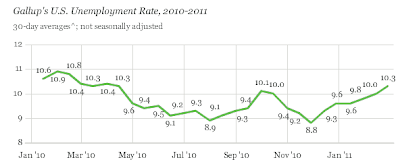

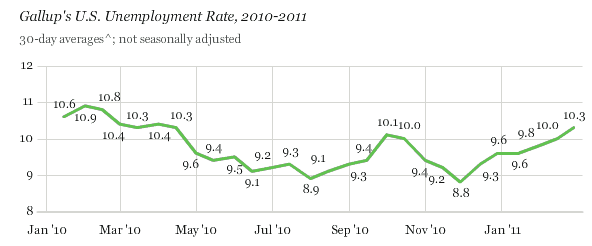

| Gallup Survey Shows Unemployment Rate at 10.3% and Rising, BLS Says 8.9% and Falling Posted: 07 Mar 2011 12:18 AM PST A Gallup survey says the unemployment rate in the US is 10.3% and rising. Meanwhile, the BLS says it's 8.9%. The comparison is not precise because Gallup does not seasonally adjust but the BLS does. However, on an equal comparison basis, Gallup has the unemployment rate where it was a year ago but the BLS shows a drop of .5%. For BLS details please see BLS Jobs Report: Nonfarm Payroll +192,000, Unemployment Rate 8.9%; Reflections on the Jobs Report . Now let's take a look at the most recent Gallup survey. Gallup Finds U.S. Unemployment Hitting 10.3% in FebruaryInquiring minds note Gallup Finds U.S. Unemployment Hitting 10.3% in FebruaryUnemployment, as measured by Gallup without seasonal adjustment, hit 10.3% in February -- up from 9.8% at the end of January. The U.S. unemployment rate is now essentially the same as the 10.4% at the end of February 2010.

Unemployment Rate Not Seasonally Adjusted

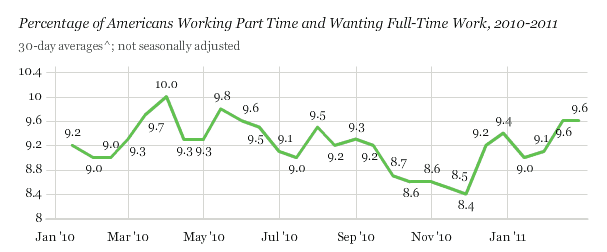

The percentage of part-time workers who want full-time work worsened considerably in February, increasing to 9.6% of the workforce from 9.1% at the end of January. A larger percentage of the U.S. workforce is working part time and wanting full-time work now than was the case a year ago (9.3%).

Part-Time Workers Wanting Full-Time Jobs

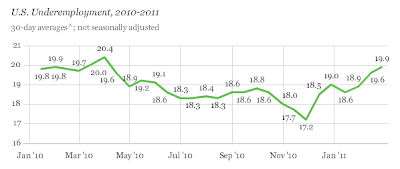

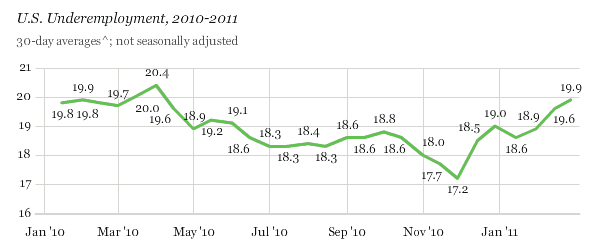

Underemployment Surges in February

Underemployment, a measure that combines part-time workers wanting full-time work with those who are unemployed, surged in February to 19.9%. This resulted from the combination of a sharp 0.5-point increase since the end of January in the percentage unemployed and a 0.5-point increase in the percentage working part time but wanting full-time work. Underemployment is now higher than it was at this point a year ago (19.7%).

Underemployment

This deterioration in the jobs situation combined with surging gas prices, budget battles at the federal and state level, and declines on Wall Street tend to explain the recent plunge Gallup recorded in consumer confidence. They also align with the continued "new normal" spending patterns of early 2011. Although Gallup's Job Creation Index has improved over the past year and showed modest improvement in February, the improvement has not been significant enough to positively affect underemployment and unemployment.

Warren Buffet said Wednesday on CNBC that the U.S. unemployment rate should be in the low 7% range by late 2012. If that is going to be the case, the job creation environment must change dramatically from what it is today. Explaining the DifferencesI was asked to shed some light on the differences between these surveys. Except to reiterate an opinion from last year I cannot. Last year I stated that normal seasonal firing patterns may not play out. My rationale was a belief that we would not see the traditional release of employees in the post-Christmas slump because staffs were cut to the bone and there was a marginal pickup in consumer demand. That presumption now appears to be the case. However, the question is not one of a few good months of non-firing but rather where to from here. I still see no driver for job growth, and that is just what Gallup says. Moreover, I discussed this setup not as an afterthought, but in advance. Adding to that discussion, just yesterday I noted Big-Box Retailers Reconsider Size; Saturation, Online Sales Affect Store Expansion Plans and Hiring Needs...

Big-Box Decisions Affect Store Hiring Plans

I am wondering, do we really need "Walmart Express" at all? At best it is a sign of total saturation of big boxes and a turf battle for smaller cities and neighborhoods.

As such, think about store hiring plans now vs. store hiring plans in the midst of the big-box commercial real estate boom.

With the new "smaller is better" model, another commercial real estate boom remotely close to the build-out that occurred in 2005-2007 is not in the cards.

Moreover, residential housing is still dead.

Together, the picture just does not add up to the 200,000+ jobs a month many economists and market cheerleaders expect. Risks Skewed to the DownsideThe Gallup survey reflects what I suggested would happen. Improvements last month have given way to a relapse this month (it just has not shown up in the BLS reports). Moreover, critical budget issues affect states, and Congress is poised to cut spending. Together with rising oil prices on a supply shock, possible European interest rate hikes, a cutoff in Quantitative Easing, forced cutbacks in China due to overheating, and a stock market that is priced well beyond perfection, the best one can say is that risks are hugely skewed to the downside, both for the stock market and the unemployment picture. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

|

No comments:

Post a Comment